10 B2B Collections Best Practices for 2026

Master B2B collections best practices to reduce DSO and improve cash flow. Actionable insights for CFOs on automation, risk, and client communication.

For many professional services firms, collections feels like a reminder problem. It usually isn’t. Within the wider B2B context, 1 in 10 invoices go unpaid, and enterprises waste about $200 billion each year on the administrative burden of accounts receivable management. That’s the core issue. Too much labor, too little orchestration, and too many breaks between invoicing, follow-up, payment, and reconciliation.

If you run a firm in the $3M to $50M range, the pain shows up fast. Cash gets trapped in aging receivables. Partners ask why revenue is up but the bank balance isn’t. Controllers spend mornings reviewing overdue accounts and afternoons chasing backup, approvals, and remittance details. None of that is strategic work, but it still has to get done.

The firms that improve cash flow don’t just send tougher emails. They build a controlled system. Credit decisions are made earlier. Payment options are easier. Follow-ups are timed by account behavior, not by habit. Cash application happens quickly enough that finance can trust its own aging.

That’s the shift behind strong b2b collections best practices in 2026. Collections works best as an operating system, not a set of disconnected tasks. Pre-invoice risk, customer communication, accounts receivable automation, AI AR automation, and post-payment reconciliation all have to connect. If they don’t, your team ends up doing manual handoffs all month.

For CFOs, Controllers, and firm owners, the objective is simple. Reduce DSO, improve cash flow, preserve client relationships, and keep controls tight.

A few visual formats work especially well for this topic:

- Aging waterfall chart: current, 1-30, 31-60, 61-90, and legal escalation, with collection actions overlaid.

- Invoice-to-cash system map: credit review, billing, reminder cadence, portal payment, cash application, exception routing.

- Cinematic finance visual: a controller reviewing a clean dashboard at dawn, with overdue accounts sorted by risk and next action.

1. Early Payment Incentive Programs

Early payment incentives work when they’re treated as a margin decision, not a blanket concession. In professional services, that matters. A design agency, law firm, engineering firm, or accounting practice often has a small number of meaningful accounts. A discount offered casually can erode profitability faster than it improves cash timing.

Used selectively, though, incentives can shorten the collection cycle without straining the relationship. Buyers often value certainty in their own cash planning. If the terms are clear and the process is easy, an early-pay option can move an invoice from “we’ll get to it” to “approve it now.”

Where incentives actually work

I’ve seen incentive programs perform best with customers that already pay, but pay slowly. They’re less useful for accounts with disputes, procurement bottlenecks, or chronic documentation issues. A discount won’t fix an invoice that’s missing a PO or sitting in the wrong approver’s inbox.

Good candidates include:

- Reliable but slow payers: Accounts that usually settle in full, just later than agreed.

- High-value recurring clients: Buyers with consistent monthly or quarterly billing where predictability matters.

- Annual prepay opportunities: Service retainers or software-like contracts where bundling value with earlier payment makes sense.

Practical rule: Don’t offer an incentive until you know the account-level gross margin can absorb it.

Standardization matters more than creativity here. If one partner offers a discount on a call, another team member interprets it differently, and accounting applies it manually, you’ve created confusion instead of speed. Put the rule in writing, tie it to the invoice, and automate the application in your AR workflow.

What doesn’t work

The weak version of this strategy is broad discounting. That trains clients to wait for exceptions and negotiate routine invoices. It also gives your team another manual decision point.

The stronger version is narrow and controlled. Offer the incentive only to segments where speed of payment clearly outweighs the cost. Then track who uses it and who ignores it. Over time, that tells you whether your issue is pricing, process friction, or payment culture.

For firms using accounts receivable automation, the win is operational discipline. Terms should calculate automatically, appear clearly on the invoice, and flow cleanly into reconciliation. If you use QuickBooks AR automation or a connected AR platform, this is one of the easier controls to implement well.

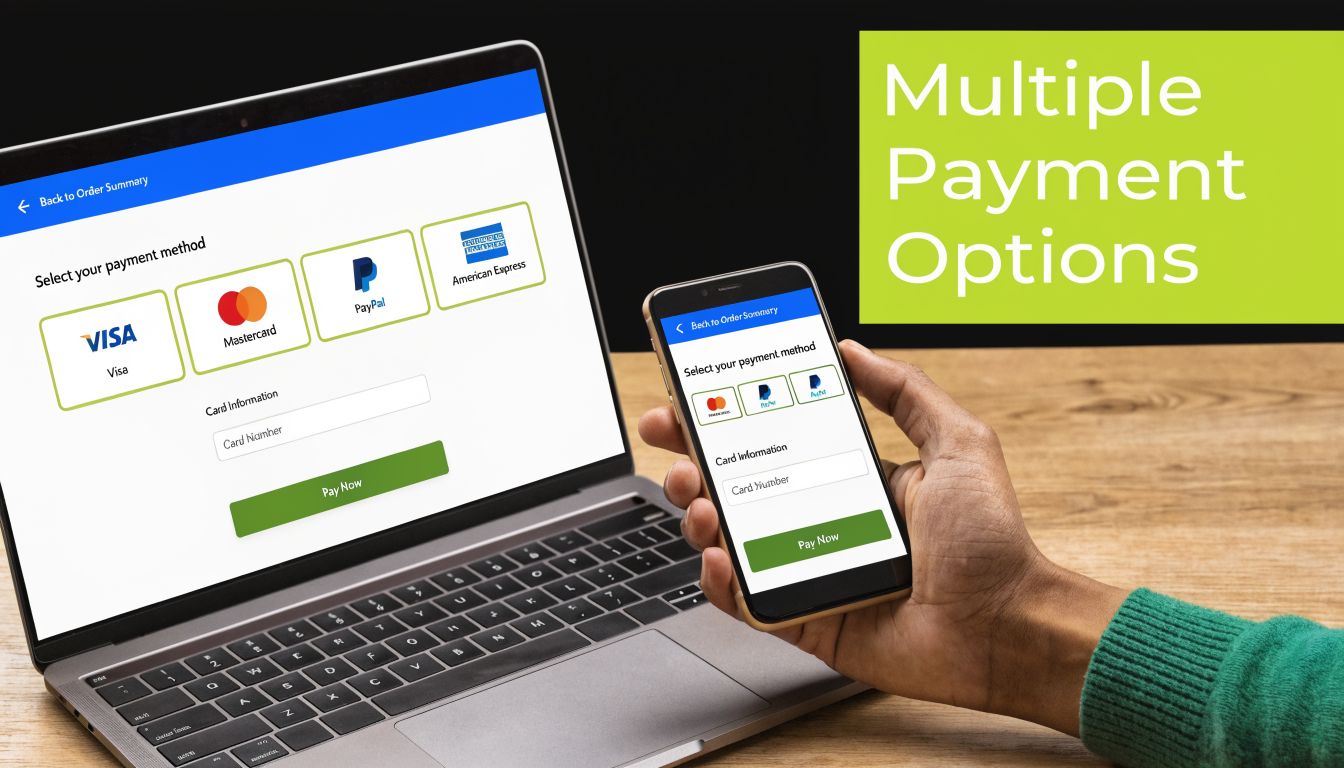

2. Omnichannel Payment Collection

The payment method matters because the collection system is only as fast as the final mile. A reminder can be well timed, accurate, and professionally written, then still miss the cash target if the client has to switch systems, request a copy of the invoice, or wait for AP to find the right approval link.

For professional services firms, omnichannel collection works best as an operating model, not a volume tactic. The goal is to connect outreach, payment choice, and posting into one controlled workflow. Email delivers the invoice and supporting detail. A portal gives the client a direct path to approve and pay. SMS can support a simple reminder when a payment link is appropriate. Phone calls still matter when an approver has gone quiet, the billing contact has changed, or a dispute is slowing release.

The control point is orchestration. Every channel should point back to the same customer record, the same invoice status, and the same payment options. If a client opens an email, clicks into the portal, promises payment on a call, and then pays by ACH, finance should see that activity in one place. That reduces duplicate follow-up and gives collectors a cleaner next action.

Remove friction at the payment step

Many overdue invoices are not credit problems. They are process problems. The client intends to pay, but the path is slow or unclear.

Common fixes are operational:

- Offer the payment rails clients use: ACH, bank transfer, card, and other approved methods that fit the account.

- Tie every reminder to execution: The message should lead directly to invoice detail, backup documents, and the payment screen.

- Use channels for specific jobs: Email handles documentation, calls handle exceptions and commitment, and portals handle approval and payment.

- Capture activity centrally: Notes, promises to pay, disputes, and remittance details should stay in the same AR workflow.

The trade-off is complexity. More channels can improve response rates, but only if they run through one process. If collections sends emails from one tool, logs call notes in a spreadsheet, and receives payments through a separate portal, the team creates blind spots. Cash may come in, but follow-up stays manual, promises get missed, and cash application slows down.

A well-run omnichannel setup shortens DSO because it removes handoffs across the full invoice-to-cash cycle. That is the point. In a disciplined AR environment, channel choice supports execution, and execution flows directly into reconciliation.

3. Intelligent Risk Segmentation and Early Warning Systems

Past-due aging alone is a weak control. By the time an invoice sits in the 31 to 60 bucket, finance is already reacting to a problem that started earlier in the customer lifecycle.

A better model scores risk across the full invoice-to-cash process. For professional services firms, that means connecting pre-invoice credit posture, billing quality, approval behavior, dispute patterns, and payment execution into one operating system. Collections gets sharper because the team works from signals, not just aging reports.

The practical payoff is better allocation of collector time. Accounts with stable behavior can stay on a lighter-touch path. Accounts showing stress can move to earlier review, tighter follow-up, or account-level escalation before exposure grows.

Build the warning system upstream

Early warning usually starts outside collections. Engagement managers see slower approval cycles. Billing teams see more pushback on time entries or missing purchase order details. Sales hears about budget freezes, project pauses, or leadership changes. If those signals never reach AR, the first formal alert is often a missed due date.

That handoff matters.

A usable segmentation model pulls a small set of signals into one view and assigns a clear next action. Common inputs include:

- Payment behavior: average days to pay, partial payments, broken promises, dispute frequency, unapplied cash patterns

- Billing quality: invoice corrections, rejected invoices, missing backup, approval delays

- Account exposure: open balance, recent credit use, contract value, renewal timing, project dependency

- External risk data: commercial credit inputs for larger or higher-risk accounts, where the cost is justified

The trade-off is complexity. Adding every possible variable creates a model no one trusts and no collector uses. Start with the handful of indicators that consistently predict delay in your own book of business, then refine from there.

Score for action, not for reporting

Risk segmentation fails when it produces a dashboard instead of a workflow. Finance needs a score, the reason the account was flagged, and the required response. If an account moves from low to medium risk because disputes increased and approvals slowed, the collector should know that immediately and change the approach.

That is where accounts receivables automation earns its keep. The system can route high-risk invoices to earlier intervention, hold low-risk accounts in a lighter sequence, and surface exceptions for human review. The value is not the score by itself. The value is consistent action tied to the score.

Judgment still matters. A temporary AP staffing issue may create a short-term risk signal without changing the long-term health of the account. Another client may look stable on paper while communication patterns suggest real deterioration. Good teams use the model to prioritize attention, then apply commercial context before escalating.

Keep the design simple:

- Risk score

- Primary reason code

- Recommended next step

- Escalation threshold

- Owner

If the team cannot explain why an account was flagged, the model will not hold up in daily use. If it does hold up, segmentation becomes more than a collections tactic. It becomes an early control point across the entire cash cycle.

4. Automated Workflow Orchestration and Dynamic Collections

Static dunning doesn’t hold up well in B2B. The same reminder cadence sent to every customer, in the same tone, through the same channel, usually creates two problems. Good customers get over-contacted, and risky accounts don’t get enough intervention early.

Dynamic workflow orchestration is a better control model. It routes each invoice through a sequence based on customer behavior, risk, response history, and commercial importance. That’s where accounts receivable automation starts behaving like an operating system instead of a timer.

A practical example is an AR platform that keeps soft-touch reminders on low-risk accounts while escalating high-risk invoices sooner, with human review for exceptions. That’s the logic behind modern accounts receivables automation. It’s less about sending more messages and more about sequencing the right action at the right time.

Dynamic beats static

The old model is easy to recognize. Day 1 reminder. Day 15 reminder. Day 30 call. Day 45 escalation. It’s simple, but it ignores context.

A dynamic model asks better questions:

- Has this client opened prior reminders?

- Did they click through but not pay?

- Have they broken a promise-to-pay before?

- Is this a strategic account that needs account-manager visibility?

- Is there a dispute or documentation request already in motion?

That changes the next step. Sometimes the right move is another reminder. Sometimes it’s a call. Sometimes it’s pausing collections until billing corrects an issue. Automation should be able to do all three without creating audit gaps.

Keep a human in the loop where it matters

For firms new to AI AR automation, I’d start with co-pilot logic, not full autopilot. Let the system draft sequences, trigger reminders, route exceptions, and suggest escalation. Keep humans on high-value accounts, disputed invoices, and anything with legal or relationship sensitivity.

That balance matters in professional services because collections touches active clients. You’re not just recovering cash. You’re managing a live commercial relationship.

A short demo often helps finance teams picture the workflow in practice:

What doesn’t work is automating bad process. If your billing data is inconsistent or your dispute ownership is unclear, workflow software accelerates confusion. Clean rules first. Automation second.

5. Strategic Legal Escalation and Authoritative Messaging

Legal escalation is a control point, not a starting tactic. Used too early, it damages relationships and weakens your credibility. Used too late, it leaves money on the table and signals that your terms aren’t enforced.

The middle ground is authoritative escalation. That means formal, legally reviewed messaging at the right aging threshold, after normal collection efforts have been documented. It increases seriousness without immediately pushing the account into litigation.

For professional services firms, this is often the moment when an overdue client realizes the invoice is no longer sitting in a routine AP queue. Tone matters here. The message should be firm, specific, and documented, but not theatrical.

Use legal escalation deliberately

A useful trigger is repeated non-response after standard outreach, especially where there’s no valid dispute and the client has received complete invoice support. By that point, your team should already have a clean record of reminders, calls, commitments, and broken follow-through.

When you need to formalize the next step, a structured legal demand letter for payment gives the account a clear choice. Resolve the balance, agree to a plan, or accept that the matter is moving out of routine collections.

Operator’s view: Legal language should create urgency, not drama.

That distinction matters. The purpose isn’t intimidation. It’s clarity. The customer needs to understand that internal collection is ending and the consequences are becoming more formal.

What to avoid

Two mistakes show up often. The first is bluffing. If you send legal-style messaging with no policy behind it, customers learn quickly that your escalation has no weight. The second is overuse. If every aging invoice gets a lawyerly tone, strategic accounts will remember it.

Reserve legal escalation for accounts that have exhausted standard paths. In a good workflow, that handoff is rule-based, approved, and visible to leadership. Sales, client service, and finance should all know when an account has crossed that line.

This is also where disciplined documentation pays off. If the matter proceeds further, your strongest asset isn’t the final letter. It’s the complete history of clear invoices, clear terms, and reasonable collection efforts.

6. Automated Invoice-to-Cash I2C Process Integration

Most collection problems start earlier than finance wants to admit. An invoice goes out with the wrong contact. A project team misses a billing milestone. A customer has terms that don’t match the contract. Collections then inherits the mess and gets blamed for slow cash.

That’s why invoice-to-cash integration matters. Collections is only one segment of a larger control chain. If credit setup, billing, payment capture, and cash application are disconnected, your team will spend the month reconciling process failures by hand.

For operators, the target is one connected flow. Client approved. Work billed correctly. Terms applied correctly. Reminder logic triggered appropriately. Payment posted cleanly. Exceptions routed without email chaos.

Build around the system of record

This usually starts with the accounting or ERP platform. For many smaller and mid-sized firms, that means QuickBooks, NetSuite, Sage Intacct, or a practice management system connected to finance. If you’re evaluating QuickBooks AR automation, this is the first question to ask: does the workflow bolt on reminders, or does it connect invoice status, collections activity, and reconciliation?

A strong I2C design should include:

- Shared customer master data: One source for contacts, terms, tax status, and billing rules.

- Automated status changes: Sent, viewed, disputed, promised, paid, partially paid.

- Exception routing: Billing issues go to billing. Payment questions go to AR. Relationship issues go to the owner.

Integration reduces noise

When teams talk about reducing DSO, they often focus on collector productivity. That matters, but integration usually creates the bigger gain in a professional services environment. It reduces avoidable errors and prevents overdue balances from being created by internal fragmentation.

The firms that struggle most tend to have hidden handoffs everywhere. Billing exports to one file. Follow-up happens in email. Promise dates sit in notes. Payments arrive in another system. Then accounting closes the month with incomplete visibility.

That setup makes every collection conversation harder than it needs to be. Integrated invoice-to-cash turns those conversations into controlled exceptions rather than routine chaos. It also gives leadership a more believable view of expected cash.

7. Customer Segmentation and Customized Collection Strategies

One-size-fits-all collections is usually a sign that the firm hasn’t decided what matters most. Revenue concentration, client lifetime value, margin, strategic importance, and payment behavior all affect how an account should be handled. Yet many firms still run the same sequence for every customer because it feels fair and easy to administer.

It’s easy, but it’s not effective.

A customized strategy starts by acknowledging that a long-standing anchor client, a new mid-market customer, and a chronically late low-margin account shouldn’t receive the same treatment. Segmentation helps finance protect cash without damaging relationships that still matter commercially.

Segment by business impact, not just invoice size

Invoice amount is only one variable. In professional services, the more useful segmentation questions are usually broader. Is the client profitable? Is the relationship strategic? Is there active project work underway? Does the client create frequent billing friction? How reliable are approvals?

I’d structure collection treatment around account reality:

- Strategic accounts: Higher coordination with account leads, lower tolerance for tone missteps, faster issue resolution.

- Stable core clients: Automated reminders, portal-first collection, light-touch phone follow-up when needed.

- High-friction accounts: Earlier review, tighter documentation, more active ownership from finance.

- Low-value chronic late payers: More standardized enforcement and fewer custom accommodations.

If your CRM, billing data, and AR system aren’t aligned, segmentation quickly degrades. That’s one reason disciplined data hygiene matters. Work in finance depends on definitions staying stable across systems. The same principle behind strong database management best practices applies here. If customer records are inconsistent, collection strategy becomes inconsistent too.

Alignment matters as much as segmentation

A segment model only works if sales, client service, and finance use the same language. If sales calls an account “strategic” but finance sees repeated late payment and shrinking realization, there needs to be a shared decision process.

This is also where leadership meetings help. Not long meetings. Just regular reviews of delinquency by segment, relationship risk, and next-step ownership. That keeps collections from operating in a silo and stops account exceptions from becoming political debates.

Strong segmentation doesn’t make collections harsher. It makes it more consistent.

That consistency is what improves cash flow over time.

8. Real-Time Cash Application and Reconciliation

A meaningful share of AR delays happens after the customer has already paid. Cash is in the bank, but it is not yet applied, reconciled, and reflected correctly across the ledger, aging, and customer record. For a professional services firm, that gap creates avoidable noise. Teams chase balances that are already covered, dispute history becomes harder to read, and month-end close takes longer than it should.

Cash application is not a back-office cleanup task. It is a control point inside the same operating system that starts with credit review and ends with posted cash. If the upstream collection process is disciplined but payments still sit unapplied, reporting quality breaks down at the final step.

The usual failure points are familiar. Clients send one payment for multiple invoices. They short-pay because of a disputed line item. Remittance advice arrives late, or not at all. Reference numbers in the bank file do not match invoice numbers in the billing system. Manual reconciliation handles these cases eventually, but it ties up skilled AR time in work that software should absorb.

The better model is straightforward. Auto-apply the clean receipts immediately. Send probable matches into a review queue with context. Route true exceptions to the right owner based on the issue, not just to a generic AR inbox.

That design usually includes automated payment reconciliation connected to bank feeds, payment processors, and invoice data so posting logic runs continuously instead of waiting for batch cleanup.

A practical rule set looks like this:

- Auto-match exact receipts: Same customer, same invoice, same amount.

- Queue likely matches for review: Partial payments, bundled remittances, deductions, and short-pays.

- Assign exceptions by cause: Billing resolves invoice errors. AR resolves remittance gaps. Account owners step in when the issue is commercial, not clerical.

This affects collections performance directly. Unapplied cash keeps invoices open on paper, which can trigger reminders, collector follow-up, and escalation on balances the client believes were already handled. That creates friction fast.

It also affects the client experience in a more specific way than many teams expect. Good customer self-service depends on accurate balances, payment status, and invoice history. If reconciliation lags, the portal shows stale information and customers lose confidence in the numbers.

Controllers should track unapplied cash volume, time-to-application, exception rate, and rework by cause. Those measures show whether the invoice-to-cash process is operating as one system or as disconnected steps. When cash is applied in real time, aging becomes more reliable, follow-up gets cleaner, and finance spends more time on true exceptions instead of preventable cleanup.

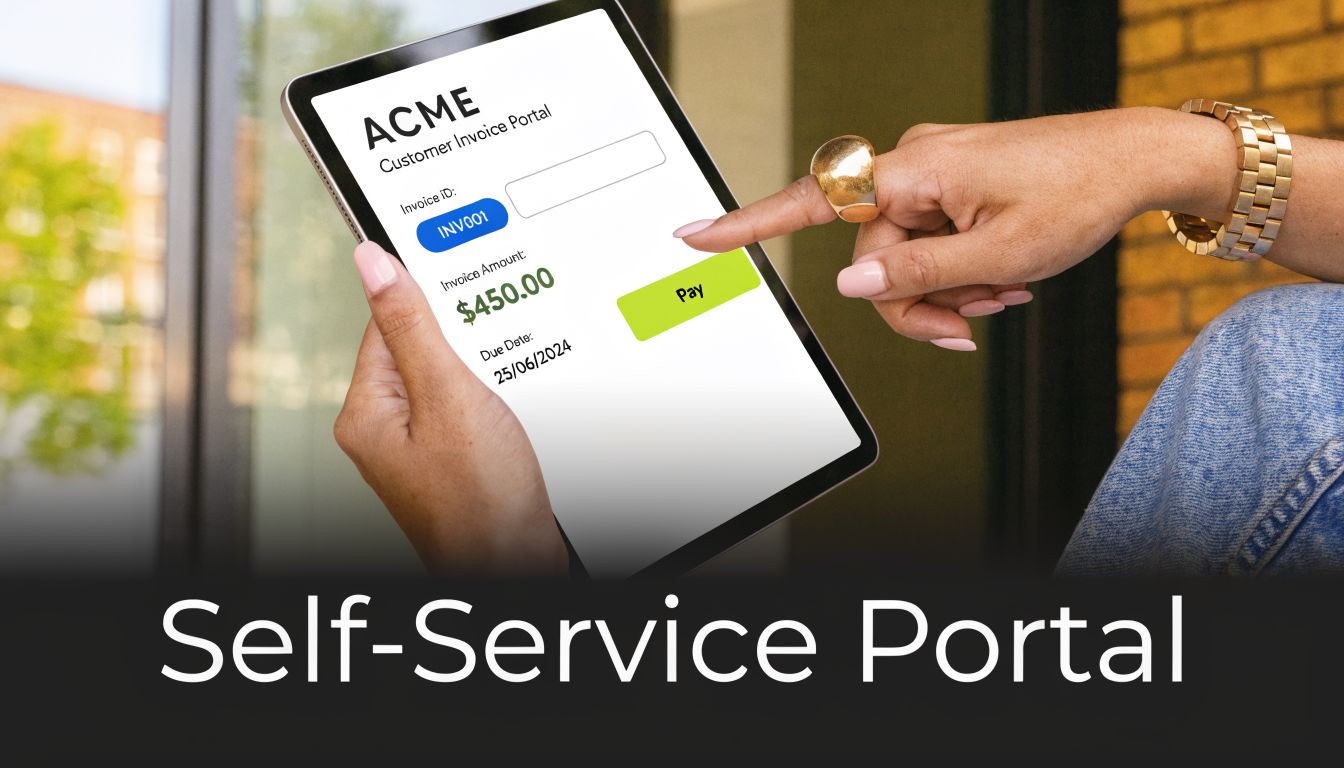

9. Proactive Customer Communication and Portal Self-Service

Many overdue invoices aren’t blocked by refusal. They’re blocked by effort. The customer needs a copy of the invoice, wants to confirm open balances, needs to split a payment, or doesn’t know where to pay. If every one of those steps requires emailing your AR inbox, delays stack up quickly.

A self-service portal solves a large part of that problem. It gives customers a clean place to see invoices, payment history, account status, and available payment methods without waiting on your team. Done well, it reduces inbound noise and accelerates payment.

This is one of the most practical b2b collections best practices for firms that want better control without becoming more aggressive. You’re making it easier for good customers to do the right thing.

Self-service should reduce work on both sides

A portal shouldn’t just be a payment button. It should answer the questions that usually create payment lag. What’s due now? What was already paid? Can I download the invoice? Can I resolve this on mobile? Can I pay without calling someone?

That’s why the best portal experiences borrow from broader ideas in customer self-service. The user experience matters. If AP or an approver can’t readily use it, they’ll default back to email and your team becomes the bottleneck again.

The highest-value features are usually straightforward:

- Invoice visibility: Current and overdue balances, with backup available.

- Payment flexibility: Card, ACH, wire, or other practical options.

- Status transparency: Paid, pending, partially paid, disputed.

Keep the portal tied to outreach

Portals work best when they’re embedded in your collection process. A reminder should point directly to the invoice and payment path. A dispute notice should route to the right handler. A promise-to-pay should be captured back into the system.

What doesn’t work is launching a portal and assuming customers will adopt it on their own. Finance has to drive behavior. Include it in invoice delivery, follow-up emails, onboarding, and account reviews.

When that happens, your team spends less time sending copies and more time resolving actual exceptions. That’s a clean trade for any controller trying to improve cash flow without adding headcount.

10. Performance Metrics, Analytics, and Continuous Optimization

High-performing collections teams measure cash movement, not task volume. Call counts, reminder totals, and completed follow-ups have some staffing value, but they do not show whether the invoice-to-cash system is working.

The right scorecard connects the full operating chain. Credit policy affects dispute rates. Billing accuracy affects delinquency. Payment method mix affects settlement timing. Cash application speed affects what collectors see and what leadership believes is overdue. In professional services firms, where invoices often include milestones, change orders, retainers, and client-specific approval paths, that connection matters even more.

A useful dashboard should answer a short list of operating questions fast. Where is cash slowing down? Which client segments are slipping? Are broken promises-to-pay rising? Is reported delinquency real, or is unapplied cash distorting the picture?

Track a small set of measures that change decisions:

- Cash outcomes: DSO, CEI, overdue trend, and cash collected against target

- Execution quality: Promise-to-pay kept rate, dispute cycle time, touch-to-resolution rate, and collector productivity by portfolio

- System health: Billing exception volume, unapplied cash aging, short-pay frequency, and credit memo trends

- Segment performance: Delinquency by client type, service line, office, partner, geography, or account owner

The point is control. If DSO rises because invoices went out late, collections is not the first fix. If CEI drops in one segment while dispute volume rises, the billing process or contract setup may be the source. Good analytics prevent finance teams from pushing collectors to solve upstream failures.

Optimization also needs a review cadence. Monthly is usually the minimum. Weekly works better for larger portfolios or firms with uneven billing cycles. Review the same metrics, test one rule change at a time, and watch for downstream effects in dispute rates, payment timing, and cash application workload.

Payment behavior also varies by customer base and channel. Research from Resolve on net terms penetration in B2B marketplaces shows meaningful differences by region and marketplace type. That matters operationally. A collections workflow that performs well with enterprise accounts on established terms may underperform with smaller clients, newer buyers, or accounts routed through procurement platforms.

Strong teams use analytics to tune the whole system, not just the reminder sequence. They adjust credit thresholds, invoice controls, escalation timing, payment options, and cash application rules as one operating model. That is how collections becomes more predictable, headcount scales better, and cash forecasts get closer to reality.

B2B Collections: 10-Point Best Practices Comparison

Item | Implementation Complexity 🔄 | Resource Requirements ⚡ | Expected Outcomes ⭐ / 📊 | Ideal Use Cases 💡 | Key Advantages |

|---|---|---|---|---|---|

Early Payment Incentive Programs | Low–Medium 🔄, simple policy & invoicing changes | Low ⚡, invoicing system updates, accounting tracking | Moderate DSO reduction ⭐📊; faster cash but some margin erosion | B2B with large invoice values; price-sensitive buyers | Easy to deploy; predictable cash improvement; minimal staff change |

Omnichannel Payment Collection | Medium–High 🔄, multiple channel integrations | High ⚡, payment processors, security, ongoing ops | Higher conversion & first-contact payments ⭐📊; reduced friction | Diverse customer base; mobile and remote approvers | Improves CX; real-time updates; increases voluntary payments |

Intelligent Risk Segmentation & Early Warning Systems | High 🔄, model development and integration | High ⚡, data pipelines, analytics, external feeds | Prevents bad debt; prioritized collections; lower defaults ⭐📊 | Large portfolios with mixed credit risk; proactive risk control | Early identification of at-risk accounts; data-driven prioritization |

Automated Workflow Orchestration & Dynamic Collections | Medium–High 🔄, rule design and testing | Medium–High ⚡, automation platform, CRM/ERP integration | Improved collection rates & reduced manual work ⭐📊⚡; scalable operations | High-volume AR teams; need for personalized outreach at scale | Personalized, adaptive campaigns; consistent outreach; saves labor |

Strategic Legal Escalation & Authoritative Messaging | Medium 🔄, compliance & escalation rules | Medium ⚡, legal counsel, documentation workflows | Increased payment compliance and settlements ⭐📊; avoids immediate litigation | Aged receivables; accounts unresponsive to standard collections | Cost‑effective pressure; documented trail for potential litigation |

Automated Invoice-to-Cash (I2C) Process Integration | High 🔄, end-to-end system integration | High ⚡, ERP integration, change mgmt, IT resources | Faster cash conversion; fewer errors; full visibility ⭐📊⚡ | Enterprises with multiple systems seeking end-to-end automation | Eliminates manual handoffs; real-time AR visibility; better forecasting |

Customer Segmentation & Customized Collection Strategies | Medium 🔄, segmentation rules & policy alignment | Medium ⚡, analytics, cross-team coordination | Higher recovery and preserved relationships ⭐📊 | Businesses with strategic accounts and mixed customer profiles | Tailored treatment boosts effectiveness and protects key customers |

Real-Time Cash Application & Reconciliation | Medium–High 🔄, matching logic & bank feeds | Medium–High ⚡, bank integrations, matching algorithms | Immediate cash visibility; faster month-end close ⭐📊⚡ | High payment volumes; firms needing accurate cash positions | Reduces manual reconciliation; improves accounting accuracy |

Proactive Customer Communication & Portal Self-Service | Medium 🔄, portal development & UX | Medium ⚡, portal, integrations, maintenance | More self-service payments; fewer inquiries; better satisfaction ⭐📊 | Customer bases comfortable with digital tools; mobile users | 24/7 payment capability; transparency; reduced support load |

Performance Metrics, Analytics & Continuous Optimization | Medium 🔄, measurement framework & dashboards | Medium ⚡, BI tools, data governance, analyst time | Data-driven DSO reduction; better investment decisions ⭐📊 | Organizations seeking continuous AR improvement and accountability | Objective visibility; drives iterative improvements and ROI-based changes |

From Reactive Collections to Proactive Cash Flow

The strongest collections environments don’t rely on heroic effort. They rely on design. This principle unifies these b2b collections best practices. Early payment incentives only work if margin controls are clear. Omnichannel collection only works if the channels are orchestrated. Risk segmentation only works if it changes sequence, tone, and ownership. Workflow automation only works if billing, collections, and reconciliation are connected.

For professional services firms, this matters even more because collections isn’t happening at arm’s length. The customer is often an active client. The invoice may relate to an ongoing engagement, a recurring retainer, or a project team that still needs access and trust. That means your system has to balance firmness with professionalism. Loose process creates more relationship damage than disciplined collections ever will.

A lot of firms still operate with partial automation. They may send reminders automatically but review risk manually. They may collect payments online but reconcile them by hand. They may have an aging report in the ERP but no reliable way to capture promise-to-pay dates, route disputes, or give account leaders visibility into at-risk balances. That setup feels modern on the surface, but operationally it still depends on inboxes, spreadsheets, and memory.

The better model is integrated. Pre-invoice credit discipline informs post-invoice follow-up. Billing data flows directly into collections workflows. AI AR automation helps identify risk and prioritize action. Self-service options reduce friction for customers who need a faster path to payment. Cash application closes the loop quickly enough that leadership can trust the numbers. That’s how you reduce DSO in a way that lasts.

There’s also a control advantage here. When the invoice-to-cash cycle is connected, exceptions become easier to see. You can tell whether a late payment is caused by buyer behavior, weak terms, poor invoice quality, limited payment options, or internal delay. Without that visibility, every overdue balance looks the same and finance ends up treating symptoms instead of causes.

If I had to narrow it down to one principle, it would be this: don’t optimize collections as a standalone function. Optimize it as part of a single operating system for cash conversion. That shift changes the work. Collectors spend less time chasing documentation. Controllers spend less time reconciling uncertainty. CFOs get a cleaner view of expected cash and a more credible plan to improve it.

That’s also why accounts receivable automation has become more relevant for firms in the middle market. At a certain scale, process discipline can’t depend on one strong AR person or one partner who knows which clients need special handling. It needs to be built into the system. For firms already using QuickBooks or similar finance tools, the opportunity is usually not to replace everything at once. It’s to connect the missing layers, especially collections orchestration, payment experience, and reconciliation.

Resolut fits naturally into that operating model. It automates AR for professional services with a focus on consistency, accuracy, and human oversight. That combination matters. Finance teams need automation, but they also need to know when a live customer relationship requires context and judgment.

If you want a more controlled way to reduce DSO and improve cash flow, Resolut is one option built for that job. It brings credit risk, collections, omnichannel outreach, payment workflows, and cash application into one AR system, so your team can operate consistently without sounding robotic.