Credit Control Debt Collection: A CFO’s Guide to Cash Flow

Master credit control debt collection. A guide for CFOs on reducing DSO and improving cash flow with AR automation, policy design, and technology.

Professional services firms don’t usually fail on revenue. They get squeezed on timing.

Globally, 1 in 10 invoices go unpaid, creating a large administrative burden for finance teams and firm owners trying to turn delivered work into collected cash, as noted in Credit Control’s FAQ discussion of AR automation gaps. In a consulting firm, law firm, engineering practice, or agency, that pressure shows up in familiar ways. Partners hesitate to push a good client. Project leads promise “it’s being handled.” Finance sends reminders manually, inconsistently, and too late.

That isn’t really a collections problem. It’s a system problem.

When firms talk about credit control debt collection, they often collapse two different disciplines into one messy activity. The result is predictable. Invoices age unaddressed, client conversations become awkward, and the finance team ends up reacting instead of controlling the process. The firms that handle this well do something simpler. They build a repeatable credit-to-cash motion that starts before the invoice goes out and continues through payment, escalation, and reconciliation.

The shift matters because AR isn’t just an accounting function. It affects hiring, partner draws, tax planning, and how confidently you can take on new work. If your billing is strong but your follow-through is loose, your reported profitability can look fine while your cash position says something else.

Strong firms don’t wait for an invoice to become a problem before deciding how they’ll handle it.

Manual follow-up also carries a relationship cost that professional services firms often underestimate. A scattered reminder sent by the wrong person can do more damage than a firm, well-timed note from finance. Clients don’t mind structure nearly as much as they mind confusion.

Introduction The Unseen Drag on Your Firm's Profitability

In a product business, late payment is often a volume issue. In a professional services firm, it’s more personal.

Your invoice usually follows weeks or months of partner attention, delivery meetings, revisions, and trust-building. That makes overdue AR harder to manage. Teams start treating payment follow-up as a client sensitivity issue rather than a normal commercial control. Once that happens, receivables stop being governed by process and start being governed by whoever feels least uncomfortable making the next call.

That’s the drag on profitability most firms don’t see clearly enough. It isn’t only the unpaid invoice. It’s the partner time spent chasing context. It’s the controller cleaning up payment status manually. It’s the missed chance to reduce DSO through discipline instead of pressure.

Why this hits service firms differently

Professional services firms sit in an awkward middle ground.

You aren’t a consumer lender with industrial collection machinery. You also aren’t a giant enterprise with specialized AR teams segmented by risk, region, and account size. In a $3M to $50M firm, AR usually lives between finance, operations, and partner relationships. That makes consistency harder, unless you deliberately design it.

A few operational realities make this worse:

- Services are intangible. Clients can question scope, timing, or value after delivery.

- Invoices often reflect milestones or retainers. That creates more room for misunderstanding if terms weren’t tight upfront.

- Relationship owners often outrank finance. If partners override process informally, collections discipline weakens fast.

- Manual reminders create tone problems. A rushed email can sound either apologetic or aggressive. Neither helps.

The real fix is control, not aggression

Most overdue AR in professional services doesn’t require a hard collections posture first. It requires clearer expectations, cleaner invoicing, better timing, and a defined escalation path.

That’s why the useful frame isn’t “how do we collect harder?” It’s “how do we create a payment environment where fewer invoices drift at all?” Once you approach credit control debt collection that way, the work changes. You stop improvising. You start operating.

Credit Control and Debt Collection The Two Sides of AR

Credit control and debt collection belong to the same workflow, but they are not the same job.

The easiest way to think about it is this. Credit control is preventative care. Debt collection is emergency surgery. If your firm relies on the second to compensate for weak execution in the first, you’ll create more friction, more write-offs, and more partner frustration than you need to.

The broader environment makes that distinction more urgent. By the end of 2023, total U.S. consumer debt reached US$17.50 trillion, up from US$17.05 trillion in Q1, and credit card balances rose by US$143 billion to US$1.13 trillion. The third-party collections market was valued at US$20.2 billion, employing around 140,000 people, while the CFPB received 109,900 debt collection complaints in 2023, with companies responding in 97% of cases, according to these debt collection industry figures. That data is consumer-focused, but the operating lesson translates cleanly to B2B. Once payment issues scale, process quality matters as much as persistence.

What credit control actually covers

Credit control starts before work begins.

It includes the commercial decisions and operating habits that make timely payment more likely. In a firm environment, that usually means client vetting, engagement letter terms, billing triggers, invoice accuracy, reminder cadence, payment methods, and internal ownership. If those elements are loose, collections become reactive by default.

A practical credit control setup usually includes:

- Client acceptance standards that determine who gets standard terms, who prepays, and who needs closer monitoring

- Clear commercial terms written into engagement letters, not buried in old email threads

- Accurate invoicing discipline so clients don’t get easy reasons to delay

- Structured follow-up before and immediately after due dates

- Defined internal escalation so overdue accounts don’t stall between finance and relationship owners

If you want a useful outside read on how firms assess payment risk earlier, NILG.AI’s insights into AI applied to credit scoring is a good primer on how data can support better front-end decisions. For a practical internal framework, this guide to credit worthiness is also useful for tightening onboarding logic.

Where debt collection begins

Debt collection starts after your normal credit controls have failed or been ignored.

That doesn’t automatically mean legal action or sending an account to an agency. It means the account has moved from routine payment management into structured recovery mode. The tone changes. The documentation burden rises. The relationship owner can’t be the sole decision-maker anymore.

Practical rule: If finance can’t tell you, in one sentence, why an invoice is unpaid and who owns the next step, you’re no longer managing AR. You’re managing ambiguity.

The operator’s trade-off

Good credit control protects the relationship by making payment routine. Debt collection risks the relationship because it introduces pressure.

That’s why mature firms design their process so the client feels consistency early and firmness later, not surprise throughout. You don’t preserve trust by avoiding payment conversations. You preserve trust by making those conversations normal, clear, and professionally handled.

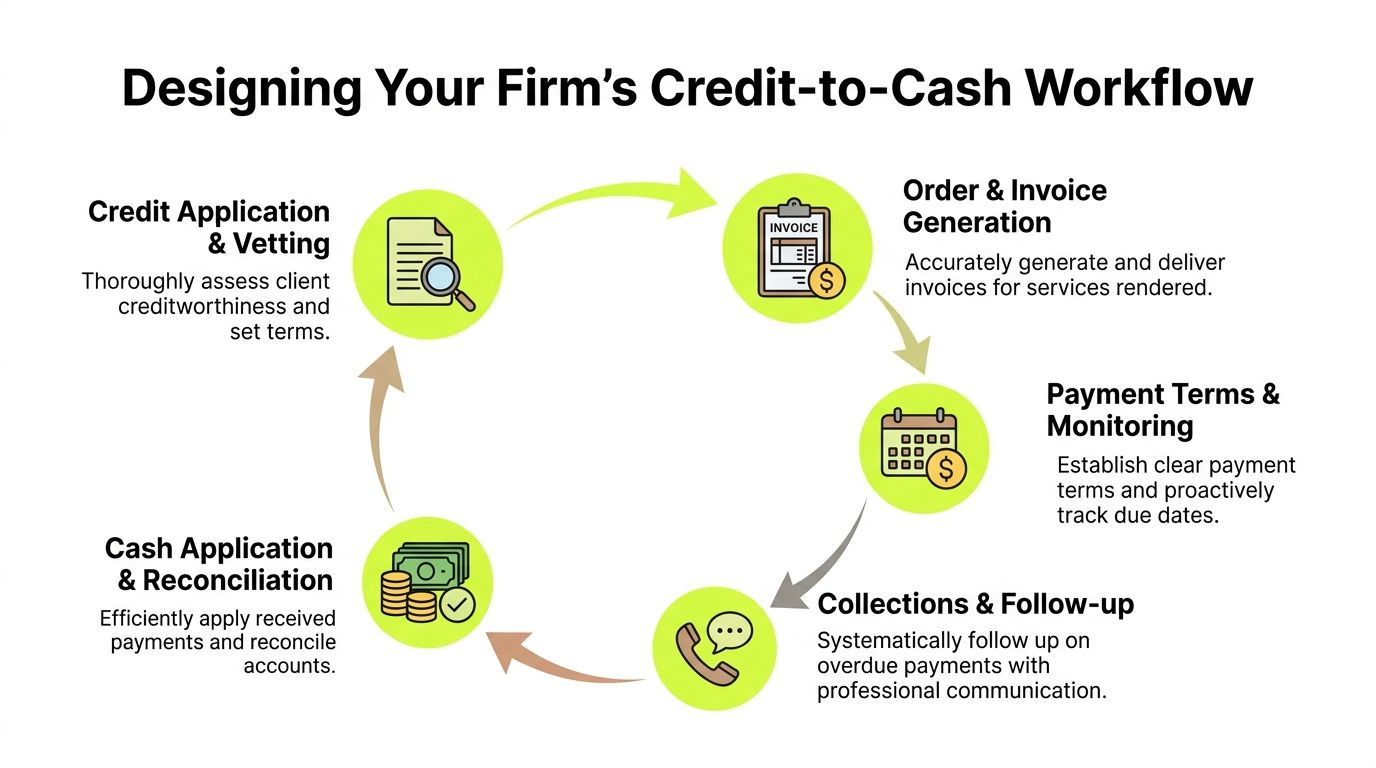

Designing Your Firm's Credit-to-Cash Workflow

A workable AR process for a professional services firm should feel boring in the best way. The team knows what happens at onboarding, at billing, before due date, after due date, and at escalation. No one is guessing. No one is waiting for a partner’s memory of “how we usually handle this client.”

Start at client onboarding

Most AR problems begin before the first invoice.

If your engagement letter is vague on billing cadence, approval expectations, retainer treatment, or who receives invoices, the collections team inherits avoidable friction. Finance should have a seat in onboarding for any client that falls outside normal terms.

Use a simple decision structure:

- Confirm legal entity and billing contacts. Don’t rely on the partner’s main relationship contact alone.

- Set terms deliberately. Standardize where you can. Make exceptions visible and approved.

- Clarify billing triggers. Monthly, milestone, retainer replenishment, expense pass-through, or completion billing should be explicit.

- Document dispute windows. Clients should know when they need to raise invoice concerns.

Tighten invoice generation

A late invoice and a disputed invoice often produce the same cash result.

That’s why “send the bill” isn’t enough. Invoice quality matters. Descriptions should be clear enough for the client’s AP team, while still matching the engagement economics your team expects. In professional services, line-item confusion creates easy delay.

A clean invoice process includes:

- Consistent descriptions that align with statement of work language

- Named client references such as matter, project, or cost center where relevant

- Visible due date and payment methods

- Fast issuance after work or milestone completion

- Internal review rules for large or nonstandard bills

The best time to collect an invoice is often before the client has mentally closed the workstream.

Build a follow-up cadence before trouble starts

Many firms wait until an invoice is overdue to make first contact. That’s too late.

Credit control works better when communication starts as a normal payment support function, not a recovery event. A reminder a few days before due date feels operational. A reminder sent weeks after due date feels corrective.

Here’s a practical cadence for service firms:

Stage | Typical owner | Tone | Purpose |

|---|---|---|---|

Invoice sent | Billing or AR | Clear and helpful | Confirm receipt and payment instructions |

Pre-due reminder | AR automation or finance | Neutral | Reduce “we missed it” delays |

Early overdue follow-up | Finance | Professional and direct | Confirm status, surface issues quickly |

Escalation to relationship owner | Finance plus partner | Controlled | Resolve blockers without mixed messages |

Final internal review | Controller or CFO | Decisive | Choose hold, plan, or escalation |

Define escalation triggers

Escalation should be rule-based, not personality-based.

If a client misses one invoice but communicates clearly, that’s different from a client who goes silent, disputes late, or repeatedly pays only when chased. Your workflow should distinguish between a temporary delay and a pattern.

Useful triggers include:

- Silence after multiple touches

- Repeated partial payments without plan

- Frequent invoice disputes raised only after due date

- Requests for ongoing work while prior balances remain unresolved

- Partners asking finance to “give it another week” without client confirmation

Close the loop with cash application

Many firms think the AR process ends when payment lands. It doesn’t.

Cash has to be applied correctly, unapplied balances investigated, and account status updated quickly enough that teams don’t keep chasing already-paid invoices. In smaller firms, sloppy reconciliation creates embarrassment faster than weak reminders do.

A disciplined credit-to-cash workflow keeps one truth visible at all times. What’s due, what’s disputed, what’s promised, and who owns the next action.

Building Your AR Policies and Communication Playbooks

A workflow without policy turns into preference. One partner wants to be flexible. Another wants finance to “be tougher.” A third doesn’t want reminders sent without approval. That’s how firms end up treating similar clients differently for no commercial reason.

Good AR policy reduces that noise. It gives finance cover to act consistently and gives partners a clear operating boundary.

What belongs in the policy

Your policy doesn’t need legalistic language to be effective. It needs to be usable.

At minimum, define these items in writing:

- Payment terms. State your standard terms and who can approve exceptions.

- Invoice timing. Specify when invoices go out after work completed or milestones met.

- Accepted payment methods. Reduce friction by making payment easy and visible.

- Dispute handling. Require clients to raise billing questions promptly and through a named contact.

- Escalation ownership. Make clear when AR owns communication, when partners step in, and when the controller or CFO takes over.

- Work continuation rules. Decide when the firm pauses new work, slows delivery, or requires a retainer refresh.

One point matters more than most firms admit. Policies must govern internal behavior, not just client behavior. If partners can override payment discipline informally, the written policy won’t survive first contact with a sensitive account.

The tone professional services firms need

The tone for credit control debt collection in a law firm, consultancy, or agency can’t sound like consumer collections language. It also can’t sound tentative.

The right tone is calm, specific, and assumption-light. You’re not accusing the client. You’re documenting expectations and moving the process forward.

Late-payment communication should sound like a controlled business process, not a personal complaint.

Sample email playbooks

Use templates so your team isn’t rewriting tone under pressure. The wording should tighten as delinquency increases, but the voice should stay professional.

Before due date

Subject: Invoice [number] due on [date]

Hi [Name], Sharing a quick reminder that invoice [number] is due on [date]. Please let us know if your team needs any supporting documentation or a copy of the invoice resent. Payment details are included below for convenience.

Just past due

Subject: Follow-up on invoice [number]

Hi [Name], I’m following up on invoice [number], which is now past due. Please confirm payment status when you can. If there’s a billing question or approval issue on your side, send it through and we’ll help resolve it quickly.

Escalated overdue account

Subject: Action needed on outstanding balance

Hi [Name], We’re reviewing the status of your outstanding balance and need to align on payment timing. Please confirm whether payment is scheduled or if there’s an issue we should address. If needed, we can also coordinate directly with your AP contact to close this out.

Notice what these do not do. They don’t threaten, overexplain, or apologize for asking to be paid.

Phone and internal handoff scripts

Phone calls matter most when email stops producing clarity. But they should be structured.

A finance caller should know:

- What they need. Payment date, dispute detail, AP contact, or escalation confirmation.

- What they won’t debate live. Scope disagreements, partner promises, or undocumented special terms.

- What gets documented immediately. Commitment date, reason for delay, and next owner.

For partner handoffs, keep the internal note short:

Invoice [number] remains unpaid. Finance sent reminders on schedule. Client hasn’t confirmed payment date. Please reinforce commercial terms and direct them back to finance for payment coordination.

Policy works when exceptions are visible

The firms with the strongest collections rhythm aren’t the firms with zero exceptions. They’re the firms where every exception is named, approved, and monitored.

Create a short exception log. If a client has extended terms, staged catch-up payments, or temporary billing holds, record it in one place. Otherwise, AR gets blamed for inconsistency that stemmed from informal side deals.

Measuring What Matters Key AR KPIs for CFOs

Most AR reporting is too shallow to be useful. Firms look at total receivables, maybe glance at aging, and decide whether things feel under control. That’s not enough if you’re trying to reduce DSO or improve cash flow in a predictable way.

The KPIs that matter should answer three questions. How much cash is stuck, how well is the team collecting what became due, and where is the risk building.

DSO tells you the pressure level

DSO is still the headline number because it translates AR performance into time. For a CFO or controller, that makes it operational. If DSO is drifting upward, cash conversion is slowing and your firm is funding clients longer than intended.

DSO alone has limits, though. It can worsen because billing surged late in the period. It can also look stable while older balances deteriorate unnoticed. That’s why DSO should be read alongside aging and collection effectiveness, not by itself.

A practical read of DSO in professional services looks like this:

- Stable but consistently high DSO often points to tolerated delay becoming normal

- Sudden DSO movement can indicate billing process changes, disputes, or weaker follow-up discipline

- Improving DSO with rising disputes may signal that collections pressure is masking invoice quality issues

CEI shows whether your process is working

Collection Effectiveness Index, or CEI, is one of the more useful operating measures because it isolates collection performance during the period.

The formula is: CEI = (Amount Collected) ÷ (Total Receivables Due) × 100, with the important adjustment that teams should subtract any opening balance already past due from collections to avoid double-counting, as explained in this CEI guide for credit control teams.

That denominator detail matters. CEI is more precise than a basic collection rate because it focuses on what was available to collect in the period. According to the same source, a 5-10% quarterly CEI improvement typically precedes 2-3 day DSO reductions within 60-90 days.

A firm can celebrate strong billings and still have weak collection execution. CEI helps separate those two realities.

Aging is your early warning system

An aged receivables report is where finance sees behavior, not just totals.

The report should be reviewed by client, partner, and aging bucket. In a service firm, that often reveals that AR issues aren’t evenly distributed. One practice area may invoice late. One partner may tolerate extensions. One client segment may always pay only after a personal nudge.

Look for patterns such as:

- Current invoices that never convert cleanly into paid status

- Accounts that keep rolling from one aging bucket to the next

- Disputed invoices clustered around certain teams or matter types

- Large balances with no documented next step

Use KPIs to manage action, not just reporting

The point of AR metrics isn’t a prettier dashboard. It’s faster intervention.

A useful review rhythm ties each KPI to a decision. Rising DSO should trigger root-cause review. Weak CEI should trigger cadence and ownership checks. Aging concentrations should trigger account-specific action plans. That’s how measurement turns into control.

The Role of Technology in AR Automation

Manual AR breaks down in the same places again and again. Reminders depend on who remembers. Notes sit in inboxes. Payment promises aren’t logged well. Partners step in late. Finance spends too much time coordinating, not collecting.

That’s where accounts receivable automation changes the operating model. Not because software sends emails. Any basic tool can do that. Its primary value is that automation standardizes timing, captures account history, reduces handoff errors, and gives finance a way to act early without sounding robotic.

What good AR software actually does

For a professional services firm, AR software for professional services should support the way your clients buy and pay, not force you into generic consumer collections behavior.

The useful features usually include:

- Automated reminder workflows tied to due dates and aging status

- Integrated payment options so clients can act when they receive the message

- Shared account timelines so finance, operations, and partners see the same status

- Cash application support to reduce manual reconciliation

- ERP or accounting integration, including QuickBooks AR automation where relevant

- Role-based escalation so the right internal person gets involved at the right time

One option in this category is automated debt collection software, which describes how coordinated workflows, outreach, and reconciliation can be handled in one system rather than across spreadsheets, inboxes, and accounting records.

Where AI AR automation becomes useful

The bigger step is AI AR automation.

Predictive collections models don’t just flag that an invoice is overdue. They estimate likely payment behavior in the next 30-90 days, helping teams decide which accounts need human contact and which can stay in automated email or SMS flows, based on FICO’s overview of predictive analytics in debt collection. The same source notes that this lets teams reserve phone outreach for high-probability accounts while automating lower-cost channels for others, reducing cost-per-recovery by 40-60% while maintaining or improving total recovery dollars.

In a service firm, that matters because phone outreach is expensive in two ways. It consumes staff time, and it uses relationship capital. If the model says an account is likely to pay with lighter-touch follow-up, there’s no reason to escalate voice contact prematurely.

A short walkthrough helps here:

Automation should reduce friction, not add distance

Some CFOs resist automation because they think it will make client communication feel cold. That only happens when the workflow is poorly designed.

The best systems separate routine communication from high-value intervention. Routine notices stay consistent, timely, and easy to pay from. Human involvement is saved for exceptions, disputes, and strategic accounts. That’s better for clients and better for staff.

If voice outreach is part of your mix, it’s worth understanding how automated outbound call software can support structured call operations without turning the experience into a blunt robocall exercise. In practice, service firms need controlled call triggers and documented follow-up, not high-volume noise.

Selection criteria that matter

When evaluating tools, focus on operational fit.

Ask whether the system can:

- Support segmented workflows by client type, balance profile, or partner sensitivity

- Integrate with your accounting stack without creating duplicate records

- Handle omnichannel communication while preserving a clean audit trail

- Adapt message tone and timing by account status

- Surface risk early instead of only reporting delinquency after it exists

If the software only automates reminders, you’ll save some time. If it orchestrates the full credit control debt collection workflow, you’ll improve control.

The Final Escalation Path Legal and Third-Party Recourse

By the time an account reaches formal escalation, your main question isn’t “can we pursue this?” It’s “should we?”

That decision needs commercial judgment, not frustration. In U.S. state courts, debt collection lawsuits reached pre-pandemic highs, with up to 4.7 million cases filed in 2022. In places such as Utah and Minnesota, about half of those cases involved debts under $2,000, according to Pew’s analysis of state debt collection lawsuits. The lesson for a professional services firm is clear. Legal collection systems process volume, but they can be a poor fit for relationship-sensitive, documentation-heavy service disputes.

When third-party collections make sense

A third-party agency can be appropriate when the account is clearly due, internal follow-up has been exhausted, and the relationship is no longer strategic enough to justify continued internal effort.

That said, agencies change the tone immediately. Even when they operate professionally, the client understands the relationship has moved into a different phase. For many firms, that’s acceptable only after internal senior review.

A useful decision screen includes:

- Clarity of debt. Is the invoice undisputed and properly documented?

- Client value. Is this a former client, a one-off matter, or an ongoing strategic account?

- Balance profile. Is the amount worth external handling after fees and internal time?

- Future work risk. Are you prepared for the commercial consequence if the client relationship ends?

If you’re comparing options, this overview of an AR collection agency is a useful operational primer on where agencies fit and where they don’t.

Legal action is a business decision first

Litigation can be appropriate, but it is rarely efficient as a default path for service firms.

Before counsel gets involved, finance should confirm that the file is clean. Signed engagement terms, invoice history, communication logs, dispute records, and proof of work completion all matter. Weak documentation turns a payment issue into a credibility issue.

For firms that need help organizing matter files and support work before escalation, using experienced Legal assistants can be practical, especially when the issue is document preparation and process coordination rather than immediate courtroom action.

The strongest escalation strategy is the one you rarely need because earlier controls are doing their job.

Treat escalation as a feedback signal

If too many accounts are reaching agencies or lawyers, don’t just review the delinquent accounts. Review the upstream process.

In most firms, repeated legal escalation points back to one of a few causes. Weak client vetting. Loose engagement terms. Inconsistent invoicing. Slow follow-up. Or partners bypassing policy. Fix those, and final-stage recovery becomes the exception it should be.

Conclusion From Reactive Collections to Proactive Control

Professional services firms don’t need louder collections. They need better control.

When the AR function is working, clients receive clear terms, accurate invoices, timely reminders, and consistent follow-up. Finance knows which accounts are routine, which are drifting, and which need intervention. Partners aren’t improvising payment conversations in parallel. Cash becomes more predictable because the process is.

That’s the practical shift behind stronger credit control debt collection. Move from reactive chasing to defined workflow. Replace ad hoc partner judgment with policy. Track DSO, CEI, and aging as operating signals, not just report lines. Use technology where it removes manual drag and preserves the tone your client relationships require.

For firms in the $3M to $50M range, that shift is often worth more than another round of revenue optimization. It reduces admin load, improves cash flow, and gives leadership a firmer grip on planning. You don’t have to choose between being disciplined and being human. The right AR system does both.

Resolut automates AR for professional services with a focus on consistency, accuracy, and a human tone. If you’re reworking billing, follow-up, and cash application to reduce DSO without damaging client relationships, Resolut is worth a look.