Credit Risk Analysis Using Machine Learning: A CFO's Guide

CFOs: Master credit risk analysis using machine learning to reduce DSO & boost cash flow with our AR automation framework.

You can feel the problem before you see it in the reporting.

Revenue is up. Utilization looks healthy. The team shipped the work. But cash lands late, several clients drift past terms at the same time, and your finance staff spends too many hours chasing invoices that should have been straightforward. In a professional services firm, that gap between earned revenue and collected cash creates avoidable strain.

For most firms in the $3M to $50M range, receivables risk still gets managed by memory, tribal knowledge, and a few spreadsheet filters. Someone in finance knows which client always pays after a reminder. Someone in operations knows which matter tends to trigger billing disputes. Someone in leadership has a gut feel about who should get flexible terms. That works until it doesn't.

Credit risk analysis using machine learning gives finance leaders a more disciplined way to act earlier. Not as an academic modeling exercise. As a control layer inside accounts receivable automation, AI AR automation, and billing operations. The useful question isn't whether a model can produce an elegant risk score. It's whether your team can use that score to reduce DSO, improve cash flow, and make better collection decisions without damaging client relationships.

Moving Beyond Guesswork in Accounts Receivable

A familiar scenario: you close a strong month, issue invoices on time, and still walk into the next cash meeting with too much uncertainty. A handful of clients are moving from current to aging. Two accounts are disputing line items. One large customer hasn't answered follow-ups. None of this looks catastrophic on its own. Together, it changes how much cash you can trust.

That is where most receivables teams get stuck. They react after invoices age instead of identifying risk while there is still room to influence behavior.

What changes when risk is scored earlier

A machine learning approach to credit risk doesn't replace finance judgment. It sharpens it. The system looks at patterns your team already sees in pieces, then scores accounts or invoices based on signals that tend to show up before payment trouble becomes obvious.

In practice, that means:

- Earlier intervention: Finance can flag a client for outreach before the invoice crosses into serious aging.

- Better prioritization: Collectors stop treating every overdue account the same way.

- Cleaner escalation: Controllers can separate temporary delay from genuine deterioration in payment behavior.

- Tighter forecasting: Cash projections improve when risk is assessed systematically instead of informally.

For firms that want a grounding in core credit controls before layering in automation, this guide to small business credit risk management is a useful companion.

Practical rule: If your collections process starts at day 31, you're already late. The best AR systems identify risk when the invoice is created, approved, or first sent.

Why this belongs in finance operations

In banking, credit risk analysis using machine learning became a mainstream topic in the 2010s as lenders moved beyond traditional scorecards toward models that could capture non-linear patterns in large loan and payment datasets. FICO notes that modern models can learn relationships such as credit utilization and delinquency more flexibly than linear scorecards, while still preserving explainability through segmented scorecard ensembles in some designs (FICO on AI and machine learning for credit risk).

That matters to a professional services CFO because receivables risk also has interacting signals. A client's size by itself might not mean much. But size plus repeated billing disputes, slower approval cycles, and a change in project mix may be a meaningful warning pattern.

The point isn't to copy a bank's underwriting stack. It's to bring the same discipline into AR software for professional services. Good finance teams already ask the right questions. Which clients habitually pay late? Which invoices trigger delays? Which engagements are more dispute-prone? Machine learning helps answer those questions consistently, across the whole portfolio, every billing cycle.

What this looks like in the real world

A sound operating model is simple.

Your ERP or QuickBooks AR automation workflow sends invoice and payment data into a scoring layer. The model assigns a risk level. The AR process responds with the right action. Low-risk invoices move through standard reminders. Medium-risk invoices get earlier human review. High-risk invoices get tighter follow-up and, when needed, revised payment terms or escalation.

That is how you move from collections as cleanup to collections as prevention.

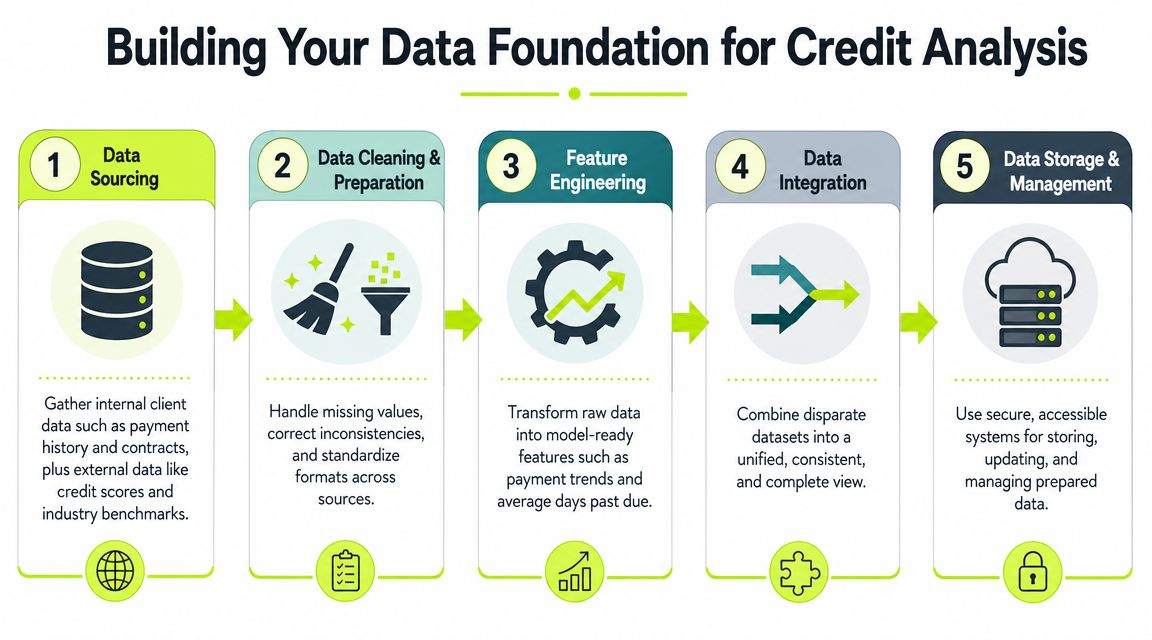

Building Your Data Foundation for Credit Analysis

Most firms already have enough internal data to start. The issue isn't data scarcity. It's fragmentation. Client details sit in the CRM. Billing history sits in QuickBooks or another accounting platform. Project attributes live in PSA or project management tools. Collections notes live in inboxes, spreadsheets, or the heads of your AR staff.

The model won't rescue messy process. It will expose it.

Start with the systems you already trust

For a professional services finance team, the first useful data map usually looks like this:

System | What to extract | Why it matters |

|---|---|---|

QuickBooks or ERP | Invoice dates, due dates, payment dates, credit memos, unapplied cash, aging | Core payment behavior |

CRM | Client segment, account owner, contract terms, renewal risk, buying center changes | Commercial context |

PSA or project tools | Project type, milestone billing, scope changes, approval delays | Delivery friction that affects payment |

Email and collections logs | Reminder timing, dispute frequency, response lags | Operational collection signals |

One operational upgrade that pays off quickly is better matching of payments to invoices. If your cash application is noisy, your model will learn from bad labels. This overview of automated payment reconciliation is relevant because reconciliation quality affects every downstream risk signal.

Build features finance can actually use

Feature engineering sounds technical, but the idea is straightforward. You convert raw records into usable indicators.

For services firms, the most practical features often include:

- Payment trend indicators: Average days to pay, recent deterioration, and variability by client.

- Invoice behavior: Aging by invoice type, partial payments, credit note frequency.

- Dispute patterns: Rebilling activity, write-down requests, approval bottlenecks.

- Commercial context: Industry, contract structure, retainer versus project work.

- Engagement complexity: Change orders, milestone dependencies, multiple approvers.

The point is not to create hundreds of variables because you can. It's to create a manageable set that captures payment behavior, billing friction, and client context.

Later, if you add external credit inputs or industry benchmarks, treat them as supplements, not substitutes. Internal payment behavior is often the most actionable signal because it reflects how your clients pay you.

A short walkthrough can help teams visualize the workflow before they formalize it:

Clean aggressively before you model

Finance teams often underestimate how much instability comes from data quality rather than model choice. If invoice dates are inconsistent, client names aren't normalized, or disputes aren't tagged consistently, the model starts learning noise.

One proven workflow comes from a Bank of Greece and BIS conference paper on probability-of-default estimation. The authors describe creating multiple data subsets, training base learners in parallel, combining their predictions, and using shadow features, which are shuffled versions of the original data, to remove variables that don't outperform random noise (Bank of Greece and BIS paper on ensemble workflow and shadow features).

If a real feature such as average days to pay can't beat its shadow version, remove it. It adds complexity without dependable signal.

That's a useful discipline for AR teams. Not every field in QuickBooks belongs in the model. Not every CRM attribute is predictive. A leaner set of stable features usually performs better in operations because finance can understand it, maintain it, and explain it.

A practical build order

Use this sequence if you're implementing credit risk analysis using machine learning inside AR operations:

- Unify invoice and payment history at the client and invoice level.

- Define what “bad outcome” means for your firm, such as chronic lateness, severe aging, or write-off risk.

- Engineer a first feature set using only data you can maintain reliably.

- Test for noise and redundancy before adding more sources.

- Push scores back into workflow tools so the output drives action.

The best data foundation isn't the biggest one. It's the one finance can govern.

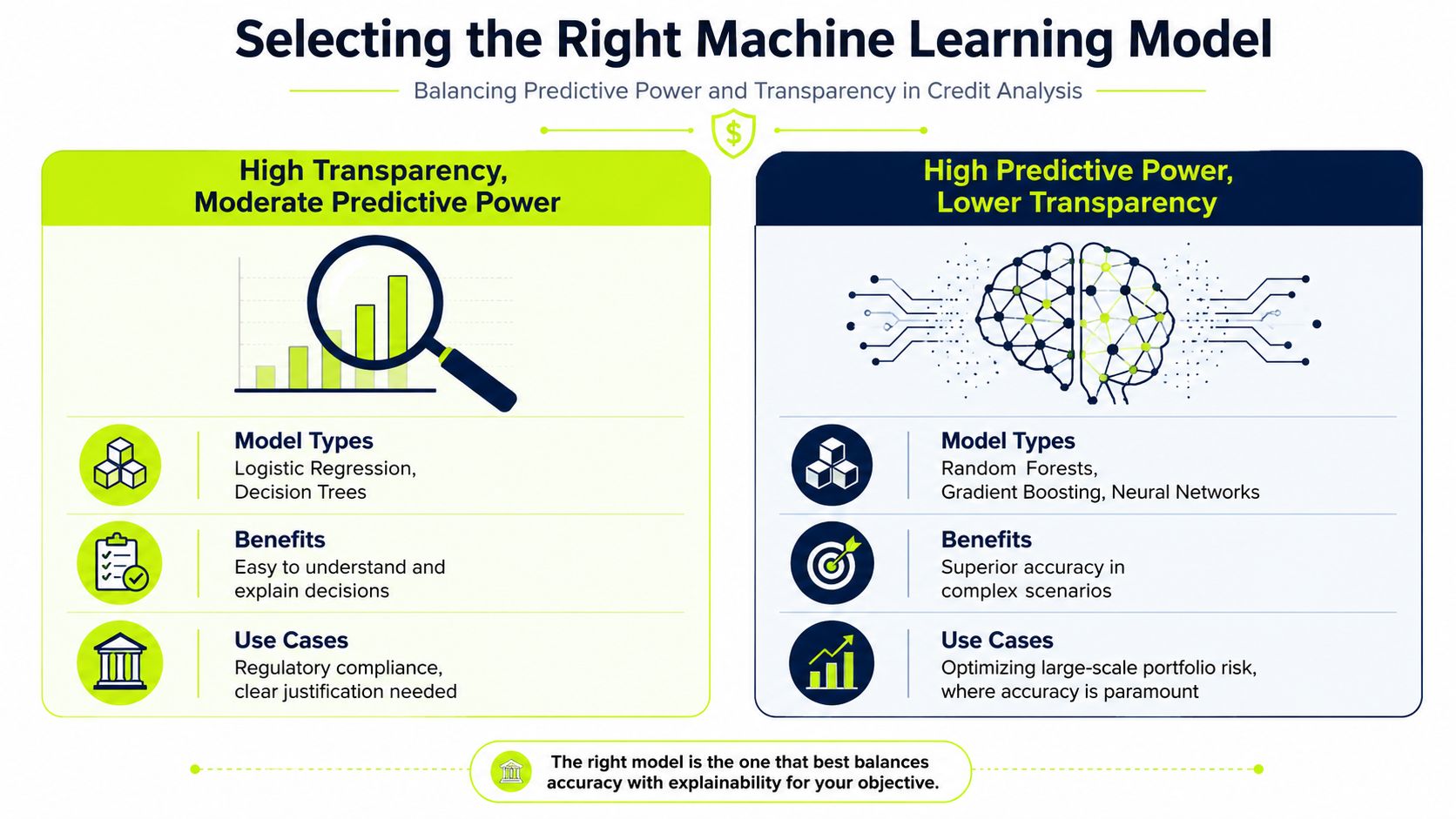

Selecting the Right Machine Learning Model

Most finance leaders don't need a lecture on algorithms. They need to know which model fits the control environment.

A key decision is a trade-off between predictive power and transparency. If your model is easy to explain but misses important risk patterns, collections stays reactive. If your model is powerful but opaque, audit, compliance, and client-facing justification become harder.

The practical comparison

Here is the finance view of the main options:

Model type | What it does well | Where it struggles | Best fit in AR |

|---|---|---|---|

Logistic regression | Clear, stable, easy to explain | Can miss interactions and non-linear effects | Firms that need simple reason codes and lighter governance |

Decision trees | Intuitive rule structure | Can be unstable if not controlled | Useful for prototypes and policy overlays |

Random forest | Stronger pattern detection | Harder to explain at decision level | Portfolio ranking and early warning |

XGBoost or gradient boosting | Often strongest predictive performance | More complex governance and interpretation | Mature finance teams with model oversight capability |

The mistake is assuming the most advanced model is automatically the right one. In practice, model quality depends on data quality, operating discipline, and the ability to defend decisions.

What the evidence says

A project using the American Express credit dataset reported 0.97 accuracy for XGBoost, compared with 0.9464 for logistic regression and 0.9650 for random forest. The same work reported 0.91 precision, 0.91 F1-score, and 0.92 AUC for XGBoost, and identified the most significant default predictors as credit score, credit limit utilization, and number of days employed, while age was not a significant factor (credit risk analysis using ML project results).

Those results don't mean XGBoost is always the right answer for a services firm. They do show why advanced models became attractive. They pick up interactions that simpler scorecards may miss.

What works in finance operations

For AR automation, I usually favor a staged approach rather than a leap straight into the most complex model.

Use a transparent baseline first. That baseline proves the data pipeline, validates definitions, and gives finance a benchmark. Then test a stronger model against it. If the stronger model materially improves ranking and early warning, keep it. But only if you can generate clear reasons for the output and embed those reasons into workflow.

A good operating question is not "Which model is smartest?" It's "Which model helps my team make better collection decisions every week, with defensible logic?"

A useful score is one your controller trusts enough to act on.

A sensible decision framework

Choose a simpler model when:

- Auditability is essential: You need straightforward explanations for why an account was flagged.

- Data is still maturing: Inconsistent inputs often negate the advantage of more advanced models.

- Change management matters most: Teams adopt tools faster when the logic feels familiar.

Choose a more advanced model when:

- Portfolio patterns are complex: Payment outcomes depend on combinations of variables, not one factor at a time.

- Ranking quality matters more than a neat formula: You need to know which invoices to touch first.

- You can support governance: Someone owns documentation, monitoring, and review.

In short, don't confuse sophistication with control. In receivables, the best model is the one that improves decisions and survives scrutiny.

Evaluating and Stress-Testing Your Risk Model

Month-end closes, DSO is drifting up, and the AR team says the queue "doesn't feel right." The model still posts a decent accuracy number, but collectors are spending time on accounts that would have paid anyway while a few large balances age past terms. That is the point of evaluation. Finance needs to know whether the score improves collection decisions under real operating conditions, not whether it looked good during model development.

For a professional services firm, that standard is practical. A useful model helps the team contact the right clients earlier, tighten terms on the right accounts, and protect cash flow without creating friction for healthy clients.

Metrics that matter to a CFO

Start with measures that connect directly to workload and cash outcomes:

- Precision: Of the clients or invoices flagged as high risk, how many turned late, disputed, or difficult to collect?

- Recall: Of the accounts that later caused a collection problem, how many did the model identify early enough to act?

- Ranking power: Do the highest-risk accounts consistently rise to the top, where the AR team can work them first?

- Calibration: Does a higher score correspond to higher observed risk, or are the numbers directionally useful but poorly scaled?

Those measures answer a finance question, not just a data science question. If precision is weak, the team wastes effort and credibility. If recall is weak, the model misses the very exposures it was supposed to surface. If ranking is weak, workflow priority breaks down.

Accuracy can still be reported. It just should not lead the discussion.

Test whether the model holds up under operating change

Historical fit is only the first screen. The harder question is whether the model remains reliable when billing patterns, client behavior, or approval processes shift.

In professional services, those shifts are common:

- A client sector slows and invoice approvals stretch out.

- The firm moves from retainers to milestone or usage-based billing.

- Procurement rules change at a major customer.

- Scope disputes increase because projects were sold loosely and documented unevenly.

These are finance and operations issues, and they change the meaning of the data. Evaluation should reflect that. I usually ask teams to review model performance by segment, by billing structure, and by recent invoice cohorts before approving broader rollout.

For a grounded overview of how machine learning models are evaluated for credit use cases, including the trade-off between predictive strength and explainability, FICO's guidance on building credit risk models with AI and machine learning is a useful reference.

A practical stress-testing routine

A small finance team can run a disciplined review without building a bank-style risk function.

- Slice results by segment. Check industry, client size, partner lead, contract type, and invoice type. A model that works for recurring advisory clients may perform poorly on project-based work.

- Separate recent cohorts. Payment behavior changes over time. Looking only at pooled historical data can hide current deterioration.

- Review false positives and false negatives with AR managers. They can often identify missing context such as approval bottlenecks, dispute patterns, or client personnel changes.

- Run scenario tests. Increase dispute frequency, lengthen approval cycles, or delay payments in a subset of accounts and see whether the ranking still supports sound collection priorities.

- Check actionability. If the model flags risk but cannot support a clear response, the score is not ready for production workflow. Teams that pair evaluation with defined collection plays usually get more value from AI for debt collection operations than teams that stop at scoring.

One warning sign appears early. The queue stops matching what experienced collectors see in the ledger.

When a model fails, the signs are often subtle at first. A few obvious accounts are ranked too low. A stable client gets escalated for no clear reason. Staff start overriding the score more often. Those are control issues, not minor annoyances.

That is why model evaluation belongs with finance, AR, and operations together. If the outputs do not line up with actual payment behavior, revise the features, retrain on fresher data, or tighten the use case. A model earns its place in AR when it improves prioritization, shortens collection cycles, and stands up to review from controllers, auditors, and leadership.

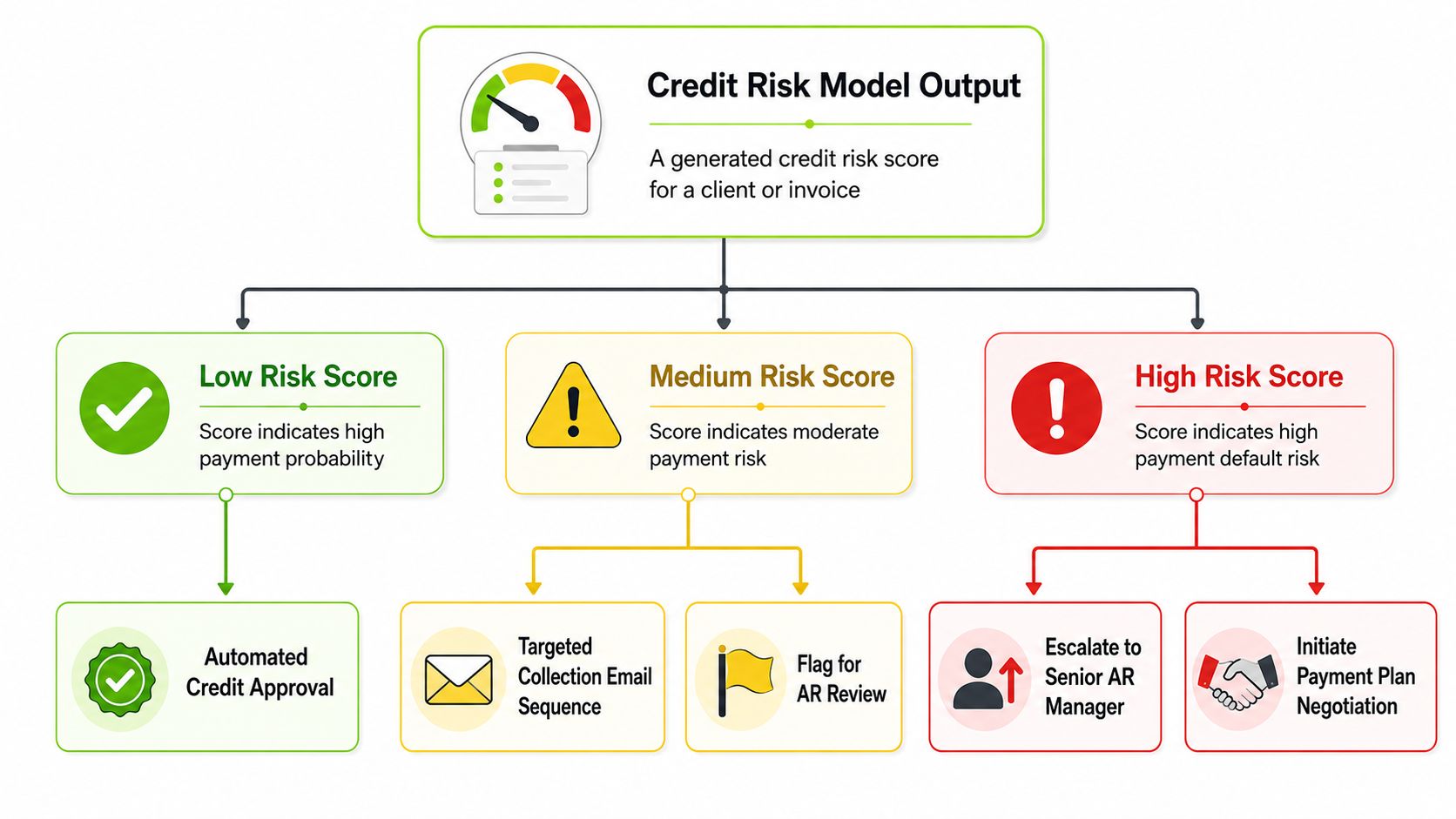

Integrating Risk Insights into AR Automation

A risk score sitting in a dashboard is an expensive ornament.

The payoff comes when the score changes what your AR team does, when they do it, and how much effort they spend. Credit risk analysis using machine learning then becomes part of accounts receivable automation rather than a side project.

Turn scores into operating rules

A practical AR workflow maps risk levels to actions.

Low-risk clients can stay on a standard reminder path. Medium-risk accounts may need earlier nudges, tighter follow-up, or invoice confirmation shortly after billing. High-risk accounts should trigger human review, direct outreach, and sometimes payment-plan discussion before the balance ages further.

That structure lets AI AR automation handle routine follow-up while your staff focuses on accounts where judgment matters.

What a working decision layer looks like

Here is a simple operating model for AR software for professional services:

Risk level | Typical signal | AR response |

|---|---|---|

Low | Stable payment history, low dispute activity | Standard reminder cadence |

Medium | Some slowing, approval friction, occasional disputes | Personalized outreach and queue review |

High | Repeated lateness, unresolved disputes, pattern deterioration | Immediate owner assignment and escalation path |

This matters most in firms where invoice volumes are rising but headcount isn't. Smart routing is how you reduce manual effort without losing control.

For teams thinking about collection workflow design, this article on AI for debt collection is relevant because it shows how automation and human review can complement each other.

Keep reason codes attached to every score

This is the part many implementations miss.

The IMF notes that machine learning can improve credit assessment, but it also highlights the governance challenge created by lower transparency in complex models. In practice, effective integration requires a system that can provide clear reason codes for risk scores so decisions can be justified to regulators, auditors, and affected parties (IMF paper on machine learning, transparency, and governance in credit risk).

That isn't only a bank problem. It's an internal control problem for any finance team using automated risk flags to shape collection actions or credit terms.

If a client gets shifted to a tighter collection path, your team should be able to explain why in operational language. For example:

- Recent payment slowdown

- Repeated invoice disputes

- Extended approval cycle

- Deterioration versus prior billing periods

Those explanations improve adoption because AR staff can judge whether the score aligns with what they know.

The workflow should stay human

The best implementations don't automate everything. They automate the predictable parts and route edge cases to people.

Use the model to decide cadence, channel, and priority. Let humans decide exceptions, relationship-sensitive outreach, and final escalation. That balance gives you a system that is faster than manual collections but still fit for professional services, where client relationships matter and a blunt approach can cost future work.

Governance, Monitoring, and Measuring Financial ROI

A credit model is not a one-time build. It is a finance process that needs ownership.

That means one person owns model performance, someone in finance owns policy, and someone in operations owns workflow execution. Without that structure, the model drifts into the same fate as many reporting projects. It exists, but nobody trusts it enough to use it decisively.

Governance is what keeps a good model useful

The World Bank makes an important point on alternative data and risk modeling: more data can improve prediction, but it can also introduce noise, privacy concerns, and bias if it isn't managed carefully. The report notes that alternative data has been associated with 5% to 20% predictive gains over traditional-data-only models, while also warning that governance and data quality matter materially (World Bank report on alternative data, predictive gains, and governance risks).

That is the right lens for professional services firms as well. More signals aren't automatically better. If you add weak or unstable inputs, the model may look smarter while becoming harder to trust.

The controls I would insist on

For a finance-led deployment, keep the governance framework practical:

- Version control: Record which model version is in production and when changes were made.

- Data ownership: Assign responsibility for invoice, payment, CRM, and dispute fields.

- Reason-code review: Check whether flagged accounts are explainable in finance terms.

- Drift monitoring: Watch for changes in payment behavior that make old patterns less useful.

- Exception logging: Track overrides by AR staff and review them for recurring themes.

One useful mindset is to treat model governance like any other finance system control. If it can influence cash collection behavior, it deserves documentation, review cadence, and escalation rules.

Strong models don't fail because the math breaks. They fail because the operating discipline around them weakens.

How to measure ROI without fuzzy math

CFOs don't need a grand narrative here. They need a clean before-and-after view.

Track ROI in three buckets:

- Cash performance

- DSO trend

- Aging movement by bucket

- Reduction in severe delinquency and write-off exposure

- Labor efficiency

- Time spent on manual prioritization

- Collector workload allocation

- Reduction in payment-chasing that doesn't change outcomes

- Decision quality

- Better prioritization of outreach

- Fewer preventable escalations

- More consistent application of credit and collection policy

You don't need to force numbers if your firm is early in the process. But you do need a baseline. If you can't compare post-launch results to a pre-launch operating state, you won't know whether the model improved cash flow or just added another dashboard.

For firms building a broader finance operating system, tools that enhance business financial strategy can help connect receivables signals with overall working-capital visibility. That matters because AR risk isn't isolated. It affects forecasting, hiring pace, partner draws, and borrowing decisions.

What works and what doesn't

What works:

- A narrow first use case

- Stable internal data before alternative data

- Human review for high-stakes cases

- Clear reason codes

- Monthly performance review with finance and AR together

What doesn't:

- Starting with the most complex model because it sounds advanced

- Feeding every available field into the model

- Treating collections automation as a substitute for credit policy

- Ignoring model drift after launch

- Declaring ROI before the process has stabilized

For professional services firms, this is ultimately about control. Better control over which clients are likely to pay on time. Better control over collector time. Better control over forecast reliability. And better control over cash.

Resolut automates AR for professional services, helping finance teams run collections with more consistency, less manual work, and better judgment. If you want a system that supports accounts receivable automation, AI AR automation, and human-in-the-loop control without turning client communication into a blunt instrument, Resolut is built for that balance.