Cash Application Automation: A CFO's Guide to Control

A CFO's guide to cash application automation. Learn to reduce DSO, improve cash flow, and transform AR from a manual task into a strategic advantage.

Monday morning looks fine in the bank account. By Wednesday, your AR aging still says several clients are overdue. By Friday, someone on the team discovers the money came in, but it's sitting unapplied because the remittance was buried in an email thread, attached as a PDF, or split across multiple invoices in a way your system didn't catch.

That gap is where working capital gets fuzzy.

In professional services firms, the damage isn't dramatic enough to trigger a fire drill. It shows up as slower closes, awkward client follow-ups, stale cash forecasts, and finance staff spending their best hours on reconciliation instead of control. A partner asks whether a client has paid. The controller says, “We think so.” That answer is expensive.

Manual cash application often survives because it feels manageable. A few spreadsheets. A few inbox rules. Someone in accounting who “knows how to work it out.” But as payment volume, client complexity, and payment channels grow, that manual process stops being administrative support and starts becoming a silent margin leak.

The Hidden Drag on Your Firm's Cash Flow

In a typical professional services firm, cash application doesn't fail all at once. It degrades gradually.

A client pays three invoices in one ACH. Another takes a deduction without explanation. A third sends remittance advice to an account manager instead of finance. The cash is received, but the system doesn't reflect settled invoices quickly enough. Your AR report drifts away from operational reality.

What manual work really looks like

The finance team downloads bank activity, opens PDF remittances, checks email attachments, compares invoice numbers, keys allocations into the ERP or accounting system, and then circles back on exceptions. If you're using QuickBooks, Sage Intacct, NetSuite, or a mix of tools plus spreadsheets, you already know the problem isn't just matching. It's gathering the information needed to match.

That creates three practical issues:

- Cash visibility lags: Money is in the bank, but not properly reflected against open receivables.

- Collections get distorted: Teams chase invoices that may already be paid, partially paid, or disputed.

- Month-end gets heavier: Unapplied cash and unresolved items pile up until close.

Manual cash application rarely looks broken in isolation. It looks “good enough” until finance needs a clean answer fast.

For a services business, that matters more than many owners expect. Revenue is tied to people, utilization, project delivery, and timing. If the firm can't see which invoices are open and which payments are already in motion, decisions on hiring, draws, vendor timing, and growth all rest on a blurred picture.

Why this is a finance leadership issue

This isn't just an AR clerk problem. It's a controller and CFO problem because cash application sits between payment receipt and financial truth.

A widely cited benchmark from Deluxe reports that only 19% of large companies have highly automated accounts receivables groups, meaning most still rely on manual workflows, which helps explain why this remains such a broad operating issue across finance teams (Deluxe benchmark on AR automation).

For smaller and mid-sized firms, the lesson is straightforward. If even large organizations haven't solved this cleanly, professional services firms with lean teams should expect manual cash application to create friction unless they design for control. That's why accounts receivable automation and AI AR automation are moving from nice-to-have projects into core finance infrastructure.

Beyond Matching Payments to Invoices

Cash application automation is often described too narrowly. It's not just software that checks a payment against an invoice number.

It's a workflow that captures payment information from wherever it arrives, structures it, matches it to open invoices, routes exceptions, and posts the result back into the accounting system. Esker describes it as a multi-stage pipeline that ingests remittance data from channels such as email, portals, EDI, PDFs, and scans, then normalizes those inputs, matches payments to open invoices, and posts the result back into the ERP (Esker on the cash application pipeline).

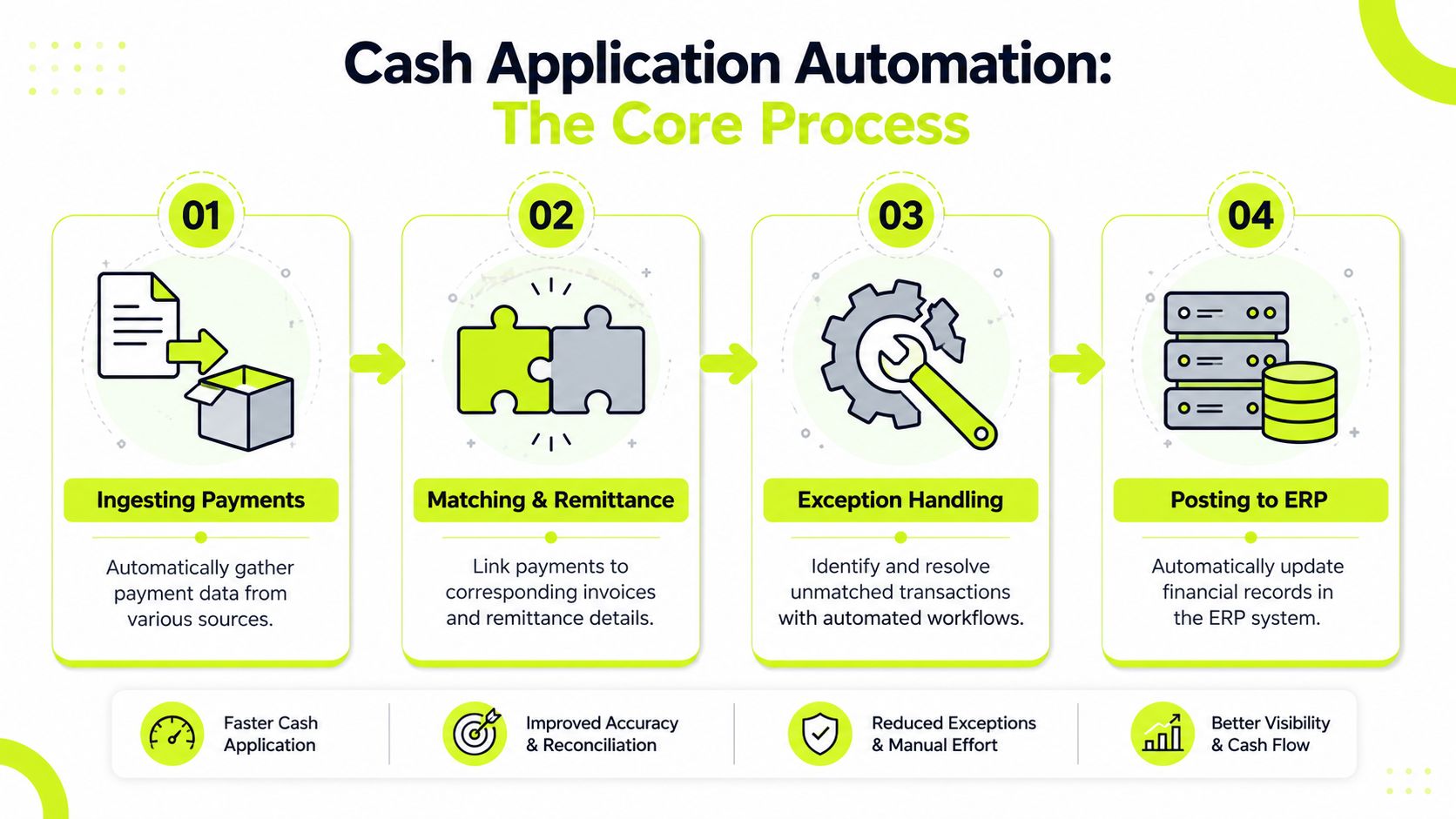

The four operating steps

Think of good cash application automation as a digital analyst that never gets tired of repetitive matching work.

- Ingesting payments The system pulls payment and remittance data from bank files, email inboxes, customer portals, PDFs, lockbox feeds, scans, and structured formats like EDI.

- Matching and remittance interpretation It extracts useful fields, ties payment amounts to the right customer record, and allocates funds across one or more invoices based on remittance details, historical behavior, and rules.

- Exception handling When something doesn't line up, the item doesn't vanish into a spreadsheet. It gets routed into a queue for review with context attached.

- Posting to ERP Once matched or approved, the transaction posts back to the ERP or accounting platform so AR, customer balances, and financial reporting stay current.

What makes it different from basic AR software

A lot of AR software helps with invoicing, reminders, or collections. That's useful, but it doesn't solve the final accounting bottleneck.

Cash application is the point where received money becomes correctly settled receivables. Until that happens, the order-to-cash cycle isn't closed. That's why a firm can have decent billing discipline and still struggle to improve cash flow. If payments arrive but don't get applied quickly and accurately, the reporting signal stays noisy.

Practical rule: Don't evaluate cash application tools on feature lists alone. Evaluate them on how they handle messy remittance, split payments, and posting accuracy inside your accounting workflow.

For professional services firms, this distinction matters because client billing is often less standardized than product invoicing. Retainers, milestone billing, multiple matters or projects, write-downs, credits, and cross-invoice payments all raise the matching burden.

Where AI actually helps

AI AR automation earns its place. Not because it sounds modern, but because many remittances are unstructured.

A useful system reads an email body, extracts invoice references from a PDF, recognizes naming variations, and connects the payment to the correct open items without a team member manually stitching it together. The practical gain isn't magic. It's less keying, less hunting, fewer avoidable errors, and a cleaner handoff for true exceptions.

That's the difference between automation that removes work and automation that relocates it.

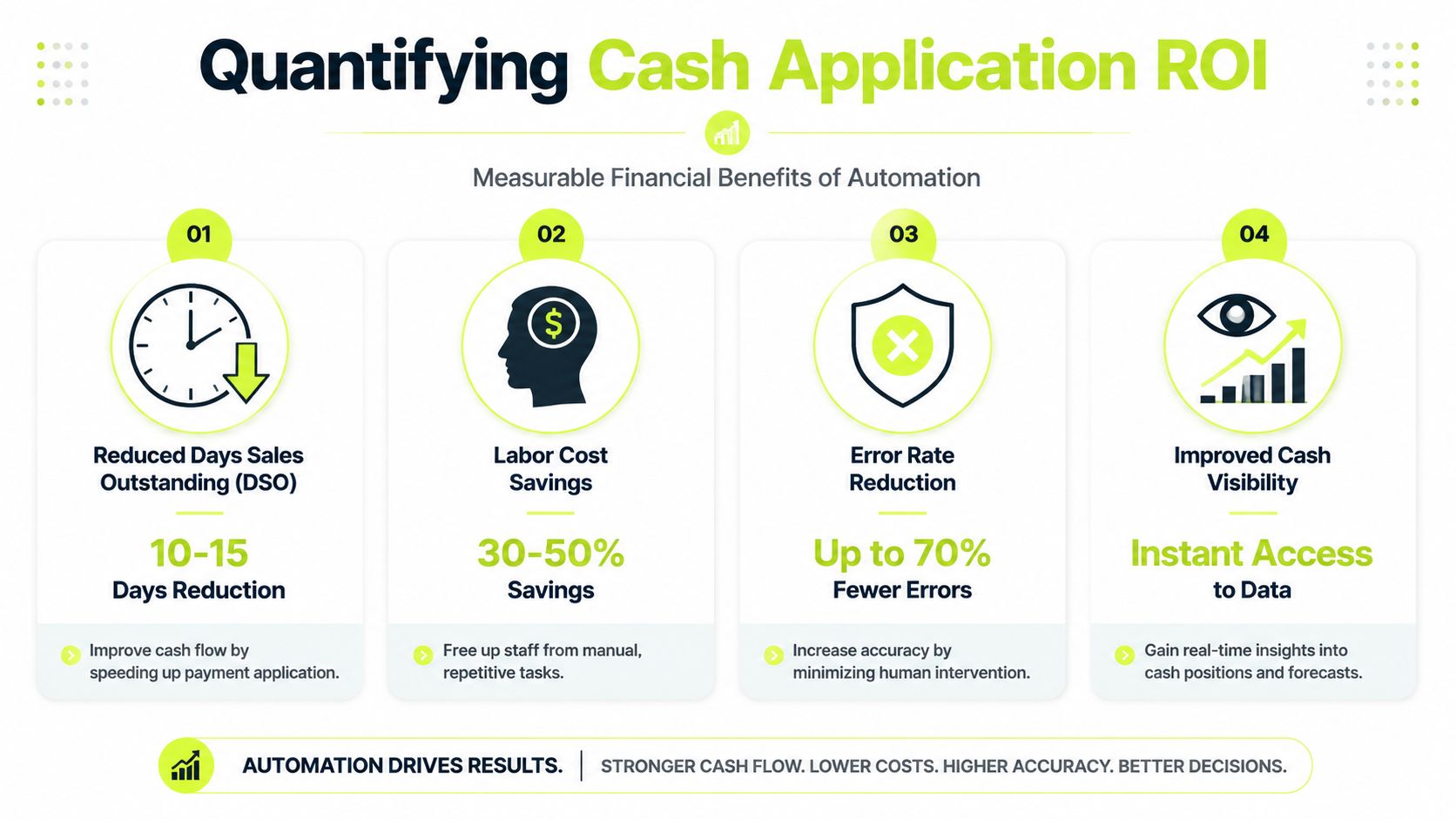

Calculating the ROI of Faster Reconciliation

Finance leaders don't buy cash application automation because matching is annoying. They buy it because delayed application distorts liquidity, slows follow-up, and consumes labor that should be spent on analysis.

The return starts with speed. Serrala notes that automated cash application can reconcile payments in minutes and supports same-day matching, while also reducing manual errors and low-value tasks across the order-to-cash cycle (Serrala on faster reconciliation and same-day matching).

The ROI categories that matter

For a CFO or controller, the business case usually lands in four buckets.

ROI area | What improves | Why it matters |

|---|---|---|

Cash visibility | Faster posting of received funds | Forecasts rely less on stale AR data |

DSO pressure | Payments stop sitting unapplied | Collected cash is reflected sooner in receivables reporting |

Labor leverage | Less manual reconciliation and rework | Finance time shifts toward exception resolution and analysis |

Control quality | Better routing, audit trail, and consistency | Fewer avoidable errors and cleaner close processes |

The point isn't that every firm will see the same outcome. The point is that cash application affects metrics finance already watches.

How faster posting helps reduce DSO

You can't credibly talk about how to reduce DSO if customer payments are still waiting to be applied.

When incoming cash sits in unapplied status, AR aging overstates what is outstanding. Collections activity gets misdirected. Client conversations become less precise. Same-day application shortens the lag between payment receipt and invoice settlement, which improves the quality of DSO reporting and makes collections action more targeted.

Ramp frames the operational benchmark clearly: a practical target is same-day application of incoming payments rather than waiting days for manual reconciliation, because AI and machine learning can process remittance data in real time and route only exceptions to human review (same-day application as the practical benchmark).

The less obvious financial return

The harder cost to notice is decision drag.

If partners or owners don't trust AR status, they hold cash longer, delay distributions, or stay conservative on hiring because they're unsure what has really been collected. That uncertainty has a cost even when no one books it to a line item.

A clean reconciliation process also improves how teams talk to clients. If a payment was made but misapplied, the relationship cost lands on the client side first. Few things erode confidence faster than a polite collection note sent to someone who already paid.

For firms reviewing adjacent workflows, this connects naturally with broader automated payment reconciliation practices because the strongest ROI comes when payment data, invoice data, and accounting records move together instead of being fixed in batches after the fact.

Faster cash application doesn't create cash from nowhere. It makes received cash visible, usable, and governable sooner.

That's why the ROI case is stronger than “we'll save some admin time.” It's really about more dependable working capital control.

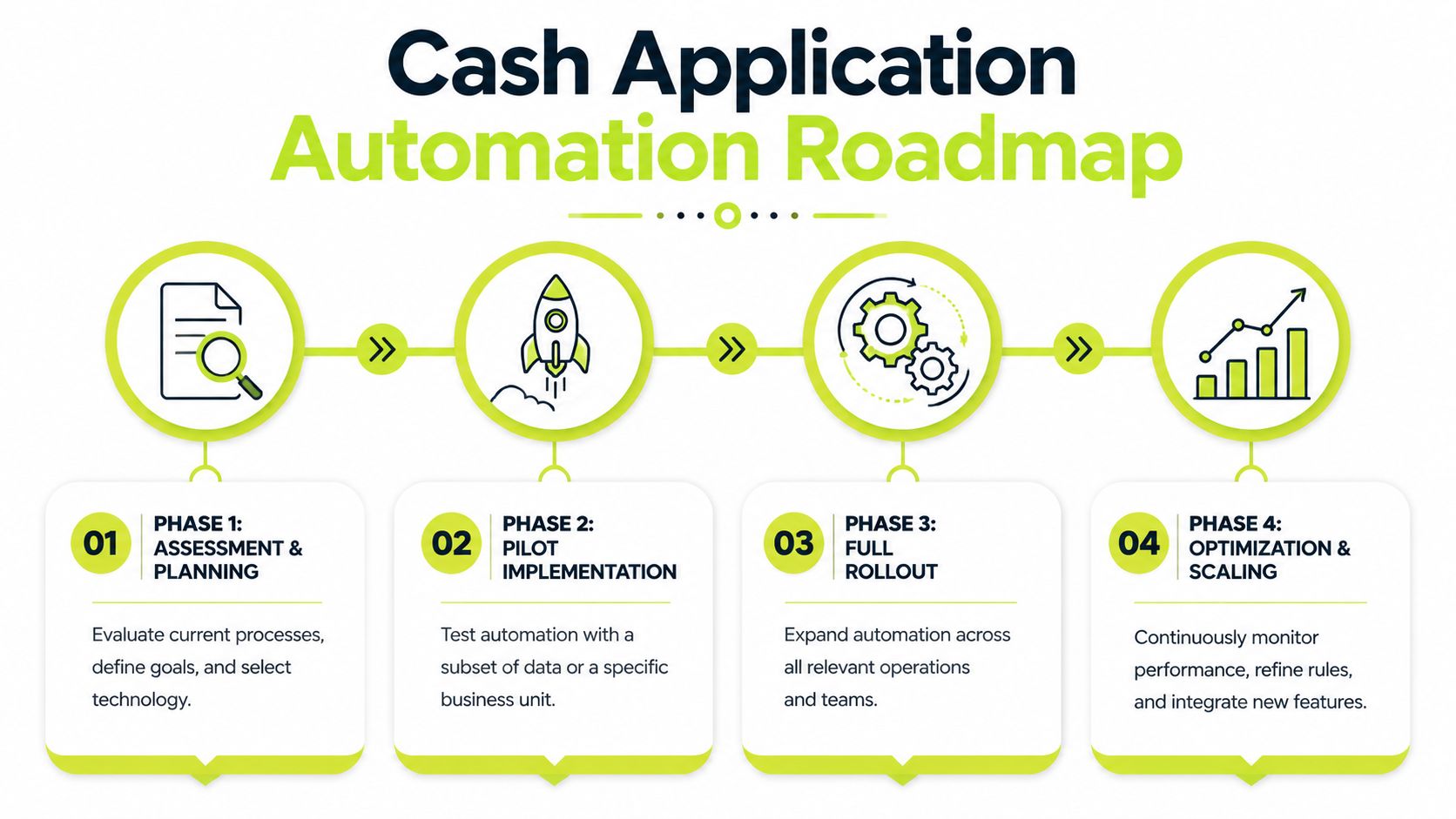

A Phased Approach to Automated Cash Application

Most finance teams don't need a grand transformation plan. They need a controlled rollout that doesn't interrupt billing, collections, or close.

The mistake is treating cash application automation like a pure software install. In practice, it's an operating model change. Paystand notes that many vendors say automation integrates easily with ERPs, but the more practical issue is how finance leaders measure readiness, decide which customers or payment types to automate first, and manage controls once the system is live (Paystand on readiness, ERP complexity, and governance).

Phase 1 assessment and process baseline

Start by documenting the current path from payment receipt to posting.

Map where remittance arrives, who touches it, what systems are involved, and where exceptions stall. In a professional services firm, that often means looking beyond finance. Project managers, account leads, or admins may be holding information the AR team needs.

Focus on questions like these:

- Where does remittance break down most often Email inboxes, client portals, lockbox files, and partial payments are common failure points.

- Which payment types are easiest to automate first Clean ACH remittances usually behave differently than bundled wires or client deductions.

- What has to stay under human review Credits, write-offs, dispute-related short pays, and nonstandard allocations often need policy-based approval.

Phase 2 vendor fit and integration reality

Many teams get seduced by demos.

For AR software for professional services, the right question isn't whether the tool can match invoices in ideal conditions. Ask how it handles multi-invoice payments, partial allocations, client-specific billing structures, and sync back to your accounting platform. If you're on QuickBooks, ask direct questions about QuickBooks AR automation, posting logic, customer mapping, and what happens when data is incomplete.

A useful shortlist usually includes criteria such as:

- ERP and ledger sync Can it post accurately without creating cleanup work downstream?

- Exception workflow Does the system route issues with enough context for fast resolution?

- Auditability Can your team see what was matched automatically, what was overridden, and why?

- Human-in-the-loop controls Can finance set approval thresholds and review rules?

One example in the market is Resolut, which handles AR orchestration including cash application inside a broader workflow for invoicing, collections, and payment activity. For some firms, an integrated approach is useful because cash application works better when it isn't isolated from the rest of AR operations.

Phase 3 pilot before broad rollout

Don't start with every client and every payment source.

Pick a contained segment. That might be clients who pay by ACH with relatively consistent remittance, or one business unit with enough volume to learn from but not so much complexity that the pilot stalls. A pilot should prove workflow, exception routing, and posting quality.

This is also the right point to define what good straight-through processing looks like in your environment. Teams evaluating broader straight-through processing in finance operations often find that the best pilot scope is narrow enough to control but broad enough to expose real exception patterns.

Phase 4 optimization after go-live

Go-live isn't the finish line. It's the start of tuning.

Review exception queues, update customer-specific rules, tighten approval policies, and retrain staff responsibilities around oversight rather than manual entry. Good implementations get better over time because the team learns where the process needs rules and where it needs judgment.

Navigating Common Cash Application Challenges

The fastest way to undermine a cash application project is to assume automation will eliminate mess. It won't. It will expose it.

HighRadius makes the point well: automation is most valuable not when it removes every manual step, but when it turns exception handling into a smaller, governed workflow that still requires policy design, auditability, and human override (HighRadius on exceptions, governance, and human review).

Exception-heavy environments need operating rules

In such scenarios, optimism usually outruns reality.

Short-pays, deductions, multi-invoice remittances, unapplied credits, and payments with weak references still need decisions. A tool can surface likely matches and route work intelligently, but finance still needs policy. Who approves allocation when a client pays less than billed? When does AR hold cash unapplied versus forcing a match? When does the issue move to billing, collections, or client service?

If your exception policy is vague, automation scales confusion faster than manual work ever could.

For many firms, this is closely tied to broader bank account reconciliation discipline. The cleaner your reconciliation controls, the easier it is to trust automated posting and isolate true exceptions quickly.

Data quality still decides the outcome

Bad customer master data creates false confidence.

If payer names don't align, invoice references are inconsistent, or customer records have duplicates, even a strong automation layer will spend too much time guessing. Before expanding automation, tighten naming conventions, invoice reference standards, and customer hierarchies. This is less glamorous than buying software, but it usually produces the cleaner result.

A practical checklist:

- Standardize remittance instructions Put clear invoice reference expectations on bills and payment communications.

- Clean customer records Merge duplicates and define ownership for maintaining account data.

- Review posting rules regularly What worked for one client segment may create errors in another.

Team roles have to change too

Automation changes AR jobs. That's not a side effect. It's the point.

The best teams stop spending most of their time keying and hunting, and spend more of it reviewing exceptions, resolving disputes, and improving process rules. Controllers should prepare for that shift early. Training should focus on judgment, escalation, and control review rather than only on system clicks.

“The team still matters. The work just moves up the value chain.”

That's the healthier model. You don't remove finance from cash application. You give finance a cleaner, more controlled field of work.

From Manual Task to Strategic Advantage

At month-end, the damage shows up fast. Cash is in the bank, but it is still sitting in unapplied cash, open invoices look older than they are, collectors call clients who already paid, and the CFO gets a weaker view of near-term liquidity than the business has.

That is why cash application belongs in working capital discussions, not just AR operations.

Applied cash drives more than ledger hygiene. It affects DSO, short-term cash forecasting, the credibility of AR reporting, and the quality of client communication. A firm that clears receipts quickly can see exposure sooner, escalate real disputes faster, and avoid creating friction with clients over balances that should already be closed.

The strategic gain is control. Controllers need to know which receivables are overdue, which cash is pending identification, and where exception volume is rising by payer, channel, or business unit. Automated cash application gives that visibility in time to act on it. Manual processing usually delivers it after the fact, once collection effort has already been misdirected or a forecast has already missed.

There is also a service issue here. Clients expect accurate statements and clean account status. When posting lags, the firm creates unnecessary noise: duplicate reminders, avoidable calls, and preventable disputes. Those errors do not look like a cash application problem to the client. They look like a finance team that does not have control of the account.

For controllers and CFOs, the case is straightforward. Cash application automation improves reporting discipline, strengthens working capital control, and reduces avoidable strain on customer relationships. If your firm is also reviewing payment operations through a compliance lens, resources on Texas MCA compliance with HB700 can be useful because payment automation and control design often intersect more than teams expect.

Resolut automates AR for professional services. Consistent, accurate, and human. If you're evaluating a more controlled approach to accounts receivable automation, including cash application, you can learn more at Resolut.