Credit Risk Management in Banks: A CFO's AR Playbook

Apply credit risk management in banks to your AR. A practical guide for CFOs to reduce DSO, improve cash flow, and automate receivables with AI.

If banks treat every loan as a risk asset that needs monitoring, why do so many professional services firms still treat accounts receivable as an administrative afterthought?

That gap is expensive. A bank would never wait until a borrower is badly delinquent before asking whether the original terms made sense, whether the exposure was too large, or whether early warning signs were missed. Yet many firms still run AR that way. They invoice, wait, remind, escalate late, and hope client relationships carry the balance.

The discipline behind credit risk management in banks can be adapted to your receivables operation without turning your finance team into a modeling shop. For a CFO, Controller, or owner, the practical question isn't how to build a bank. It's how to borrow the parts that create control, reduce DSO, and improve cash flow.

Why Your AR Is Not Managed Like a Bank's Loan Book

Most firms think credit risk starts when a client stops paying. Banks know it starts much earlier.

They assess risk before exposure grows. They set limits before concentration becomes dangerous. They monitor signals continuously, not only after loss appears on a report. That operating rhythm changed sharply after the 2008 crisis. The financial crisis was a watershed moment, triggered by systemic failures in underwriting and flawed credit risk models, and the aftermath led to Basel III with stricter capital ratios and risk management standards for banks, as described in this overview of how top banks build credit risk models.

Professional services firms usually do the opposite. Sales closes the deal. Finance inherits the payment risk. Terms stay loose for “good clients.” Follow-up depends on whoever has time. That isn't a collections problem. It's a credit design problem.

What banks do that most firms don't

Banks don't confuse revenue with collectible cash. In AR, that confusion shows up in familiar ways:

- Terms set by habit: New matters or projects start on standard terms without a real view of payment behavior.

- Exposure ignored: One client grows into an oversized share of receivables before anyone flags concentration risk.

- Collections delayed: Teams wait for aging buckets to worsen instead of acting on weak signals early.

- Responsibility split: Sales owns the relationship, finance owns the chase, and no one owns total exposure.

Practical rule: If your first serious intervention happens after an invoice is past due, you're managing lateness, not risk.

That's why even basic concepts like client selection, term setting, and invoice prioritization matter more than many firms realize. A tighter definition of credit worthiness helps finance teams move the conversation upstream, before billing turns into a recovery exercise.

The AR version of underwriting discipline

A bank's loan book and your receivables ledger aren't identical. But the logic transfers well.

Each client engagement creates exposure. Each invoice has a probability of being paid on time, late, partially paid, or disputed. Each delay ties up working capital. Each write-off is a credit loss, whether or not you use that language internally.

The operational shift is simple to describe and harder to enforce. Stop treating AR as a static report. Start treating it as a live portfolio with entry rules, monitoring rules, and intervention rules.

That's where bank-grade principles become useful. Not as theory. As a control system.

The Three Levers of Bank Credit Risk Management

Banks don't manage credit risk with one number. They break it into separate questions, because each question leads to a different action.

At the core are Probability of Default (PD), Loss Given Default (LGD), and Exposure at Default (EAD). Those sound technical, but for a services firm they translate cleanly into client and invoice decisions.

PD asks who is likely to pay late or not at all

PD is the likelihood that a borrower defaults. In AR terms, it's the chance that a client won't pay according to terms.

A bank under the Internal Ratings-Based approach estimates PD internally, and that estimate directly affects the capital it must hold. Risk weights can range from 20% for AAA-rated exposures to 150% for lower-quality ones, which creates a direct incentive to manage credit quality, as outlined in this explanation of IRB credit risk modelling.

You don't need a capital model to use that logic. You need a way to separate clients that deserve standard terms from clients that need deposits, tighter billing cycles, or executive review.

LGD asks what happens if the client doesn't pay

LGD is the share of exposure you expect to lose after default.

In professional services, LGD depends on things banks also care about. Contract structure. Documentation quality. Billing accuracy. Dispute potential. Ability to suspend future work. Senior sponsor involvement. A vague statement of work and weak approval trail usually mean higher loss severity, even if the client eventually pays something.

A useful AR question is: if this account stalls, how much can we realistically recover, and how much effort will it take?

EAD asks how much is actually at risk

EAD is the amount exposed when default occurs.

For a bank, that may include drawn and undrawn commitments. For your firm, it usually means open invoices, unbilled work in progress about to be invoiced, and work still being delivered without fresh payment assurance. Many firms underestimate this because they look only at overdue invoices and ignore near-term billing that will soon increase exposure.

The most dangerous receivable is often not the oldest invoice. It's the account still accumulating new exposure while payment quality is deteriorating.

How these three levers work together

Think of each client as a small credit portfolio.

Lever | Bank question | AR equivalent | Typical action |

|---|---|---|---|

PD | How likely is default? | How likely is this client to pay late, dispute, or stall? | Adjust terms, reminders, approval thresholds |

LGD | How much will we lose? | If payment breaks down, how much can we still collect? | Tighten contracts, secure approvals, escalate faster |

EAD | How much is exposed? | What total open and pending amount is at risk? | Cap exposure, require deposits, pause work |

For finance leaders building policy, it helps to review broader strategies for financial risk and compliance that show how governance and monitoring work together. The bank lesson is straightforward. Risk measurement only matters if it changes behavior.

Applying Bank-Grade Analytics to Your Client Ledger

Most firms already have more usable risk data than they think. The problem isn't lack of information. It's that the data sits in accounting, CRM, email threads, and project systems without a clear risk lens.

A bank-grade approach starts by asking which signals predict payment friction. Not just whether an invoice is overdue, but whether the account was drifting toward delay weeks earlier.

Start with operational data you already own

For a professional services firm, the first version of invoice-level risk scoring can be built from plain inputs:

- Payment behavior: Days to pay, broken promises, partial payments, repeated “processing” delays

- Commercial terms: Invoice size, billing frequency, upfront retainer status, exceptions to standard terms

- Delivery signals: Scope changes, pending approvals, disputed line items, missing purchase order details

- Concentration exposure: Open balance by client, by practice area, or by partner-managed book

- External cues: Public stress signals, leadership changes, industry slowdown, funding uncertainty

That doesn't require a data science team. It requires discipline in how signals are captured and used.

Why AI AR automation changes the math

Traditional AR reporting is backward-looking. It tells you what aged. It rarely tells you what's about to slip.

That's where AI AR automation becomes practical, not theoretical. Machine learning models can improve PD precision by 15% to 25% by analyzing alternative data like payment patterns, and 66% of lenders now blend traditional and ML models, according to this review of credit risk analysis using machine learning.

For a services firm, the equivalent is simpler than bank underwriting. You're not pricing securities. You're prioritizing action. Which accounts need a personal call today? Which invoices should trigger a reminder before due date? Which clients should move from monthly billing to milestone billing? Those are high-value decisions.

A practical overview of AI for debt collection is useful here because it reframes collections as an ongoing risk-detection workflow, not a batch of late notices.

Good AR analytics don't replace judgment. They help the team apply judgment before the invoice becomes a problem.

What works and what doesn't

The firms that make this stick usually keep the model lightweight. They don't wait for perfect data. They define a manageable score, test whether it matches reality, and refine.

What tends to work:

- Risk scoring at the account and invoice level

- Weekly review of newly escalated accounts

- Different workflows by risk tier

- Terms changes linked to actual payment behavior

What usually fails:

- One generic collections cadence for every client

- No distinction between dispute risk and liquidity risk

- Static credit reviews done only at onboarding

- AR software for professional services used as a reminder tool, not a decision tool

The shift worth making is conceptual. Your ledger isn't just a list of balances. It's a portfolio of short-duration credit exposures. Once the team sees that clearly, better action follows.

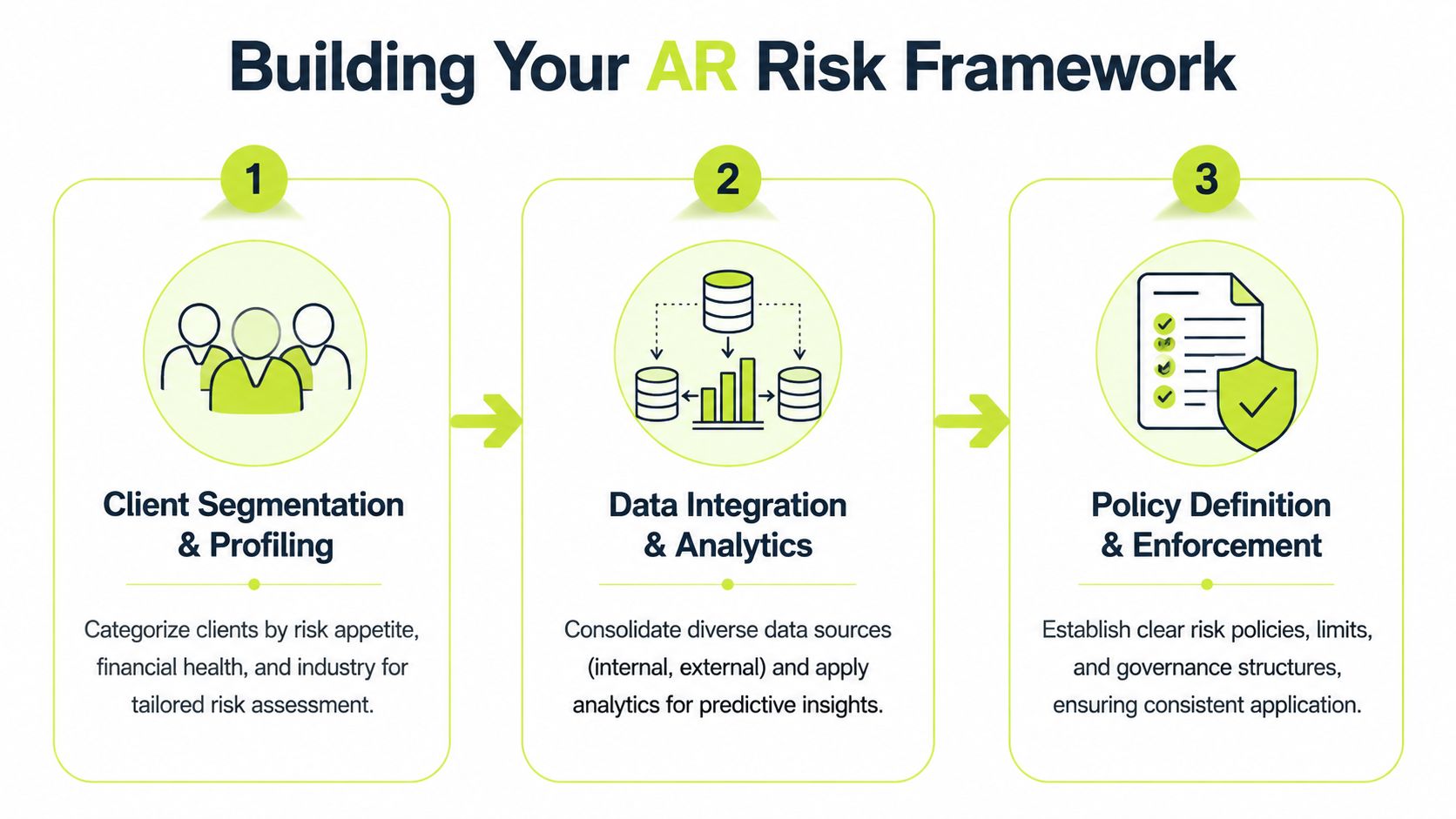

How to Build Your AR Risk Management Framework

A workable framework doesn't need bank complexity. It needs clear rules, ownership, and repeatable action.

The easiest mistake is to focus only on collections messaging. Messaging matters, but it sits downstream of policy. Strong AR control starts before the first invoice goes out.

Pillar one is client underwriting

Banks tightened frameworks because losses force discipline. In the U.S. federal banking system, net charge-off ratios in commercial loans rose to 0.70%, the highest since 2013, and banks strengthened Tier 1 risk-based capital ratios to 14.27%, reinforcing the need to align reserves with risk, according to the OCC's 2025 risk review release.

For a services firm, “capital reserve” translates into a simpler question. How much working capital are you willing to tie up with a given client before payment quality proves itself?

Underwriting in AR should cover:

- Term design Not every client should receive the same terms. New clients, large matters, and exception-heavy projects may need retainers, milestone billing, or shorter due dates.

- Approval authority Someone should own term exceptions. If partners or account leads can extend terms casually, finance loses control before risk even appears.

- Documentation quality Weak contracts, missing approvers, and vague billing language raise collection friction later. Fixing that after invoicing is expensive.

A useful reference point is how modern bank risk management strategies connect governance to portfolio outcomes. The same principle applies in AR. Policy only works when exceptions are visible.

Pillar two is concentration management

Many firms know their biggest clients by revenue. Fewer know their biggest clients by receivables exposure.

That matters because a profitable account can still create cash strain if it dominates the ledger. Concentration rules don't have to be rigid. But they should exist.

Consider setting review triggers around:

- Single-client open exposure

- Exposure by partner or practice

- Exposure growth without payment improvement

- Large unbilled work in progress on already slow accounts

The following situation often surprises many smaller firms: They think they have a collections issue when they really have a portfolio construction issue.

Pillar three is early warning and intervention

Most receivables problems don't appear suddenly. Teams can usually spot changes in behavior if they know where to look.

Watch for:

- Payment timing drift

- More billing questions than usual

- Frequent requests to resend invoices

- Approval bottlenecks inside the client account

- Silence from a previously responsive contact

Operating insight: Early-warning indicators only help if they trigger a predefined action within days, not discussion at month end.

That action might be a courtesy outreach, a term reset, a hold on additional work, or senior involvement from the relationship owner.

For smaller firms, guidance on small business credit risk management can help frame this without overengineering it. The goal isn't to build a compliance department. It's to make receivables decisions consistent enough that cash flow stops depending on memory and improvisation.

Activating Your Framework with AI and Automation

A policy is only real when the workflow enforces it.

Take a common scenario. A client that usually pays on time starts asking billing questions two cycles in a row. The latest invoice sits untouched. The amount is larger than normal, and more work is scheduled next week. In a manual shop, that may sit in someone's inbox until the due date passes. In a risk-managed operation, that account gets flagged immediately and routed into the right path.

What an automated sequence should do

A good accounts receivable automation workflow shouldn't blast the same reminder to every client. It should adapt tone, timing, and escalation based on risk and relationship context.

A practical sequence often looks like this:

- Low-risk invoice nearing due date Send a polite reminder with invoice copy, payment options, and a clear contact path for questions.

- Moderate-risk account showing drift Add earlier follow-up, confirm receipt, and ask for payment timing in plain language.

- High-risk account with rising exposure Escalate channel mix, involve the account owner, and consider pausing new work until payment clarity improves.

- Dispute-coded account Route to a workflow that resolves documentation or approval friction before standard collections pressure increases.

QuickBooks AR automation and similar workflow integrations become useful in these scenarios. The accounting platform remains the system of record. The automation layer handles prioritization, reminders, escalation logic, and task routing so the team acts consistently.

Why co-pilot models work better than full autopilot

Finance teams often hesitate because they assume automation means handing client communication to a machine without control. That's not the model that works best.

The stronger approach is co-pilot. AI handles routine risk flagging, sequencing, and follow-up prompts. Humans step in on exceptions, sensitive accounts, and relationship-heavy decisions. The rise of co-pilot AI modes in finance has been shown to reduce manual AR work by 50% while boosting recoveries by 15% to 25% through personalized automated outreach, based on this discussion of risk management solution challenges and co-pilot workflows.

Let automation handle repetition. Let people handle judgment, negotiation, and client context.

That split matters in professional services because your collections process also signals how your firm operates. Sloppy follow-up weakens credibility. Overly aggressive automation can damage trust. A calibrated system protects both cash and relationship value.

Choosing tools without overbuying

You don't need enterprise banking software to activate bank-grade discipline in AR. You need a tool stack that connects your ledger, client data, and workflows.

For finance leaders comparing options, a practical financial services technology guide is useful for thinking through integration, control, and process fit. In this category, platforms vary. Some focus mainly on reminders. Others support risk identification, collections orchestration, payment workflows, and human review.

Resolut is one example in the AR automation category. It combines credit policy and risk assessment, intelligent risk identification, omnichannel collections, and human-in-the-loop workflows in one operating layer for receivables teams. For a firm that wants consistency without adding headcount, that's the kind of design to evaluate.

Measuring the ROI of a Risk-First AR Strategy

A risk-first AR program should show up in operating numbers quickly. Not only in collections activity, but in cash reliability.

The first mistake is measuring effort instead of outcomes. More reminders sent doesn't mean the system is working. What matters is whether receivables are aging more slowly, cash is arriving more predictably, and fewer accounts require late-stage intervention.

What to track every month

A CFO-level dashboard should include:

- DSO The cleanest signal of whether billing and collection speed are improving.

- Collection Effectiveness Index Useful for separating real collections performance from simple billing volume changes.

- Receivables over 90 days This shows whether risk is being contained early or merely shifted downstream.

- Promise-to-pay kept rate A practical indicator of whether client commitments are reliable.

- High-risk exposure share The open balance tied to accounts already showing warning signs.

AR Performance Before vs. After Risk Management

Metric | Traditional AR (Manual) | Risk-Managed AR (Automated) | Impact |

|---|---|---|---|

Invoice follow-up | Inconsistent, staff-dependent | Rule-based and timely | Better consistency |

Client prioritization | Based on aging only | Based on risk and exposure | Earlier intervention |

Escalation | Reactive | Trigger-based | Fewer surprises |

DSO management | Reviewed after slippage | Managed during the billing cycle | Faster cash conversion |

Cash flow visibility | Limited | Forward-looking | Better planning |

What finance leaders usually notice first

The earliest improvement is rarely dramatic write-off reduction. It's control.

Teams know which accounts need attention. Partners can see where delivery is outrunning payment quality. Controllers stop relying on heroic manual follow-up at month end. Cash forecasting gets steadier because invoice risk is visible earlier in the cycle.

That is the essential value of applying credit risk management in banks to receivables. You move from chasing balances to managing exposure.

Resolut automates AR for professional services with workflows built for consistent follow-up, risk-aware escalation, and human oversight when nuance matters. If you're looking to reduce DSO and improve cash flow without making collections feel mechanical, Resolut is designed to bring that control into day-to-day finance operations.