AR in Accounting: A CFO's Guide to Cash Flow Control

Master AR in accounting. This guide for CFOs covers reducing DSO, improving cash flow, and implementing accounts receivable automation for operational control.

If your firm is growing and cash still feels erratic, the issue usually isn't revenue. It's execution inside accounts receivable.

You've done the work. Time was tracked. The invoice went out. But payroll lands before client payments clear, project leaders swear a customer “always pays,” and the aging report keeps getting reviewed after the problem is already expensive. That's the point where ar in accounting stops being a bookkeeping topic and becomes a control problem.

In professional services, AR sits right in the middle of delivery, billing, client communication, and cash forecasting. If those handoffs are loose, cash gets delayed even when clients are willing to pay. If those handoffs are disciplined, the same revenue base produces better liquidity, fewer surprises, and less borrowing pressure.

Beyond the Balance Sheet Reframing AR in Accounting

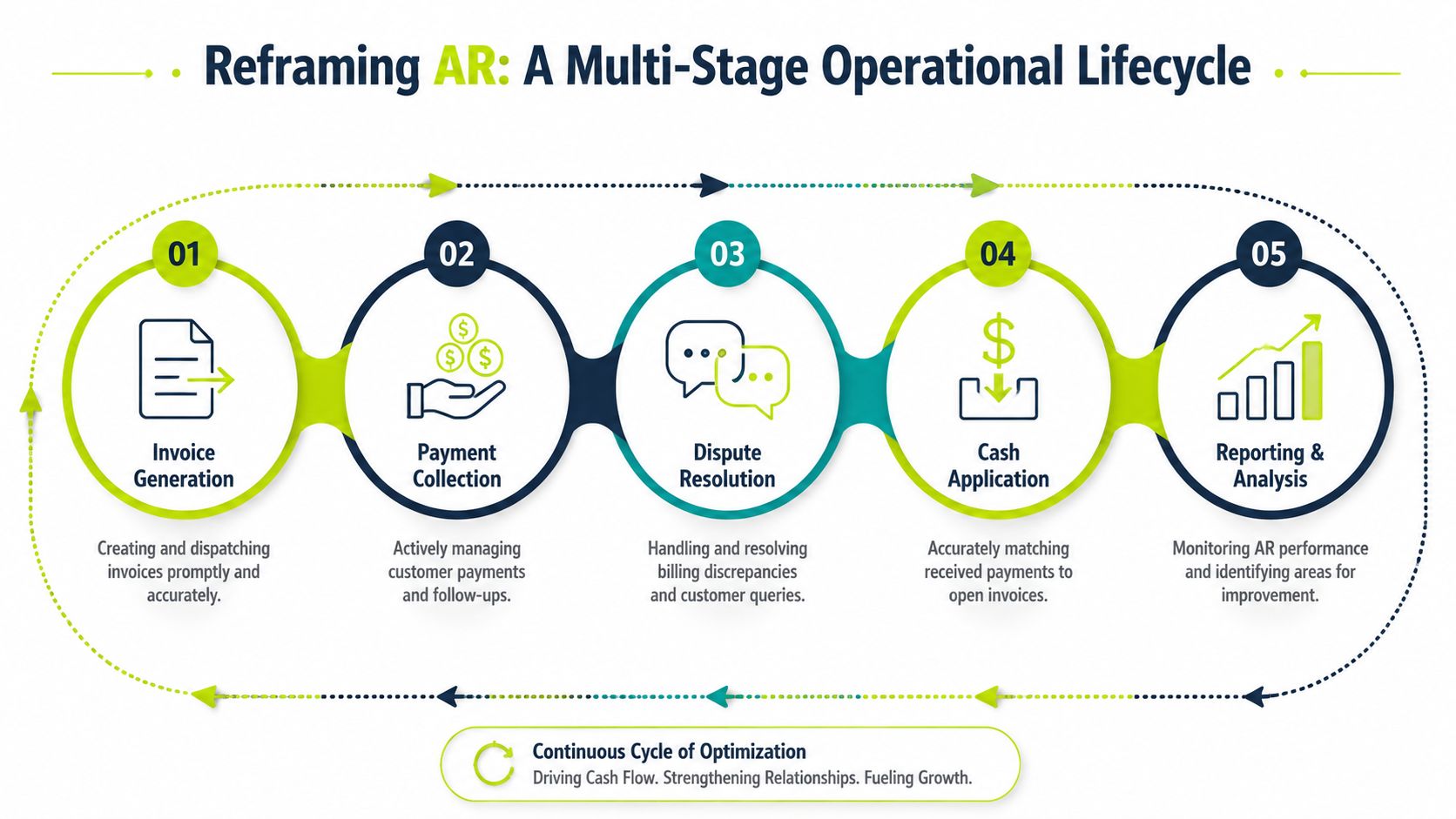

Most firms were taught to think of accounts receivable as a current asset. That's technically correct, but operationally incomplete. For a CFO or controller, AR is better understood as a chain of decisions and handoffs that determines how reliably earned revenue converts to cash.

That distinction matters because a receivable doesn't become risky only when it turns late. It becomes risky much earlier. It starts when a client is onboarded without clean billing contacts, when engagement terms are vague, when time entries are delayed, or when invoices go out with the wrong backup.

In other words, AR is not one number. It's a workflow.

The five control points that matter

A practical AR lifecycle usually looks like this:

- Invoice generation The invoice has to be accurate, timely, and easy to approve on the client side. In services firms, billing delays often start with internal approval bottlenecks, missing purchase order references, or weak matter-level detail.

- Payment collection This isn't just “send a reminder.” It includes cadence, ownership, escalation, and consistency. Many firms rely on partners or account leads to chase selectively, which creates uneven results.

- Dispute resolution A disputed invoice is no longer a pure collections item. It becomes an operating issue involving billing, delivery, and client service. If no one owns dispute aging, invoices stall in limbo.

- Cash application Once payment arrives, someone still has to match it correctly. That's where unapplied cash, short pays, and customer credits start to muddy the ledger.

- Reporting and analysis AR reporting should tell you where cash is getting stuck, not summarize what's already old.

Practical rule: If your team only gets serious about AR after invoices age, you're managing consequences, not causes.

Why manual handoffs create leakage

Manual AR breaks down at the seams. A project manager approves billing late. Finance sends the invoice without required attachments. A client pays partially, but the remittance isn't clear. The cash hits the bank, yet the subledger still looks open. Then leadership reviews distorted numbers and makes decisions from bad visibility.

That's why “chasing invoices” is too narrow. Chasing is one activity inside a broader system.

For firms with international clients or entities, it also helps to review accounting procedures in the UK because local process expectations around payables and receivables can shape how quickly invoices move through approval and payment.

If you need a clean operational distinction between inbound and outbound working-capital processes, this overview of accounts receivable vs accounts payable is useful for aligning finance and operations around ownership.

The Critical AR Metrics That Drive Predictable Cash Flow

Month-end closes. AR shows a healthy total balance. The problem is that total balance does not tell a controller when cash will arrive, where collections are slipping, or whether the team is correcting issues fast enough to protect next month's payroll and partner draws.

That is why AR metrics matter. They turn receivables from an accounting balance into an operating control system.

DSO gets most of the attention. It should. As Versapay explains in its guide to accounts receivable KPIs, DSO measures the average time it takes to collect credit sales. But DSO is a summary measure. It tells you cash is slowing down. It does not tell you whether the cause is delayed billing, weak follow-up, client disputes, or posting errors.

A finance dashboard built for predictability needs a tighter set of measures.

The four metrics I'd put on page one

Metric | What it tells you | Practical read |

|---|---|---|

DSO | Average time to collect receivables | Useful for spotting changes in cash conversion speed, limited for root-cause diagnosis |

AR turnover ratio | How often receivables are collected during a period | Shows cash velocity and how efficiently credit turns into cash |

ADD | How many days invoices are late beyond stated terms | Separates normal payment timing from true delinquency |

CEI | How much of the collectible balance the team actually collected | Shows execution quality in the current period |

Sage includes Days Sales Outstanding, Average Days Delinquent, Collections Effectiveness Index, bad debt ratio, AR turnover ratio, dispute rate, cost of collections, write-off ratio, and customer payment trends in its overview of accounts receivable metrics to track.

Two formulas every controller should know cold

The first is AR turnover ratio:

Net credit sales ÷ average accounts receivable

Average AR is usually beginning AR plus ending AR, divided by two. Higher turnover usually means cash is converting faster and less working capital is sitting idle.

The second is CEI. CEI uses beginning AR, credit sales, ending AR, and bad debt adjustments to measure how effectively the team collected what was available to collect during the period. I rely on CEI because it answers the operating question management cares about: did the team collect what should have been collectible this month?

A flat DSO can still hide a problem. Revenue mix can shift. One large client can pay early. New billings can mask a growing block of overdue invoices. CEI and ADD help expose that kind of false stability.

What works in professional services

In a professional services firm, billing quality shapes every AR metric that follows. Time entries need cleanup. Partners hold drafts. Clients require detailed backup. One delay upstream can make collections look weak even when the AR team is doing its job.

That is why monthly review should follow a clear order of operations:

- Start with DSO to see whether overall cash conversion is getting faster or slower.

- Check ADD to measure actual lateness against agreed terms.

- Use CEI to judge how well the team performed in the current period.

- Review turnover to understand whether receivables are moving with enough speed over time.

For a more detailed operating view of the first metric, this guide on DSO in accounting is a useful reference.

What not to do

Do not manage AR from a single aging report.

Do not let one large account distort your view of the full portfolio.

Do not treat these metrics as finance-only reporting. In professional services, collections results often depend on billing discipline, project management, and client communication long before the invoice becomes overdue.

Predictable cash flow comes from seeing AR early, in the right sequence, with enough precision to act before balances age.

Uncovering the Hidden Costs and Risks in Manual AR

Late payment is the visible symptom. Manual AR failure usually sits somewhere else.

The most common blind spot is cash application. A payment arrives, but the remittance is incomplete, the amount doesn't match the invoice, or the customer netted a credit against a separate job. The bank balance improves, yet the receivable stays open or gets closed incorrectly. Finance thinks cash came in. The ledger tells a different story.

That's how firms end up arguing about collections performance when the underlying issue is posting quality.

Where manual AR usually breaks

The Financial Professionals glossary highlights a point many finance teams learn the hard way: a frequently overlooked problem in AR is not invoice issuance, but cash application after payment arrives, and negative or credit AR balances from misapplied payments, short pays, or overpayments can distort working capital, current ratio, AR turnover, and DSO reporting if they aren't reclassified correctly in this AR glossary reference.

For a professional services firm, those breakdowns usually show up in a few places:

- Unapplied cash that makes open invoices look older than they are

- Short pays that sit unresolved because no one knows whether the issue belongs to billing, account management, or collections

- Overpayments and credits that stay buried in customer accounts and make performance look better or worse than reality

- Disputes without ownership where project teams and finance each assume the other side is handling it

Why this distorts decision-making

When AR is messy, the finance team starts spending time reconciling stories instead of balances.

The controller says collections are improving because cash receipts look stronger. The partner says the client has paid. The AR clerk says several invoices are still open. All three may be partially right. None of them has a clean operating picture.

That's dangerous because leadership decisions start from the wrong premise. You may tighten credit on the wrong client, miss an internal billing problem, or conclude that staff need to collect harder when a more effective solution is better reconciliation and dispute routing.

If your ledger carries hidden credits or unapplied cash, your AR dashboard becomes a confidence trick on your own management team.

The operational cost nobody budgets for

Manual AR also consumes skilled finance capacity in low-value work.

A strong AR specialist should spend time prioritizing risk, resolving exceptions, and coordinating with client-facing teams. Instead, many spend their day assembling backup, checking inboxes for remittance advice, updating notes across spreadsheets, and re-opening invoices that were closed incorrectly.

That slows month-end close, weakens forecasting, and makes client communication inconsistent. In a services business, inconsistency matters. One client gets a polished, timely reminder. Another gets silence until the invoice is old enough to create tension.

The result isn't just delayed cash. It's lower trust in the numbers.

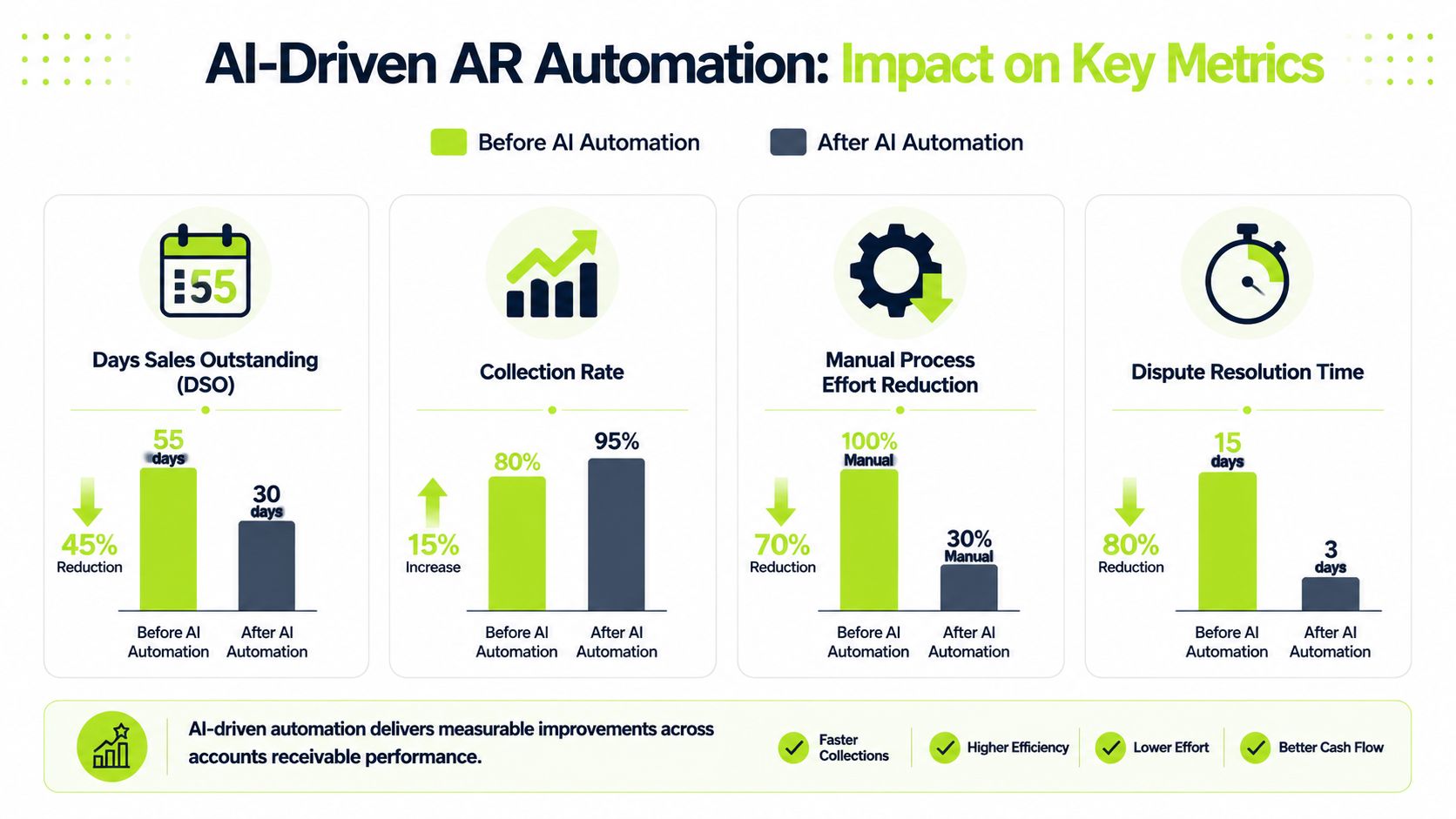

How AI-Driven AR Automation Creates Operational Control

The fix for manual AR isn't “more reminders.” It's a controlled system that coordinates billing, collections, disputes, and cash application with one set of rules and one operating view.

That's why accounts receivable automation has moved from a nice-to-have to a finance infrastructure decision. Quadient reports that the global AR automation market is valued at $3.40 billion in 2025 and is projected to reach $5.95 billion by 2030, with North America accounting for 44.9% of the market in 2025. The same source notes that over 60% of CFOs plan to increase investment in finance automation in 2025 and 72% of finance leaders report using AI tools in their function, up from 34% the prior year, in its review of the accounts receivable landscape in 2025.

That matters because finance leaders aren't buying software for novelty. They're buying control.

What basic automation gets wrong

Basic AR tools usually automate one slice of the process. They send scheduled reminders, maybe expose a payment link, and log activity.

That helps, but it doesn't solve the core problem in professional services. Collections outcomes depend on context. A disputed invoice shouldn't get the same sequence as a clean invoice. A client who pays reliably but slowly needs different handling than a client showing new payment risk. A short pay should trigger research, not a generic nudge.

That's where AI AR automation becomes materially different from rules-only workflows.

What operational control looks like in practice

A useful AR system should do at least four things well:

- Segment intelligently so outreach reflects client behavior, invoice status, and risk profile

- Coordinate exceptions by routing disputes, credits, and short pays to the right owner fast

- Support clean cash application so receipts and remittance data don't sit in manual queues

- Create one reporting layer where collections activity and ledger status line up

Here's a useful overview of how AI for debt collection changes the cadence and quality of collection workflows.

A short walkthrough can help make the operating model concrete:

What works for services firms

In a professional services environment, I'd look for AR software for professional services that handles nuance well. That means integrating with the accounting ledger, preserving client relationship tone, and keeping project teams involved only where they add value.

If your firm runs on QuickBooks AR automation requirements, the practical question is whether the system can sync invoices and payment postings reliably enough that finance doesn't end up maintaining two truths.

One option in this category is Resolut, which combines collections workflows, payment orchestration, and cash application with human-in-the-loop control. The point isn't brand preference. The point is choosing a system that treats AR as one coordinated process instead of separate tasks.

Good automation doesn't remove judgment. It removes the manual friction that keeps judgment from being applied where it matters.

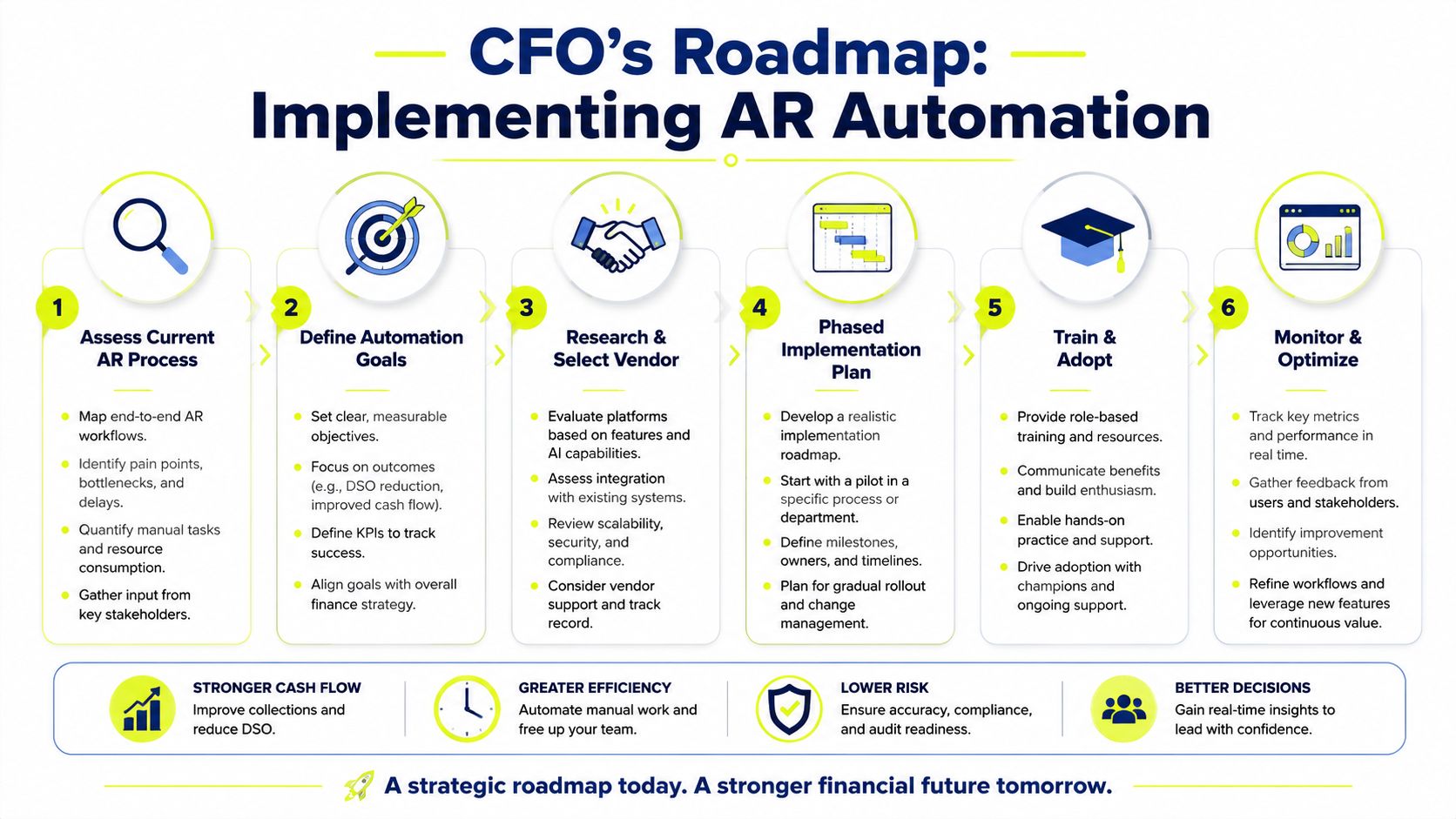

A CFO's Roadmap to Implementing AR Automation

A sound AR automation project starts with a business decision, not a software demo. The first question isn't “Which platform has the most features?” It's “Where are we leaking cash, and is it cheaper to fix collections than fund the gap?”

That trade-off matters. NetSuite's guidance on accounts receivable financing makes the point clearly: AR financing can close working-capital gaps, but at a cost, and in a higher-rate environment the ROI from faster collections through automation can be significantly better than the effective cost of financing or factoring invoices.

Start with the internal case for change

Before you evaluate vendors, pin down the current state.

Use a short diagnostic:

- Map the workflow from invoice approval through payment posting

- List exception types such as disputes, credits, short pays, and unapplied cash

- Identify handoff failures between project teams, billing, AR, and accounting

- Document system reality including QuickBooks, ERP, PSA, CRM, inboxes, and spreadsheets

This gives you something more credible than “our team is busy.” It gives you a cash-control case.

Build the rollout in phases

The best implementations don't try to automate every edge case on day one.

A phased sequence usually works better:

- Clean the data first Standardize customer records, billing contacts, invoice fields, terms, and owner assignments. Automation amplifies data quality, good or bad.

- Launch collections workflows next Start with reminder sequencing, promise-to-pay tracking, and escalation rules. This creates visible discipline quickly.

- Then tackle exceptions Bring disputes, credits, and short pays into managed queues with named owners and status rules.

- Add cash application orchestration It enables many firms to finally get a trustworthy AR picture.

What to ask during vendor selection

For CFOs evaluating accounts receivable automation, the strongest questions are operational:

Question | Why it matters |

|---|---|

Can it integrate cleanly with QuickBooks or our ERP? | If not, reconciliation pain just moves around |

How does it handle disputes and short pays? | Collections alone won't fix exception-heavy AR |

Does it support human review where needed? | Finance still needs control over tone and escalation |

How are workflows configured and changed? | If every edit needs vendor support, agility suffers |

What reporting ties activity to ledger reality? | You need one version of performance |

If your team is also building internal AI capability beyond AR, DataTeams has a practical guide on AI in business that's useful for thinking about adoption, governance, and implementation discipline.

Keep ownership clear

Many projects stall at this stage. Finance buys the software, but nobody clarifies roles.

Use a simple ownership model:

- Controller owns policy, reporting, and close integrity

- AR lead owns workflow execution and exception queues

- Project or account leads support dispute resolution, not routine chasing

- IT or systems support owns integration and data sync oversight

- CFO owns targets, cadence, and accountability

The strongest automation projects are boring after launch. The work becomes routine, visible, and repeatable. That's a sign the controls are doing their job.

Measuring the ROI of Your Automated AR System

ROI should be measured in cash outcomes first, labor outcomes second, and software features last.

The primary indicators are straightforward. Watch whether you reduce DSO, improve collections consistency, lower the volume of overdue invoices, and reduce distortion from unapplied cash and stale credits. If those move in the right direction, your forecasting improves because AR becomes more predictable.

The second layer is cost and capacity. A good automated process reduces the amount of skilled finance time spent on repetitive follow-up, inbox triage, and manual posting cleanup. That time can be redirected into dispute resolution, client communication, credit review, and close quality.

A practical post-launch scorecard

Use a before-and-after review built around a small set of measures:

- Cash conversion performance using DSO, ADD, turnover, and CEI

- Portfolio hygiene by tracking unapplied cash, credit balances, and disputed invoices

- Team efficiency through manual touchpoints removed from the monthly cycle

- Forecast confidence based on whether expected collections are landing when projected

For a CFO, the most valuable outcome is control. When AR is automated well, you stop discovering cash issues late. You see them early, route them correctly, and correct them before they distort the month.

That's where the true value lies. Better liquidity, cleaner reporting, and less management energy wasted on avoidable noise.

Resolut automates AR for professional services with a focus on consistent workflows, accurate cash application, and human oversight where it matters. If your firm wants tighter control over collections, better visibility into receivables, and a calmer month-end, you can learn more at Resolut.