Boost Cash Flow: AR Escalation Procedures for CFOs 2026

Optimize accounts receivable escalation procedures to cut DSO, boost cash flow, and streamline collections. Essential guide for CFOs on triggers, comms, &

A client pays like clockwork for two years. Then one invoice slips past due. Your team sends a reminder, gets a polite reply, hears that AP is “looking into it,” and moves on. Two weeks later, nothing has cleared. The partner on the account doesn't want finance pushing too hard. The controller wants a firmer note. The owner wants cash in the bank without turning a solid client relationship into a collections fight.

That tension sits inside most professional services firms.

Late payment rarely starts as a collections problem. It usually starts as an ownership problem. No one has defined what happens when a client stops responding, disputes scope after the work is done, or promises payment and misses the date. Without formal escalation procedures, every overdue invoice becomes a judgment call. Judgment calls create inconsistency. Inconsistency creates delay. Delay pressures cash flow and makes your team sound more emotional than professional.

The fix isn't aggression. It's structure. Good escalation procedures give your firm a controlled way to move from reminder to action, with the right tone, the right owner, and the right level of authority at each step.

Beyond Reminders Why Your Firm Needs Formal Escalation Procedures

A reminder sequence alone won't protect your cash flow.

What breaks down in most firms isn't effort. It's the absence of a shared rulebook. Finance sends emails. Client service reassures the account team that the relationship is fine. A partner says to “give them a few more days.” Meanwhile, the invoice ages, and no one can say who owns the next move.

Informal collections create avoidable friction

In practice, informal follow-up creates two bad outcomes.

First, some clients get chased too hard because a team member is frustrated. Second, other clients get too much slack because they're strategic, familiar, or politically sensitive. Neither approach is disciplined. Both train clients that your payment process is negotiable.

Practical rule: When collections relies on personality, clients learn to wait for the least assertive person in your firm.

Formal escalation procedures solve that by making the process predictable. They define when an issue moves upward, what information travels with it, and what authority changes hands. That's consistent with the broader definition of escalation as a governed transfer of authority rather than a random reaction, a concept with roots in risk control and decision-making under pressure in both military and operational settings, as outlined by the U.S. Naval Institute's historical perspective on escalation.

Preserve the relationship by removing emotion

Owners often hear the word “escalation” and assume conflict. In well-run firms, it means the opposite. It keeps conflict from creeping into the process.

A documented path lets your team say, calmly and professionally, that the invoice has entered the next stage. The message is no longer “we're upset.” The message is “this is our process.”

That matters when you're dealing with clients you want to keep. A stronger note can still be respectful. A partner call can still be constructive. A legal review can still be measured. If you want a useful outside perspective on how late-payment risk develops before it becomes default, Comfi's guide on preventing payment default is a worthwhile read.

For firms tightening their written notices, it also helps to align escalation language with a proper dunning letter process, so your outreach sounds deliberate rather than improvised.

What good looks like

A formal process does three things at once:

- Protects client goodwill: The tone stays controlled because steps are predefined.

- Protects internal alignment: Finance, partners, and delivery leads know when the issue changes hands.

- Protects cash flow: No invoice sits in limbo because someone is avoiding an uncomfortable call.

That's the shift. Escalation procedures aren't a last resort. They're the operating system that keeps overdue receivables from becoming relationship problems and write-off discussions.

Designing Escalation Triggers and Timelines

Most firms trigger escalation too late.

They wait for a number on an aging report, usually after the invoice has already become a management issue. That's backward. Strong escalation procedures start before the breach, not after it.

Build triggers around risk, not just age

Effective operational guidance says escalations should start before service-level commitments are breached, often when a case reaches 75% to 80% of its resolution time, and organizations should aim to keep routine escalations below 10% of total case volume, according to the CX Foundation's escalation management benchmarks. In AR, that principle translates well. Don't wait until an invoice fully rolls into the next problem category if the warning signs are already visible.

Those warning signs are often behavioral:

- Silence after receipt confirmation: The client received the invoice but stops replying.

- Broken promises: Payment dates are offered, then missed without explanation.

- Recurring disputes: A client repeatedly raises scope or approval questions only after invoice delivery.

- Channel switching: The client replies to the partner but ignores finance.

- Partial cooperation: They acknowledge the debt but avoid committing to a clearing date.

Aging still matters. It just shouldn't act alone. If you're refining how you track this, a clean accounts receivable aging process gives finance better visibility into where delay is routine and where it signals deterioration.

Use a timeline your team can actually follow

Most firms don't need a complicated framework. They need one that gets used.

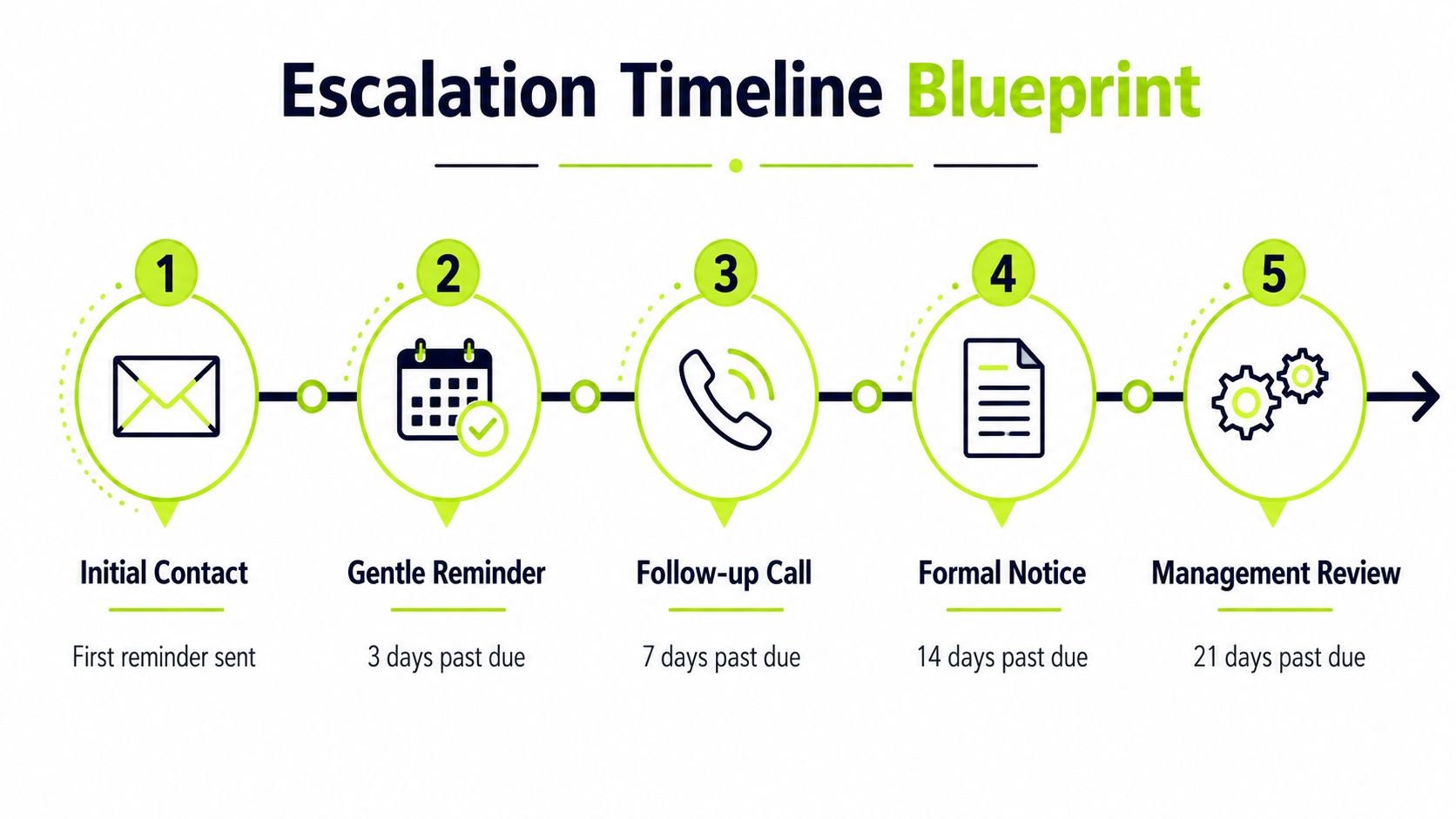

A practical escalation timeline for professional services can look like this:

- Pre-due confirmation Confirm receipt, correct billing contact, and any PO or approval requirement. This catches administrative blockers before they become collections work.

- Early overdue reminder Send a polite note that assumes good intent. Restate invoice amount, due date, and payment method. Ask if anything is preventing release.

- Direct follow-up Move from email-only to human contact. A short call often surfaces the actual issue faster than a fourth reminder.

- Formal notice Document what's overdue, what was previously discussed, and the date by which you need resolution or a payment plan.

- Management review Pull in the account partner, finance leader, or owner only when the decision required has changed. That may involve approving terms, pausing new work, or preparing legal review.

Keep the path narrow

A healthy process doesn't escalate everything. It filters.

Trigger type | Best response | What to avoid |

|---|---|---|

Administrative issue | Correct quickly at the current level | Escalating to leadership too early |

Temporary delay with communication | Short extension with documented date | Endless verbal assurances |

Repeated missed commitments | Move to formal notice | Restarting the reminder cycle |

Commercial dispute | Route to decision-maker with context | Letting finance argue scope |

If every late invoice reaches leadership, your process isn't disciplined. It's overloaded.

The objective is early intervention with selective escalation. That's how you reduce DSO, improve cash flow, and keep escalation procedures from becoming a blunt instrument.

Building Your Escalation Matrix Roles and Accountability

A timeline without named owners won't hold.

Someone still has to send the message, make the call, approve an exception, and decide when the matter leaves routine collections and becomes a commercial or legal issue. That's where an escalation matrix matters.

Assign by decision, not by rank

The strongest guidance on escalation paths is simple. Identify the issue, assess whether it can be resolved at the current level, route it with full context to the defined owner, communicate options, and monitor until closure. The key point is that escalation should follow the decision required, not just seniority, as explained in this project escalation procedure reference.

That principle matters in firms where partners often outrank finance operationally but aren't always the right first escalation point.

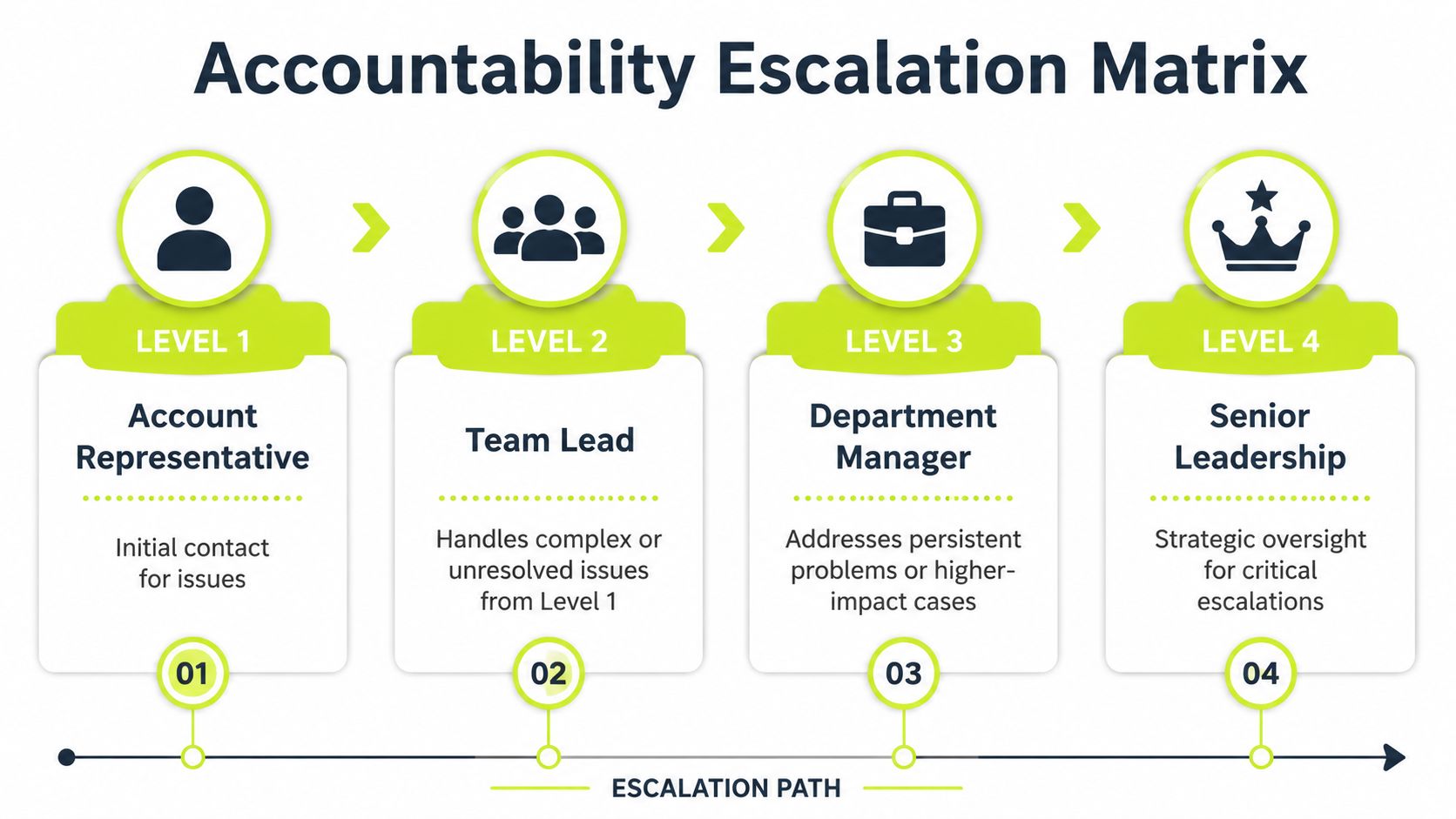

A good matrix looks more like this:

Level | Typical owner | Decision authority |

|---|---|---|

Level 1 | AR specialist or finance admin | Resolve billing delivery, payment status, basic reminder flow |

Level 2 | Controller or finance manager | Approve short extensions, investigate repeated delays, handle structured follow-up |

Level 3 | Account partner or department lead | Resolve commercial friction, protect relationship, align future work with payment reality |

Level 4 | CFO, owner, or outside counsel | Approve hold actions, final settlement posture, legal escalation |

Define handoff rules clearly

Here's where matrices usually fail. Firms name roles but don't define what must travel with the escalation.

Every handoff should include:

- Invoice facts: Amount, date, due date, and what remains open.

- Communication history: What was sent, who replied, and what was promised.

- Root issue: Admin error, dispute, liquidity issue, or silence.

- Requested decision: Extension, partner intervention, work pause, or legal review.

If you've ever had a partner ask, “Why am I only hearing about this now?”, the problem wasn't just aging. It was handoff quality.

A useful parallel comes from regulated environments where traceability matters. Sift AI's guide to audit trails for social care is not about AR, but it's a strong reminder that documented ownership and decision history are what make accountability real.

A short explainer on escalation accountability can help frame this for non-finance leaders:

Prevent the classic ownership gap

The most common failure point is the middle. Finance believes the partner has taken over. The partner assumes finance is still working it. The client experiences mixed messages or none at all.

The handoff isn't complete when the case is forwarded. It's complete when the next owner accepts it and acts.

For professional services firms, that means each level needs a response standard, an acceptance owner, and a clear return path if the issue is resolved. Otherwise, the escalation matrix becomes a diagram no one follows.

Crafting Communication for Each Escalation Stage

The message matters as much as the trigger.

Teams get into trouble when they jump from soft reminders to hard language too quickly, or when they stay polite for too long and sound optional. Good escalation procedures use a controlled progression. The client should feel increasing seriousness, but not a loss of professionalism.

Stage one and two keep the door open

Early communication should assume the issue is fixable.

That doesn't mean vague. It means specific, easy to act on, and low on emotion.

Before due date or just past due, email works well:

Subject: Invoice [number] due on [date] Hi [Name], Sharing a quick reminder that invoice [number] is due on [date]. Please let us know if you need a copy of the invoice, updated billing details, or anything else from our side to process payment. Thanks, [Name]

A few days later, tighten the language slightly:

- State the status clearly: “Our records show this invoice remains unpaid.”

- Ask a direct question: “Can you confirm the payment date?”

- Offer one path to resolution: “If there's an issue with approval or documentation, reply here and we'll address it.”

These messages work because they reduce excuses. They also give finance useful signal. A responsive client with a real blocker should stay in normal workflow. A nonresponsive client is telling you something.

Mid-stage communication gets more explicit

Once a promised date is missed, the tone should change.

Many firms frequently stay too soft. They keep asking for updates instead of requiring action. A stronger note doesn't need threats. It needs clarity.

Follow-up email after a missed commitment:

Subject: Follow-up on overdue invoice [number] Hi [Name], We haven't received payment for invoice [number], and the payment date previously discussed has now passed. Please confirm by [date] whether payment is being released, or let us know immediately if there's a specific issue preventing resolution. If needed, we can also discuss a short payment plan, but we need a confirmed next step. Regards, [Name]

At this stage, the best phone calls are short and controlled. Don't argue invoice history line by line unless the client raises a real dispute. Your objective is to establish one of three outcomes: payment date, documented issue, or escalation to a decision-maker.

“I'm calling to confirm whether this is a timing issue, a dispute issue, or an approval issue. Once I know that, I can route it correctly.”

That sentence keeps the conversation operational. It doesn't invite a debate.

Late-stage communication should sound formal, not hostile

When the invoice is materially overdue, your message should communicate that the matter has moved into a formal process.

That usually means:

- Reference prior contact: Show the client this isn't the first request.

- Name the current status: “This invoice is now in formal review.”

- Set a response deadline: Ask for payment or a documented resolution path.

- State the consequence neutrally: Partner review, work pause, revised terms, or legal review.

For written notices, it helps to use a structure similar to a debt recovery letter template so the language stays consistent across team members.

A practical progression by channel often looks like this:

Stage | Best channel | Tone |

|---|---|---|

Early reminder | Helpful and specific | |

No response | Email plus call | Direct and calm |

Missed promise | Call plus written recap | Firm and structured |

Formal escalation | Formal email or letter | Reserved and procedural |

What doesn't work

Several patterns weaken collections fast:

- Apologetic language: “Sorry to bother you” tells the client your process is negotiable.

- Emotional pressure: Frustration invites defensiveness.

- Long messages: The more words you add, the easier it is to ignore the ask.

- Undefined next steps: “Please advise” is too easy to sidestep.

The strongest AR communication sounds steady. Not passive. Not dramatic. Just clear about what's due, what happens next, and who now owns the matter.

Measuring the Performance of Your AR Escalation Process

If you don't measure escalation quality, your process will drift.

Some firms celebrate speed. Others celebrate low complaint volume. Neither tells you whether your escalation procedures are improving collections or just moving work around. The better question is whether the triggers are precise and whether the escalations that do occur effectively resolve issues.

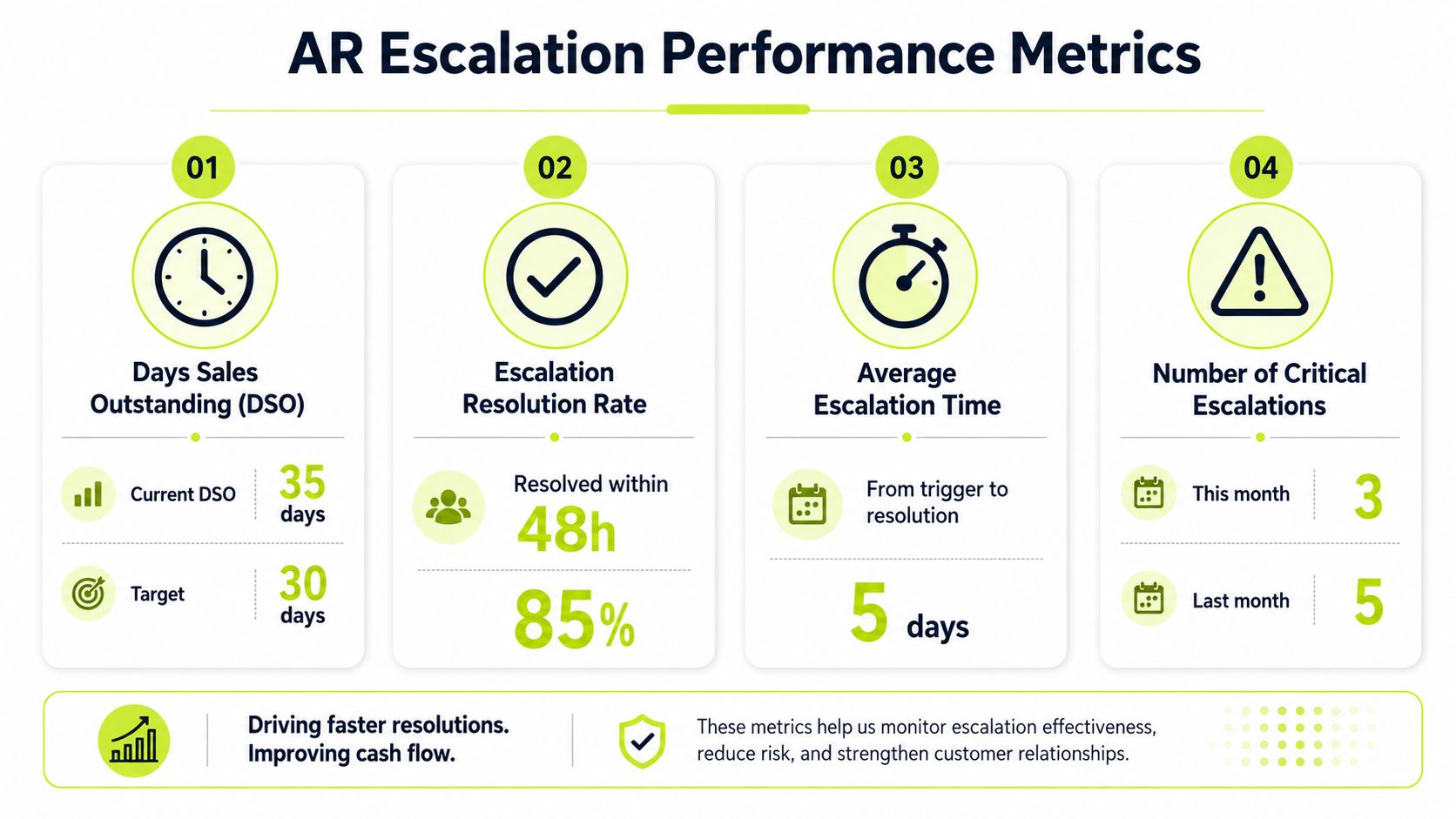

Track financial and operational outcomes together

Finance leaders already watch DSO, Collection Effectiveness Index, and average days delinquent because those measures show whether receivables are converting into cash. Keep using them.

Then add escalation-specific measures beside them:

- Escalation rate: How much of invoice volume enters formal escalation

- Repeat escalations: Cases that bounce upward more than once

- Time to resolution after escalation: Whether escalation shortens the path to cash

- Post-escalation outcome: Paid, disputed, placed on plan, or sent for legal review

Don't reward speed alone

Research on escalation of care makes an important point that applies well beyond healthcare. Faster escalation isn't always better. Success depends on the quality of the trigger, meaning the ability to identify real deterioration early without creating false alarms or escalation fatigue, as discussed in this research on escalation trigger quality.

That's exactly the trap in AR.

If your team escalates too slowly, cash drifts and client excuses harden. If your team escalates too quickly, you create noise, frustrate good clients, and overload decision-makers with issues that frontline staff could have solved. Precision matters more than raw pace.

Read the metrics like an operator

A few patterns usually stand out:

Pattern | Likely issue |

|---|---|

High escalation rate | Weak invoicing discipline, poor trigger design, or too little frontline authority |

Low escalation rate with poor cash conversion | Team hesitation or unresolved invoices sitting outside the process |

High repeat escalations | Lost context, weak ownership, or unclear closeout rules |

Long post-escalation resolution time | Wrong person is receiving the case, or authority is still unclear |

Measure whether escalation improved the outcome. Don't just measure whether it happened on time.

That's the difference between administrative compliance and genuine control. If you want to reduce DSO and improve cash flow, your process has to prove that the right invoices are escalated at the right time, for the right reason.

Using Automation for Consistent and Effective Escalation

Manual escalation procedures are better than ad hoc chasing, but they still break under volume.

People forget follow-ups. Partners intervene inconsistently. Notes sit in inboxes. A client replies to one person while another person sends a formal notice. In a professional services firm with multiple billing contacts, timekeepers, and account owners, manual coordination gets messy fast.

Automation gives your process teeth

At this stage, accounts receivable automation stops being a convenience and starts acting like a control system.

A good workflow engine can enforce timing, route issues by rule, preserve communication history, and make sure no invoice disappears between AR, delivery, and leadership. That's especially useful when you're trying to reduce DSO without turning collections into a full-time job for senior people.

In practical terms, AR software for professional services should help you:

- Trigger outreach consistently: Messages go out on schedule, even when the team is busy.

- Segment by risk and behavior: Unresponsive accounts, dispute-prone accounts, and reliable clients shouldn't receive the same path.

- Create closed-loop ownership: Every escalation needs an owner, a status, and a next action.

- Support human review where needed: Finance should step in on exceptions, not routine reminders.

AI improves judgment at the edge

The value of AI AR automation isn't that it replaces judgment. It applies judgment more consistently at scale.

That matters because modern escalation design depends on closed-loop execution with clear response standards so issues don't get lost between teams. That risk-control purpose has deep roots in escalation itself, and current guidance emphasizes visible, time-bound accountability in closed-loop systems, as described in this overview of closed-loop escalation pathways.

For finance teams, that translates into cleaner routing and better timing. The system can identify missed promises, detect silence after prior engagement, and move the case to the next owner with context intact. That's a better use of technology than blasting more reminders.

It also fits the way firms work. A controller may want rules. A partner may want discretion. An owner may want assurance that strategic clients are handled carefully. Automation can support all three if the process is documented first.

Where this becomes practical

If your team runs on QuickBooks, Excel trackers, inboxes, and partner memory, you don't need more hustle. You need operational consistency.

That's why QuickBooks AR automation and broader AR orchestration matter most when the firm has already decided how escalation should work. Software can't fix a vague process. It can enforce a good one. When the rules are clear, automation protects tone, timing, accountability, and client experience all at once.

The firms that collect well aren't the ones that sound toughest. They're the ones that stay consistent.

Resolut helps professional services firms put that consistency into practice. Its approach to AR automation supports structured outreach, closed-loop follow-up, and human review where judgment matters most. If you want a more controlled way to improve cash flow without compromising client relationships, Resolut is built for that balance.