10 Credit Risk Management Best Practices

Actionable credit risk management best practices for CFOs. Reduce DSO and improve cash flow with proven strategies for automation and control.

For every ten invoices a professional services firm sends, one will likely go unpaid or require costly intervention. That gap sits directly in cash flow, partner draws, hiring plans, and how much time your finance team wastes chasing avoidable exceptions.

In firms built on trust and relationships, credit risk often gets handled informally. A partner says the client is good for it. Billing goes out late because the team is busy. Collections wait because no one wants to strain the relationship. Then aging builds, disputes linger, and finance gets pulled into cleanup mode.

That's not a relationship strategy. It's a control failure.

The stronger approach is simple. Treat credit risk as an operating system, not a one-time approval step. The Basel Committee's disclosure framework helped standardize a structure that still holds up today: policy, measurement, monitoring, and disclosure across credit exposures and quality, with enough information about models and methods to make risk understandable and comparable (Basel Committee guidance on credit risk disclosure).

For a professional services firm, that means moving beyond spreadsheets, partner memory, and reactive calls. It means building an accounts receivable automation process that scores risk early, updates exposure continuously, routes work automatically, and makes payment easy when the client is ready.

The payoff isn't theoretical. You get tighter control, cleaner prioritization, fewer preventable delays, and better odds of reducing DSO without turning your finance team into a call center.

Here are ten credit risk management best practices that are effective in the field.

1. Predictive Credit Scoring and Risk Assessment

Most firms still make credit decisions once, at onboarding, then act surprised when a previously good client turns into a collection problem. Static reviews miss how risk manifests in services businesses. It often starts with slower approvals, partial payments, project overruns, or a change in billing contacts.

A better scoring approach combines external credit data with your own payment history, dispute patterns, invoice aging behavior, and engagement signals. The score has to be explainable. If finance can't tell a partner why an account moved from standard terms to tighter controls, the model won't survive contact with the business.

S&P Global's private-credit guidance points in the right direction here. Best practice is defensible scoring that combines qualitative and quantitative drivers, supported by annual recalibration and good recordkeeping, because poor records create operational risk (S&P Global guidance on best-practice risk management for private credit).

What works in practice

In a professional services firm, scoring should drive actions, not just dashboards. A high-risk client might require milestone billing, shorter terms, or partner approval before new work starts. A stable client with clean payment behavior can stay on normal terms with lighter-touch reminders.

Use your own operating data aggressively:

- Payment behavior: Track whether the client pays on stated terms, only after reminders, or only after escalation.

- Invoice friction: Flag accounts with repeated disputes, missing POs, or frequent billing corrections.

- Exposure trend: Watch whether open AR is growing faster than the client's normal payment pattern.

- Relationship context: Fold in account team insight, but document it so judgment doesn't replace process.

Practical rule: If the score doesn't change the next action, it isn't a risk model. It's decoration.

If you need a practical grounding in what should feed a score, this overview of credit worthiness is a useful starting point.

2. Dynamic Credit Limit Management

Credit limits shouldn't be set once and forgotten. In services firms, exposure changes fast. A client that starts with a small monthly engagement can move into a large project, multiple statements of work, or a stack of pass-through expenses before anyone notices the receivable has outgrown the original assumptions.

That's where firms get hurt. Not because the client was obviously bad, but because exposure drifted while controls stood still.

Set limits that move with behavior

Dynamic limits tie open exposure to current risk, not just onboarding paperwork. If a client pays consistently and documentation is clean, you can expand room for work. If payment slows or disputes increase, the limit should tighten automatically or trigger review.

The trade-off is obvious. Sales teams hate surprises, and partners don't want a project paused because finance changed a limit behind the scenes. So don't run this as a black box. Publish the rules.

A workable model often includes:

- Clear increase logic: Reward clean payment history and predictable billing administration.

- Clear decrease logic: Tighten when aging worsens, disputes stack up, or promised payments slip.

- Grace windows: Give account teams a short period to resolve issues before a hard stop.

- Approval paths: Let exceptions happen, but require named ownership.

The point isn't to block revenue. It's to stop financing a client's working capital without meaning to.

In firms using AR software for professional services, this becomes much easier because limits can be tied to live invoice status, not a monthly spreadsheet review. That's a major shift from static credit control to real operating control.

3. Omnichannel Collections Strategy

Collections break down when every reminder looks the same and every client gets chased through the same channel. Some clients respond to email immediately. Others ignore inbox reminders but pay the moment they get a text with a portal link. Others need a call from the account lead because the issue is procedural, not financial.

A coordinated omnichannel approach fixes that. The message, channel, and timing should change based on account history and customer behavior.

The broader process matters because credit risk doesn't end at approval. It runs through assessment, decisioning, monitoring, and collections follow-up, and modern guidance emphasizes continuous monitoring with early-warning and intervention playbooks instead of periodic review (HighRadius discussion of credit risk process and collections follow-up).

Sequence the channels, don't spam them

What works is orchestration. Start with a clear email reminder before due date. Follow with a portal-linked reminder near due date. Escalate to SMS or phone only if the client hasn't engaged. If they open the invoice and schedule payment, pause the sequence. If they raise a dispute, route the account out of collections and into resolution.

That discipline matters more than channel count.

A useful reference point is this guide to collection processes along with these B2B collections best practices.

Good collections feels coordinated from the client side. Bad collections feels like four people from your firm don't talk to each other.

If you're pursuing AI AR automation, this is one of the first places to apply it. Let the system pick the next best touch based on engagement, risk tier, and invoice status. Keep humans on exceptions and relationship-sensitive escalations.

4. Automated Cash Application and Reconciliation

You can't manage credit well if cash posting lags reality. When payments sit unapplied, your aging is wrong, risk flags are wrong, and collectors waste time contacting clients who may have already paid.

This is one of the least glamorous parts of accounts receivable automation, but it has outsized operational value. If your team still spends hours matching remittances, bank deposits, short pays, and invoice references by hand, your risk data is delayed at the exact point where speed matters.

Clean posting is a control function

Automated cash application should pull bank data, remittance detail, and invoice records into one workflow, then match and post with exception handling for the ambiguous items. Systems like SAP Cash Application, BlackLine, and other reconciliation platforms have made this standard in larger environments. Smaller firms can apply the same principle with lighter tooling, especially when QuickBooks AR automation is part of the stack.

A practical rollout looks like this:

- Start with simple payment types: ACH and clean remittance patterns are the easiest place to automate.

- Design exception queues: Short pays, bundled payments, and missing references need owners and aging rules.

- Keep manual override: Some payments will always need judgment.

- Feed corrections back: Repeated mismatch patterns usually point to invoice design or customer instruction problems.

For firms fighting to improve cash flow, this matters because unapplied cash hides the true state of receivables. Finance can't prioritize accurately if the ledger is a day or two behind.

For a useful outside perspective on workflow pain, this piece on solving manual AR data entry captures the operational drag well.

5. Segmentation-Based Collection Strategies

Not every late invoice deserves the same treatment. A longtime client with one missed payment and a clean history is different from a chronically slow payer with constant billing objections. Treating them the same creates unnecessary friction in one case and not enough pressure in the other.

Segmentation is one of the most practical credit risk management best practices because it lets a small AR team behave like a much larger, more disciplined function.

Build a few segments first

You don't need a complex model on day one. Start with a manageable set of segments based on payment behavior, invoice value, and relationship importance. Then map a collection path to each segment.

For example:

- Low-risk, high-value clients: Light reminders, named owner follow-up, easy access to payment options.

- Medium-risk accounts: Earlier reminders, tighter cadence, more explicit due-date language.

- High-risk accounts: Faster escalation, shortened terms on new work, possible retainer or milestone billing.

- Dispute-prone accounts: Separate workflow focused on issue resolution before standard collections resumes.

The FICO Mortgage Credit Risk Manager's Best Practices Handbook describes segmentation by delinquency status, credit score, and product type as a critical best practice, and notes that leading servicers increasingly integrate transactional data from origination, servicing, and collections with predictive analytics (FICO handbook on portfolio segmentation and predictive analytics).

The asset class is different, but the operating lesson carries over. Segment first. Then monitor continuously. Static quarterly review is too slow when payment behavior changes mid-engagement.

6. Legal Escalation and Litigation Strategy

Most firms either escalate too late or threaten legal action too early. Both are expensive mistakes.

Late escalation wastes collectability. Early escalation damages a recoverable relationship and can turn an administrative issue into a defensive standoff. The right answer is a written escalation policy with clear triggers, documentation standards, and decision rights.

Use legal pressure selectively

Legal action works best when the account is large enough to justify cost, the documentation is strong, and normal commercial resolution has failed. It also works better when your internal file is clean: signed engagement terms, approval trail, invoice history, delivery evidence, and a record of collection attempts.

A sensible sequence usually looks like this:

- Commercial escalation first: Senior finance or partner outreach, not just collector follow-up.

- Formal demand next: Written notice with clear amount due, basis, and deadline.

- Counsel review before filing: Assess collectability, venue, contract terms, and relationship implications.

- Alternative resolution if viable: Mediation or negotiated payment plan can beat litigation in many service disputes.

Operator's view: Litigation is a recovery tool, not a collections strategy.

If you use legal-style messaging inside your collections workflow, control the language carefully and involve counsel where needed. The purpose is to create seriousness and clarity, not to bluff. Professional services firms especially need discipline here because many receivable disputes are mixed. Part billing disagreement, part client cash issue, part relationship fatigue.

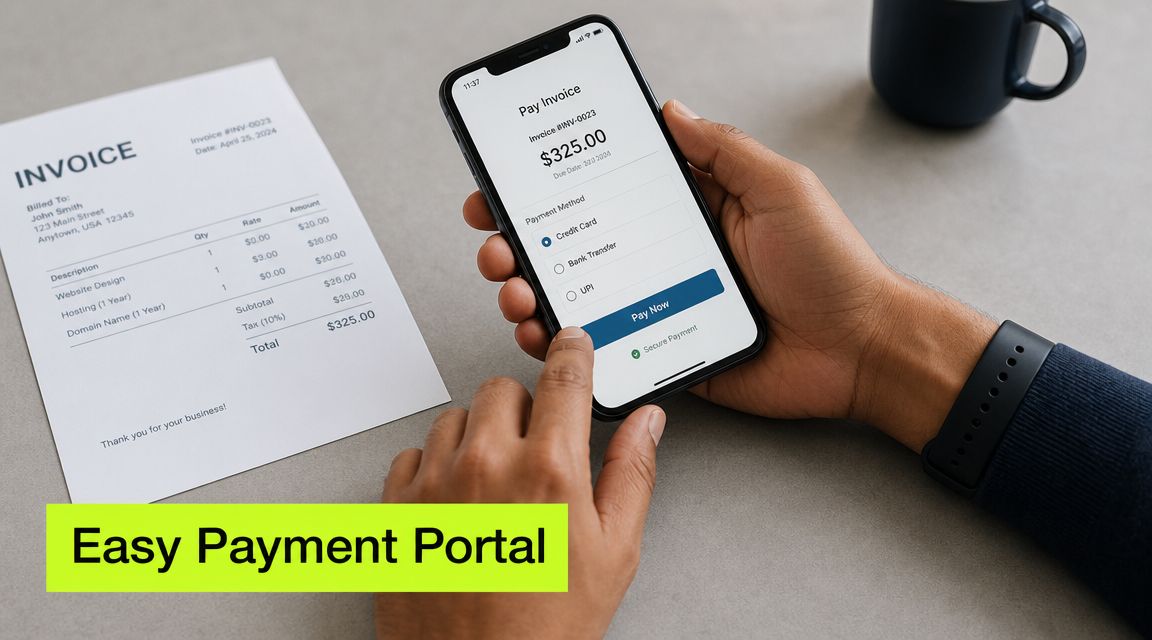

7. Customer Payment Portal and Flexible Payment Options

A surprising amount of payment delay has nothing to do with credit quality. The client intends to pay, but the process is annoying. The invoice PDF is buried. The ACH instructions are missing. The approver is on mobile. The payment page is clunky. AP needs a card option for one entity and bank transfer for another.

If you want to reduce DSO, remove payment friction first.

Make paying easier than delaying

A good portal should let clients view invoices, choose a payment method, schedule payment, and confirm status without emailing your team. For many firms, that means supporting ACH, cards, and other digital options in one clean experience.

This is especially useful for firms with recurring invoices, milestone billing, or multiple legal entities. Clients don't want to decipher remittance instructions every time. They want a consistent path.

What tends to work:

- Portal links in every reminder: Don't make the client search for the way to pay.

- Mobile-friendly design: Many approvals happen away from a desktop.

- Saved preferences where appropriate: Returning clients shouldn't start from scratch.

- Structured payment plans: Helpful when a large invoice needs staged resolution.

Continuous monitoring guidance from modern credit providers also emphasizes proactive delinquency management and making the payment process simple, secure, and efficient, alongside ongoing visibility and early-warning triggers (LoanPro guide for modern credit providers).

Later in the client journey, education helps too. This short video is useful if your team is thinking about how digital payment experiences affect collection outcomes.

For firms evaluating AR software for professional services, this is one area where product quality is immediately visible to the client.

8. Risk-Based Resource Allocation and Portfolio Management

Most AR teams don't have a workload problem. They have a prioritization problem.

Collectors and controllers spend too much time on low-impact follow-up because the queue is ordered by age or whoever complained most recently. Meanwhile, the accounts that require judgment sit untouched because no one has a clean way to rank effort against likely cash impact.

Put your best attention where it matters

Risk-based allocation means routing accounts by expected value, likelihood of recovery, relationship sensitivity, and operational complexity. A high-balance account with recent slippage and no dispute owner should rise quickly. A low-balance invoice with an engaged client and scheduled payment shouldn't absorb senior attention.

In practice, this means portfolio views that combine:

- Exposure size

- Aging and movement

- Risk score

- Dispute status

- Strategic account importance

- Collector workload and skill fit

There's a governance angle here too. The Basel disclosure framework emphasized that model-based credit approaches should include enough qualitative and quantitative information to make risk management understandable and comparable. That principle applies internally even if you're not a bank. If your routing logic can't be explained, it won't be trusted.

The firms that improve cash flow consistently don't ask their teams to work harder. They route the right accounts to the right action sooner.

9. Customer Communication and Dispute Resolution Framework

Disputes are where many firms lose control. A client says the invoice is wrong, or the work wasn't approved, or the PO changed, and collections stops. Then the issue sits between billing, delivery, and account management until the receivable becomes old enough to trigger panic.

That isn't a dispute process. It's a parking lot.

Separate disputes from delays

You need a formal taxonomy. Pricing issue, scope issue, missing documentation, billing error, service complaint, approval-chain problem. Each category should have an owner, response standard, and escalation path.

Without that structure, two bad things happen. Legitimate disputes take too long to resolve, and weak excuses get treated like valid blockers.

A tighter framework usually includes:

- Acknowledgment rules: Confirm receipt quickly so the client knows the issue is moving.

- Named ownership: Billing, project lead, legal, or account manager. Not "the team."

- Documentation requirement: The client must identify the invoice issue specifically.

- Partial payment option where appropriate: Uncontested amounts shouldn't wait on the whole dispute.

- Closure confirmation: Resolve, document, and return the account to normal collections.

Disputes should slow collection only for the portion that's genuinely in question.

For professional services firms, this is often where AI AR automation is most helpful. Not to decide who's right, but to classify disputes, route them instantly, track aging, and prevent silent stagnation. The main control win is speed and ownership.

10. Data-Driven Performance Analytics and Continuous Improvement

If the only AR number leadership sees is total overdue balance at month-end, you're managing by autopsy. Good credit control needs live operating signals. Which segments are slipping, which collectors are overloaded, which clients always promise then miss, which dispute types keep recurring, and where payment friction is slowing otherwise healthy accounts.

The point of analytics isn't reporting volume. It's changing decisions faster.

Track leading indicators, not just lagging outcomes

Strong dashboards for credit and collections usually combine portfolio health, workflow efficiency, and client behavior. DSO matters. So do promise-to-pay kept rates, dispute aging, unapplied cash volume, pre-due reminder engagement, and payment method mix.

The most useful review cadence is layered:

- Weekly team review: Exceptions, aging movement, bottlenecks.

- Monthly management review: Segment trends, exposure changes, policy adjustments.

- Quarterly reset: Scoring logic, thresholds, staffing, and automation rules.

For firms building a more analytical discipline, this explanation of the collection effectiveness index is a practical companion metric to DSO. And if you want examples of event-driven reporting patterns, these powerful real-time analytics examples are helpful.

One more operating point matters here. As noted earlier, modern credit risk programs have moved from periodic review to continuous surveillance, segmentation, and early-warning logic. Your analytics stack should reflect that. Static month-end packs won't support dynamic credit decisions.

Top 10 Credit Risk Management Practices Comparison

Item | Implementation Complexity 🔄 | Resource Requirements 💡 | Expected Outcomes 📊⭐ | Ideal Use Cases | Key Advantages ⚡ |

|---|---|---|---|---|---|

Predictive Credit Scoring and Risk Assessment | High, ML models, retraining, data pipelines 🔄 | Large historical datasets, data scientists, external data integrations 💡 | Early risk detection; reduce defaults ~15–25%, identify risk 30–60 days earlier 📊⭐ | Large B2B portfolios with rich payment history (SaaS, manufacturing) | Proactive interventions and dynamic risk profiles for targeted action ⚡ |

Dynamic Credit Limit Management | High, real‑time rules engines and governance 🔄 | Real‑time monitoring, integration with AR/sales, strong policy controls 💡 | Lower bad debt by ~10–20%; enable revenue growth via safe limit increases 📊⭐ | Companies balancing growth and exposure (distributors, fintech lenders) | Automated exposure control that balances risk and sales opportunity ⚡ |

Omnichannel Collections Strategy | Medium‑High, multi‑platform orchestration 🔄 | Unified comms platform, channel integrations, content ops, compliance monitoring 💡 | Payment response ↑30–50%; lower cost per contact and improved CX 📊⭐ | High‑volume AR with varied customer preferences; global collections | Higher engagement through preferred channels and personalized sequencing ⚡ |

Automated Cash Application and Reconciliation | Medium, ERP/bank integrations and ML matching 🔄 | Clean payment data, bank feeds, ML models, IT/finance support 💡 | Eliminates 80–90% manual work; reduces DSO by ~2–3 days; near‑real‑time posting 📊⭐ | Organizations with high payment volumes and varied payment types | Rapid reconciliation, improved cash visibility, frees AR capacity ⚡ |

Segmentation‑Based Collection Strategies | Medium, segmentation logic + workflow automation 🔄 | Segmentation models, automation rules, performance tracking tools 💡 | Collection rates ↑15–25%; collection costs ↓20–30% via targeted effort 📊⭐ | Firms with diverse customer/value mix needing tailored approaches | More efficient resource use and improved customer satisfaction ⚡ |

Legal Escalation and Litigation Strategy | Medium, legal integration and compliance controls 🔄 | Legal counsel, documentation processes, decision logic, budget for litigation 💡 | Recoveries ↑30–50% on high‑value delinquent accounts; deterrence effect 📊⭐ | Chronic non‑payers or high‑value accounts where recovery justifies cost | Strong leverage for recovery and formal resolution; clear escalation path ⚡ |

Customer Payment Portal & Flexible Payment Options | Medium, payment integrations and security 🔄 | Payment processors, PCI/security, UX, multi‑currency support, support team 💡 | Collection rates ↑15–25%; faster posting and better payment convenience 📊⭐ | Businesses seeking self‑service payments and global invoicing | Lowers payment friction, offers flexible plans and faster cash application ⚡ |

Risk‑Based Resource Allocation & Portfolio Management | High, portfolio analytics and workforce mgmt 🔄 | Portfolio analytics engine, forecasting, capacity planning, collector tools 💡 | Collection rates ↑20–30%; collection costs ↓25–40%; improved scalability 📊⭐ | Large portfolios requiring prioritization and ROI‑focused resourcing | Maximizes collector ROI and scales operations without proportional headcount ⚡ |

Customer Communication & Dispute Resolution Framework | Medium, cross‑department workflows and SLAs 🔄 | Dispute intake system, clear SLAs, coordination with ops/sales/legal 💡 | Fewer escalations; preserves relationships; enables partial recoveries while resolving disputes 📊⭐ | Service‑intensive businesses (SaaS, professional services) with frequent disputes | Reduces friction, clarifies ownership, and prevents disputes from stalling cash ⚡ |

Data‑Driven Performance Analytics & Continuous Improvement | Medium‑High, BI, data governance, testing frameworks 🔄 | Robust data infrastructure, BI tools, analytics team, A/B testing capability 💡 | Improved KPI performance (DSO, collection rate, bad debt); better forecasting and continuous gains 📊⭐ | Organizations committed to iterative optimization and executive reporting | Empirical decision‑making, measurable improvements and scalable best practices ⚡ |

From Risk Management to Cash Flow Orchestration

The common mistake in credit risk management is treating it as a narrow underwriting function. In a professional services firm, risk sits across the full invoice lifecycle. It starts when you accept a client on terms. It grows when scope expands without updated controls. It gets harder when billing is delayed, disputes aren't classified, reminders are inconsistent, and payments arrive without clean application.

That's why the best credit risk management best practices work as a system.

Predictive scoring without dynamic limits leaves exposure unmanaged. Omnichannel collections without a clean payment portal creates friction at the moment the client is ready to pay. Automated outreach without dispute routing annoys good clients and stalls real resolution. Analytics without workflow execution gives you prettier reports but not better outcomes.

CFOs and controllers in the $3M to $50M range usually don't need a giant transformation program. They need tighter operating design. A documented policy. Clear thresholds. Faster routing. Better payment experience. Fewer manual touches. More confidence that the receivables ledger reflects reality.

That's where accounts receivable automation changes the game. Not because automation replaces judgment, but because it protects judgment for the moments that actually need it. Routine reminders, risk refreshes, payment matching, segmentation, and status tracking should happen automatically. Finance should spend time on exception handling, client decisions, and cash planning.

A practical implementation path is usually straightforward:

- Start with visibility: Clean aging, unapplied cash, dispute categories, and exposure by client.

- Add control rules: Credit thresholds, escalation stages, and standard collection cadences.

- Automate repetitive work: Reminder sequences, task routing, portal links, and cash application.

- Layer in intelligence: Risk scoring, dynamic limits, and next-best-action logic.

- Review and recalibrate: Keep policies current as your client base and service mix change.

For many firms, QuickBooks AR automation or a connected AR platform is the fastest route to operational discipline because it reduces dependence on manual exports, inbox follow-up, and side spreadsheets. The right setup helps reduce DSO, improve cash flow, and give firm owners better confidence in what will convert to cash.

Visuals can help leadership absorb this quickly. A waterfall chart showing invoice volume narrowing into disputes, overdue balances, and collected cash is effective. A heat map of clients by exposure and payment risk makes prioritization visible. A cinematic dashboard view that contrasts "manual AR chaos" with "automated control tower" also works well for internal buy-in.

If you're evaluating systems, keep the standard simple. The platform should help you monitor continuously, act early, reduce manual work, and keep the client experience professional. Resolut is one option built around that model for professional services, combining credit, collections, payment workflows, and cash application in a single operating layer.

If you want a cleaner AR operation without turning collections into a blunt instrument, Resolut is worth a look. It automates AR for professional services in a way that stays consistent, accurate, and human.