Credit Risk Assessment Methods: Smart Decisions for 2026

Master credit risk assessment methods for professional services. Make data-driven AR decisions to improve cash flow and protect client relationships in 2026.

A client signs quickly, approves the proposal without friction, and pays the initial retainer on time. Everyone relaxes. Then the second invoice slips past terms. At first it looks like normal delay. Then it hits aging, the account team starts sending “just checking in” notes, and finance realizes the problem isn't one invoice. It's that nobody tested payment risk before the work ramped up.

That's the trap in professional services. You're not underwriting loans, but you are extending credit every time you deliver work before cash hits the bank. If your firm lives on monthly billing, milestone invoices, or ongoing retainers, credit risk sits inside your AR whether you label it that way or not.

Most firms handle this too late. They treat collections as a back-end cleanup task instead of a front-end control. That's backwards. Strong credit risk assessment methods don't exist to block good clients. They exist to set terms intelligently, protect margin, and keep client relationships from deteriorating under avoidable payment tension.

Introduction Why Client Onboarding Is Your First Line of Defense

Controllers usually know the pattern before they know the cause. A new client looks strong in the sales process. The partner trusts them. The scope expands fast. Then AR starts carrying the risk no one priced in.

In a services firm, that risk often becomes apparent in indirect ways. It appears as vague PO delays, invoice disputes that weren't raised during delivery, approvals that suddenly need “one more signoff,” or a billing contact who goes silent once the work is done. By the time the invoice is old, your negotiating strength is weak.

Client onboarding is where you keep that from happening.

You don't need a bank-style underwriting team. You need a disciplined intake process that answers a few practical questions before work starts.

- Who approves payment: Not just who signed the proposal, but who releases funds.

- How does the client buy services: Procurement-heavy enterprise, founder-led small business, PE-backed operator, nonprofit, agency, or government contractor. Each pays differently.

- What would slow payment: Missing vendor setup, budget timing, legal review, dependency on downstream client payment, or internal dispute risk.

- What terms fit the risk: Retainer, milestone billing, tighter review windows, or partial prepayment.

Good AR control starts before the first invoice exists.

If you skip this step, your team ends up using collections to solve an onboarding failure. That's expensive, distracting, and completely avoidable.

The Spectrum of Credit Risk Assessment

Credit risk assessment methods sit on a spectrum. On one end is operator judgment. On the other is statistical modeling. Most professional services firms need both, but they need to know which job belongs to which method.

From gut feel to measured risk

Credit risk assessment has evolved from manual judgment to statistical modeling. The first credit bureaus were established in the late 1800s, and modern empirical methods now rely on historical loan-performance data to calculate metrics such as Probability of Default (PD) over a defined time horizon, as outlined in this review of the history of customer risk assessment.

That matters even if you're not a lender. The underlying operating lesson is simple. Historical payment behavior beats opinion when you need consistent decisions.

Judgment still has a place. A partner may know that a client's CFO just changed, a merger is underway, or internal procurement is a mess. A model won't always catch that immediately. But judgment on its own breaks down fast when volume grows.

A useful way to frame this is through descriptive predictive prescriptive analytics. Finance teams first describe what happened, then predict what's likely to happen, then prescribe what action to take. That's exactly how a mature AR process should work.

What the spectrum looks like in practice

Here's the most straightforward approach:

Approach | What it uses | Best use in a services firm | Main weakness |

|---|---|---|---|

Pure judgment | Partner instinct, sales notes, client reputation | New or strategic accounts with limited data | Inconsistent and hard to audit |

Hybrid assessment | Intake questions plus payment history and aging signals | Most mid-market client decisions | Requires discipline to maintain |

Empirical scoring | Historical outcomes, disputes, payment timing, portfolio patterns | High-volume recurring billing environments | Needs structured data |

The mistake is treating this like a philosophy debate. It isn't. It's an operating choice.

Use human judgment where data is thin. Use empirical methods where invoice volume is high and repeatable patterns exist. If you do the opposite, you either slow the business down or accept more risk than you realize.

The right question isn't “Should we trust people or data?” It's “Which decisions need consistency more than intuition?”

Applying the 5 Cs Framework to Service Clients

The 5 Cs still work. You just have to translate them out of commercial lending language and into service delivery reality.

Character and capacity

Character is the client's payment behavior and reliability. For a services firm, that means asking whether they approve invoices cleanly, whether they create surprise disputes, and whether their internal team treats vendors professionally. A prospect can have a polished brand and still be a poor payer.

Capacity is their ability to pay from operating cash flow. Don't confuse top-line revenue with payment strength. A growing company with weak internal controls can be a harder account than a slower, well-run firm with disciplined AP.

Use intake questions that force specifics:

- Character check: Ask who has approved prior vendors, how invoice disputes are handled, and whether billing goes through procurement or department heads.

- Capacity check: Ask how your invoice fits their budget cycle, whether spend is pre-approved, and whether milestone billing aligns with cash release authority.

Capital, collateral, and conditions

Capital is financial stability. In services, you're not always getting audited financials, but you can still look for practical signs. Have they recently raised funding, changed ownership, cut headcount, or centralized approvals? Those are operating signals, not trivia.

Collateral is the hardest one for service firms because you usually don't hold physical assets. Treat it as commitment and advantage. A large upfront retainer, access to core deliverables only after payment, or contractual control over final work product all function like practical substitutes for collateral.

Conditions are external pressures on the client. Their sector may be under stress. Their customers may be paying slowly. A project tied to discretionary marketing spend carries different risk than one tied to compliance, legal, or mission-critical operations.

Here's a simple field guide:

- Low concern: Clear approver, defined budget, clean billing process, mission-critical work

- Medium concern: Some approval complexity, longer AP cycle, minor dispute history

- High concern: Unclear payer, changing scope, budget ambiguity, repeated documentation friction

For firms that want to compare software options around this workflow, this guide to credit risk assessment tools is a useful starting point.

If your team can't explain why a client received certain terms, you don't have a policy. You have improvisation.

The Limits of Manual Assessment

Manual assessment feels prudent because it's familiar. It also hides a lot of sloppiness.

The 5 Cs are useful, but they're subjective by design. One partner calls a client “strategic” and pushes for open terms. Another sees the same account as a collections headache and asks for tighter controls. Both think they're being reasonable. Finance gets stuck cleaning up the difference.

Subjectivity becomes policy drift

That inconsistency is more expensive than most firms admit. It changes terms account by account, creates exceptions no one documents, and teaches clients that payment discipline is negotiable if they escalate to the right internal sponsor.

Judgmental methods evaluate the 5 Cs qualitatively, but they're subjective. Empirical models learn from historical outcomes, which reduces analyst bias. Bank-grade systems use 60% training / 20% validation / 20% testing and track performance with metrics like AUC to measure discrimination power, as explained in this overview of credit risk modeling and assessment.

You probably won't build a bank-grade model inside a services firm. That's fine. The lesson still applies. If a method can't be tested against outcomes, you can't tell whether it's improving decisions or just making people feel comfortable.

Manual processes don't scale

The second problem is scale. A partner can personally screen a small client base. They can't reliably do that across a broader portfolio with different industries, billing patterns, and payment behaviors.

Manual review also slows down the process in exactly the wrong places:

- At onboarding: Finance waits for context trapped in sales emails or partner memory.

- At billing: Exceptions pile up because no one linked risk level to terms in advance.

- At collections: AR uses the same reminder cadence for good clients and bad ones.

That last point matters most. If every account gets the same treatment, you're not managing risk. You're sending reminders.

You can't improve what you can't measure

A manual system doesn't create a feedback loop. It rarely tracks whether a client with “standard terms” consistently pays late, whether disputes predict eventual delinquency, or whether certain service lines carry higher payment risk.

A practical finance team needs more than opinions. It needs pattern recognition.

That doesn't mean replacing operator judgment. It means containing it. Keep judgment for exceptions. Move recurring decisions into a framework that finance can review, compare, and refine.

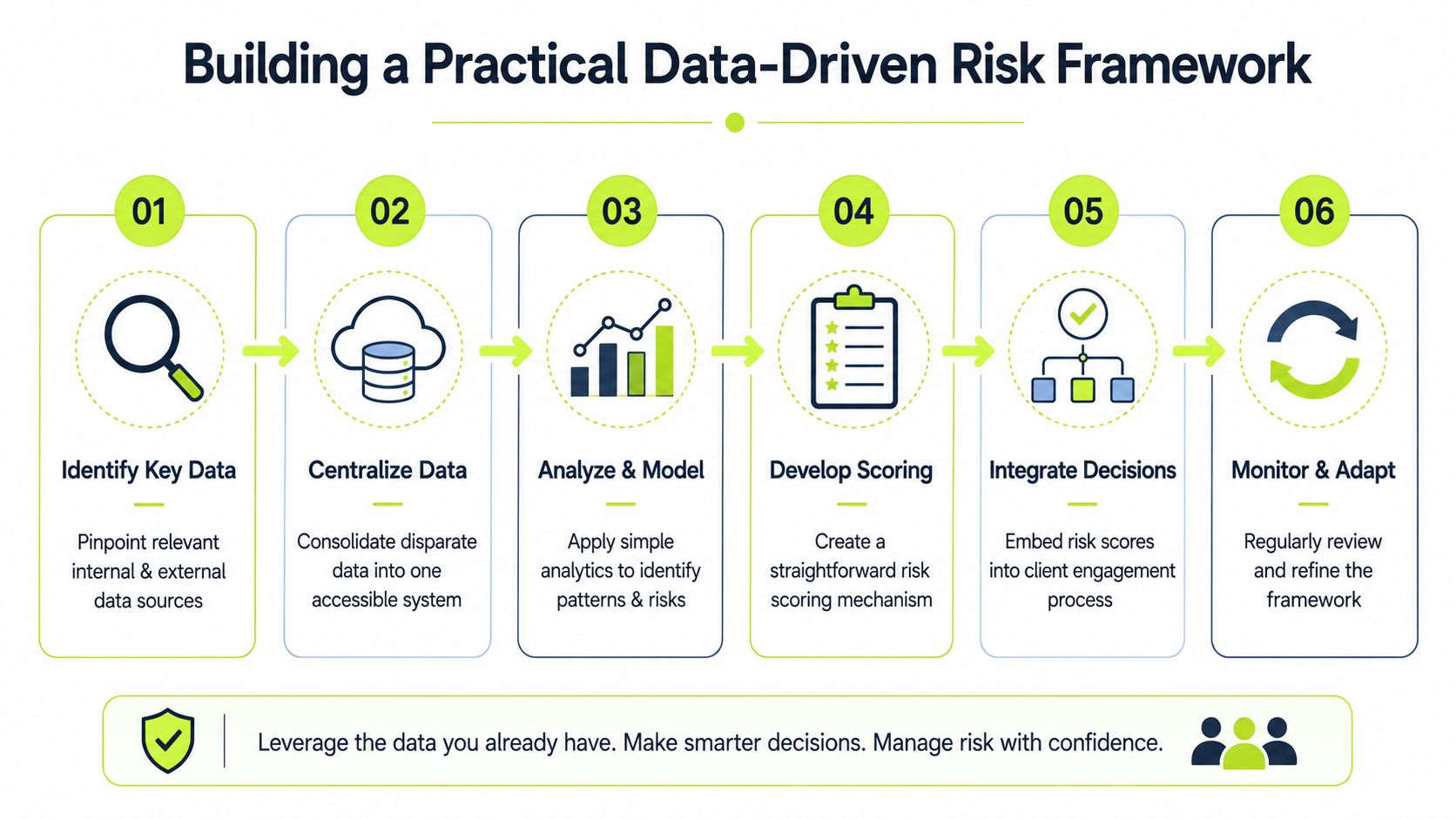

Building a Practical Data-Driven Risk Framework

A services firm doesn't need a quant team to build a useful risk model. It needs clean habits and a short list of variables that matter.

Start with the data you already own

Most firms already have the raw inputs sitting in QuickBooks, their PSA, CRM notes, email threads, and billing history. They just haven't turned that information into a consistent score.

Focus on a small set of signals:

- Payment behavior: Days to pay, broken promises, partial payments, and whether delays are isolated or recurring

- Invoice quality signals: Frequency of disputes, credits, rebills, or approval delays

- Engagement structure: Retainer versus project work, milestone billing, concentration by client

- Client context: Industry, size, ownership structure, billing contact stability

If you enrich that with external data, keep it practical. A World Bank review found that combining traditional bureau data with alternative sources such as utility, phone, cable, earnings-history, and transaction data can improve predictive power by 5% to 20%, and leading frameworks combine PD, EAD, and LGD to calculate expected loss, according to the World Bank paper on alternative data and credit reporting.

For a services firm, the takeaway isn't to mimic bank math. It's to widen your lens beyond a single credit score or a partner's opinion.

Turn signals into risk tiers

Keep the scoring logic simple enough that your controller can explain it in one minute.

A workable version looks like this:

Risk tier | Typical signals | Recommended terms |

|---|---|---|

Low | Consistent payment behavior, clean approvals, low dispute friction | Standard terms, automated reminders |

Medium | Some aging, occasional disputes, slower internal approvals | Shorter review windows, earlier reminder cadence, tighter milestone billing |

High | Recurring aging, unclear payer, repeated disputes, unstable process | Upfront retainer, staged billing, senior review before additional work |

This framework should drive action, not sit in a dashboard.

A related operational benefit of enrichment is that the same discipline that helps improve sales outreach also helps finance identify who controls budget, approvals, and payment workflows.

Review and recalibrate

Scores get stale if no one checks outcomes. Finance should review whether clients placed in a low-risk tier behave like low-risk accounts and whether medium-risk accounts are drifting upward.

If you're exploring more advanced scoring approaches, this overview of credit risk analysis using machine learning is worth reading.

Operator view: Don't overbuild the model. A simple score used consistently is better than a sophisticated one no one trusts.

How AR Automation Operationalizes Risk Assessment

A risk framework only matters if it changes behavior inside AR. Otherwise it's just a smarter spreadsheet.

In practice, accounts receivable automation and AI AR automation become useful. Not because they sound modern, but because they convert policy into repeatable execution. A finance team can define terms, reminder timing, escalation thresholds, and exception handling once, then apply them consistently across the portfolio.

Risk-aware AR beats generic collections

Most professional services firms still run collections in a blunt way. Same follow-up cadence. Same tone. Same delay before someone intervenes. That creates two problems. Good clients get unnecessary friction, and risky clients get too much time.

A better operating model links risk tier to action:

- Low-risk accounts: Standard invoicing, courteous reminders, self-serve payment options

- Watchlist accounts: Earlier follow-up, tighter internal review, faster escalation of disputes

- High-risk accounts: Shorter terms, live owner involvement, restricted work expansion until balance behavior improves

That's how you reduce DSO without turning your finance team into an aggressive collections shop. It also protects the relationship because the outreach matches the account's actual behavior.

Modern supervisory frameworks are useful here conceptually. The ECB's SREP methodology treats credit risk assessment as both a quantitative risk-level estimate and a qualitative control assessment, separating inherent risk from the management and control framework. For AR teams, the lesson is to combine early-warning indicators with a documented process so outputs remain explainable and auditable, as described in the ECB's explanation of credit risk SREP methodology.

That's exactly what a mature AR process needs. Not just a score. A score plus rules plus a documented override path.

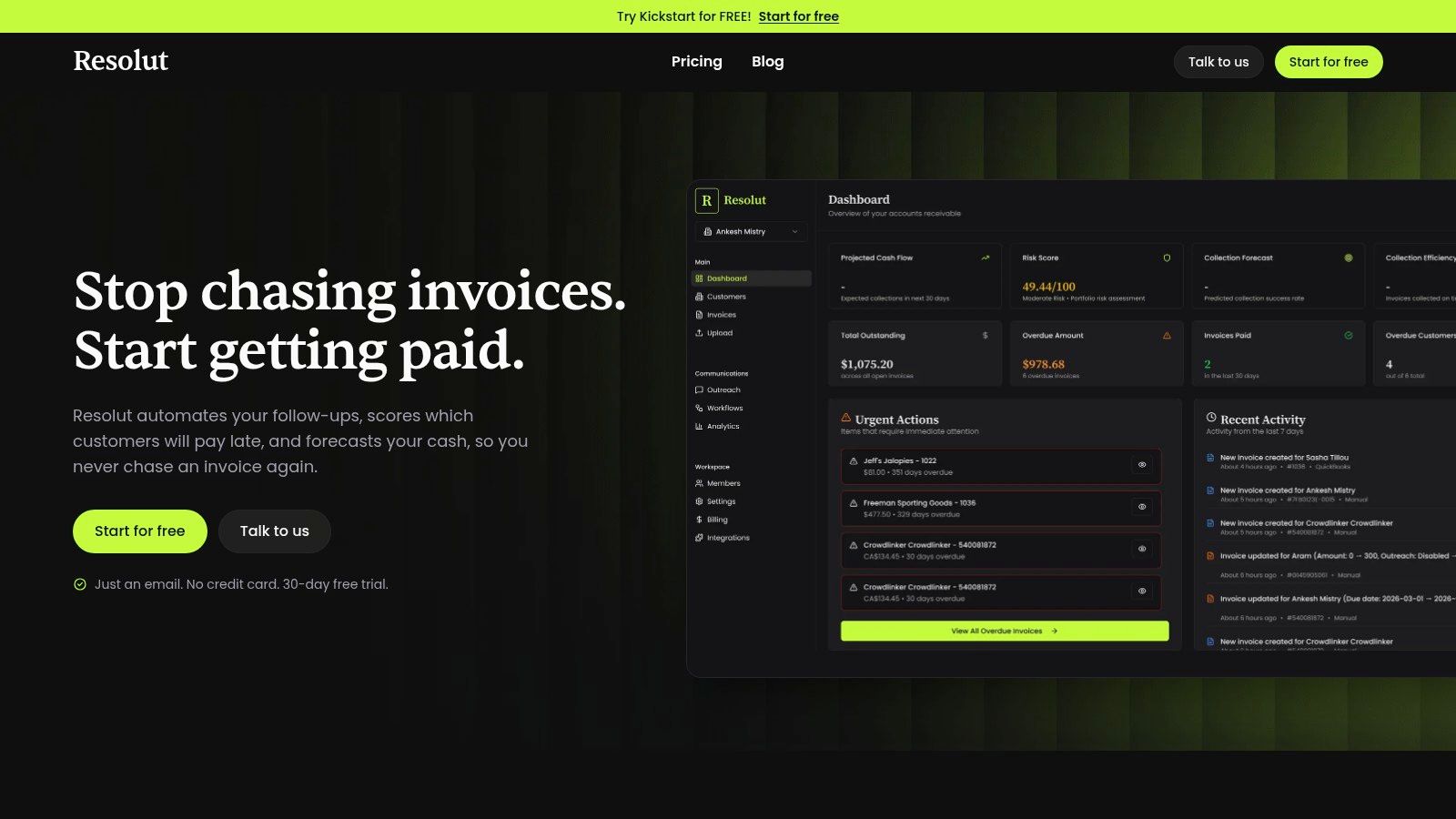

What this looks like inside a real finance stack

In a services firm, the most practical setup is usually tied directly into your accounting system. If you're running QuickBooks AR automation, for example, the system should pull invoice status, payment timing, and aging data automatically instead of asking staff to update trackers by hand.

The operating loop is straightforward:

- Pull live billing and payment data from the accounting system.

- Classify accounts based on payment behavior and current exposure.

- Trigger the right workflow for reminders, escalations, and internal alerts.

- Capture response patterns so finance can see what's improving and what isn't.

That's what good AR software for professional services should do. It should reduce manual work, tighten consistency, and give the controller a cleaner view of where cash risk sits today.

For a closer look at the mechanics, this explainer on what AR automation is covers the operating model well.

A short product walkthrough makes the workflow easier to visualize:

Automation doesn't replace judgment

Some firms get nervous concerning this. They assume automation means losing nuance. It doesn't. It means reserving human attention for the accounts that deserve it.

Document the rule. Automate the routine. Escalate the exception.

That's the right balance. Finance still decides policy. Relationship owners still handle sensitive calls. But the system handles consistency, timing, and visibility. That's how you improve cash flow without running AR through heroics every month.

Conclusion From Reactive Collections to Proactive Control

Most professional services firms don't have a collections problem. They have a control problem.

They let client risk enter the business unnoticed, usually at onboarding, then ask AR to fix it after invoices age. That approach burns team time, weakens client communication, and makes cash flow less predictable than it should be.

Better credit risk assessment methods solve that upstream. Start with a disciplined intake process. Use the 5 Cs in plain business language. Stop relying entirely on partner instinct once account volume grows. Build a practical score from real payment behavior, billing friction, and client context. Then make sure AR executes against those rules consistently.

This is the shift that matters. Finance moves from reacting to late invoices to controlling exposure before it becomes a collections issue. Good clients get a smoother experience. Riskier clients get tighter terms and faster intervention. Leadership gets cleaner visibility into where cash may slip.

That's not academic risk management. It's operational discipline.

If you want to reduce DSO, improve cash flow, and make accounts receivable automation work in a services environment, keep the model simple and the process strict. Complexity won't save you. Consistency will.

Resolut helps professional services firms turn AR into a controlled operating system instead of a monthly scramble. With Resolut, teams can automate follow-up, apply risk-aware workflows, and keep collections consistent, accurate, and human.