How Much Does Cash on Delivery Cost? True Impact

Discover how much does cash on delivery cost your business. We detail hidden operational expenses, DSO impact, and AR automation solutions for finance leaders.

Most advice on cash on delivery starts in the wrong place.

It starts with the carrier fee.

That’s useful, but it overlooks the decision a CFO or controller must make. How much does cash on delivery cost isn’t really a shipping question. It’s an accounts receivable process question. The core issue is whether COD improves cash collection enough to justify the friction it adds to reconciliation, cash application, failed delivery handling, and working capital.

If you only look at the line item on a carrier invoice, you’ll understate the cost badly. The visible fee is the smallest part of the problem. The larger expense sits inside finance operations, where teams spend time matching payments, tracing delivery confirmations, clearing exceptions, and waiting for cash to become usable.

For professional services firms, COD may sound niche. But the lesson applies broadly. Any payment process that relies on manual confirmation, delayed posting, and exception-heavy collection behavior creates the same drag. COD is just the cleanest example of what bad AR design looks like.

The Question Finance Leaders Should Be Asking About COD

The wrong question is, “What does the carrier charge for COD?”

The right question is, “What does COD do to DSO, working capital, and finance labor?”

Most published advice still centers on explicit carrier fees such as USPS collection charges or visible surcharges. That’s incomplete. A more useful finance view is to treat COD as a high-friction receivables workflow with hidden costs in cash handling, security, bank deposits, and manual reconciliation that can total 3% to 5% of transaction value, according to USPS-related analysis summarized here.

COD is not “instant cash” in practice

On paper, COD looks attractive because the customer pays at delivery.

In practice, finance still has to recognize, deposit, verify, reconcile, and post the payment. That means the company may collect money physically before it has clean cash visibility in the ledger. Those are not the same thing.

For a controller, this creates three immediate questions:

- When is the cash usable? Delivery date and cleared, posted cash date often differ.

- Who resolves exceptions? Someone has to match receipts to invoices and investigate gaps.

- What’s the cost of manual handling? Cash movement, security, and reconciliation time all hit operating expense.

Practical rule: If a payment method creates more exception handling than standard invoicing, it belongs in your AR cost model, not just your shipping budget.

The finance mistake I see most often

Owners and operators tend to call COD “safe” because payment happens before the goods are released, or at least at the point of delivery.

That’s too narrow. Safety for finance means predictable settlement, accurate posting, low exception volume, and minimal administrative labor. COD often fails that test. It may reduce one kind of credit risk while creating another kind of process risk.

Short version: a low visible fee can still produce a high total collection cost.

If you’re evaluating COD, don’t ask whether the charge looks reasonable. Ask whether the process belongs in a business that wants tighter controls, faster closes, and cleaner cash forecasting.

Deconstructing the Explicit Costs of Cash on Delivery

Start with the part everyone sees. COD has direct, invoiceable costs, and they vary by carrier, geography, and payment collection method.

Carrier pricing structures are real, but they don’t tell you whether COD makes financial sense. They only tell you what gets billed openly.

The market context matters

COD is shrinking globally as a payment method, but it hasn’t disappeared. According to this review of COD by country, COD’s share of global e-commerce payments is forecasted to decline from 2% in 2022 to 1% by 2026. The same source shows how uneven adoption is. Greece has 85.6% of online stores offering COD, while Nigeria sits at 17%.

That matters because pricing and operational expectations follow market norms. In high-COD regions, merchants may treat these costs as a standard tradeoff for conversion. In lower-COD markets, the economics usually look worse because customer demand for COD is weak and digital payment adoption is stronger.

If you want a broader view of how payment choice affects conversion and checkout design, Marvyn AI's ecommerce payment guide is a useful companion read.

What the explicit cost bucket includes

The visible cost of COD usually includes a mix of:

- Carrier COD fees tied to collection amount or service rules

- Delivery surcharges for the extra collection step

- Payment handling charges when the carrier remits collected funds

- Rural or difficult-route delivery premiums in some markets

- Retry or redelivery charges when collection fails on first attempt

Here’s the problem. Finance teams often compare those fees with ACH or card fees and stop there.

That comparison is too shallow.

A better comparison asks whether a transparent payment rail with straightforward processing is cheaper than a collection method that looks inexpensive but requires manual intervention after the fact. If you're benchmarking visible payment costs against lower-friction alternatives, this breakdown of ACH payment processing fees is a more relevant reference point than another COD fee table.

Why visible fees are only the surface

Visible fees tell you what the vendor charges.

They don’t tell you what your team absorbs. They don’t capture the cost of posting delays, dispute cleanup, or the handoff failures between operations and accounting. They also don’t show the effect on forecasting when receipts arrive with weak remittance detail.

A fee on the shipping invoice is easy to spot. The labor cost of fixing COD exceptions usually hides inside payroll, close delays, and unreconciled cash.

That distinction is where finance leaders separate themselves from operators who only price the shipment.

Unmasking the Hidden Operational Costs in Your AR Process

COD stops looking cheap the moment finance has to post, trace, and reconcile it.

Treat COD as a collections workflow, not a delivery option. The visible carrier fee is only the entry ticket. The actual cost sits inside accounts receivable, where every handoff creates delay, rework, and control risk. As discussed earlier, operators that rely on COD often absorb total costs in the low single digits of transaction value once labor, cash handling, and exception management are included.

Reconciliation is the first hidden bill

COD creates ugly AR work. High volume. Low signal. Too many exceptions.

Your team has to confirm whether the driver collected the right amount, whether the bank deposit matches the delivery record, whether the receipt belongs to the right invoice, and what caused any short pay or missing remittance detail. None of that shows up neatly on a shipping invoice. It shows up in payroll, slower closes, and aging items that should have cleared already.

If you want a baseline for the internal labor burden, the Invoice Processing Cost Calculator is a useful starting point for quantifying administrative cost per transaction.

Cash handling adds security and control costs

Physical collection creates a control environment that digital payments avoid.

Someone must define custody rules, approve exceptions, verify deposit timing, and investigate breaks in the payment trail. If documentation is incomplete, AR ends up stitching together driver logs, bank activity, handwritten notes, and customer emails. That is not a shipping problem. It is a finance process failure with direct cost.

Security matters here too. Cash and check collection increase exposure to loss, theft, and dispute because proof of payment is weaker and chain of custody is harder to defend. Finance leaders should price that risk into COD policy instead of treating it as background noise.

Failed delivery and delayed posting distort DSO

COD also damages cash metrics in ways many teams miss.

A delivered order is not cash in the bank. Funds can sit with the carrier, in transit to deposit, or unmatched in suspense while AR chases documentation. Failed deliveries make it worse because the invoice stays unresolved, inventory stays tied up, and the collection cycle resets. If you are serious about reducing working capital drag, measure COD against what DSO in accounting shows about how long receivables stay outstanding, not against shipping fees alone.

That is the right finance lens.

What finance should track

Do not track COD as a logistics convenience. Track it as a high-friction receivables process.

Cost area | What finance should monitor |

|---|---|

Reconciliation labor | Hours spent matching delivery records, deposits, and invoices |

Cash controls | Custody procedures, deposit timing, and exception approvals |

Exception volume | Short pays, missing remittance, disputes, and unapplied cash |

Posting delay | Time from delivery to bank receipt to ledger application |

Forecast reliability | Whether expected COD receipts are usable for cash planning |

This scorecard gives you the true cost of COD. Carrier fees never will.

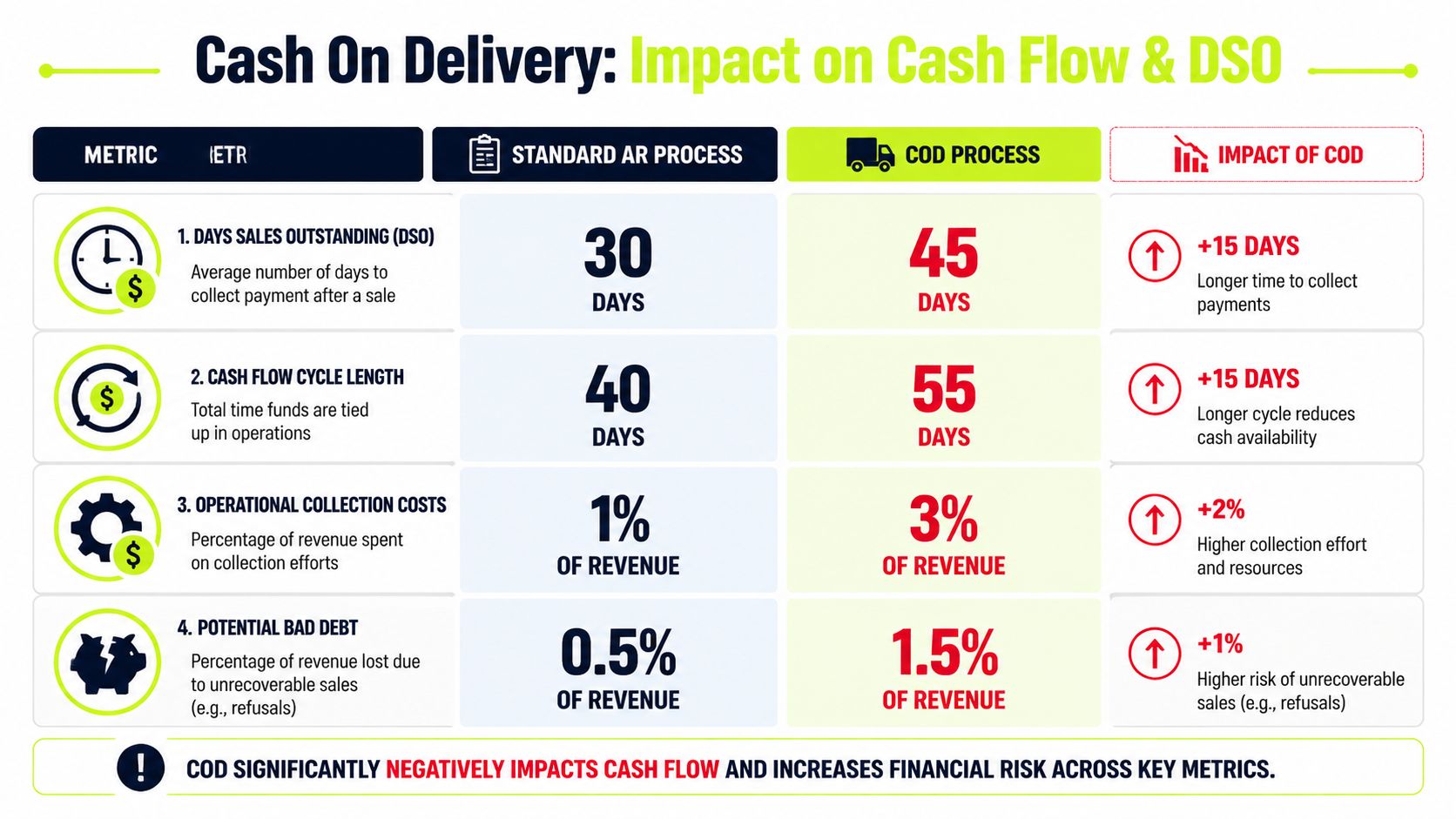

Modeling the Financial Impact on Cash Flow and DSO

Finance should stop asking whether COD increases shipping cost. The right question is how much working capital it traps after the sale is supposedly complete.

According to DYL Ventures’ analysis of COD economics, a retailer shipping 1,000 units monthly with a $120 average order value and a 25% refusal rate can absorb $8,400 in monthly COD overhead, or 7% of gross revenue. That total includes service fees, fixed charges, and $3,750 in return shipping costs tied to refused deliveries. For a finance leader, that is not a delivery issue. It is margin erosion plus slower cash conversion.

Build the model around cash timing, not order status

A COD order can show as delivered while cash is still unusable.

That gap matters. AR cannot close the invoice until funds are confirmed, matched, and posted. Treasury cannot count the receipt with confidence until it reaches the bank. FP&A cannot rely on the number for near-term cash planning if a meaningful share of COD receipts sits in transit or in exceptions. If you want a practical benchmark for the metric itself, review what DSO in accounting actually measures before building the model.

Use three variables in the model:

- Refusal and failure rate How often does the transaction fail to convert into collected cash?

- Post-delivery cash lag How many days pass between delivery confirmation, bank receipt, and ledger application?

- AR touch time per order How many manual actions are required to investigate, match, post, or escalate the payment?

Those inputs determine whether COD protects cash or delays it.

Why COD pushes DSO up

COD is often labeled immediate payment. That is operationally misleading and financially wrong.

DSO does not improve because a driver attempted collection at the doorstep. DSO improves when the business has cash in the bank, the receipt is applied to the right invoice, and the balance is cleared from receivables. Every failed delivery extends that clock. Every unmatched receipt extends it again. Every exception assigned to AR adds labor cost and keeps cash forecasts less reliable.

This is the hidden drag finance teams miss. COD works like a manual accounts receivable workflow attached to a shipment.

Translate COD friction into finance terms

Model the impact in four lines:

- Revenue at risk from refusals Orders shipped but not converted into cash.

- Direct logistics loss Outbound charges plus return handling on failed deliveries.

- Working capital tied up Inventory remains unavailable for resale while the transaction is unresolved.

- Back-office collection cost AR and operations spend time reconciling proofs, deposits, disputes, and unapplied cash.

That fourth line is where many models break down. Companies count carrier fees and ignore internal labor. They should not. If AR specialists spend hours clearing COD exceptions instead of collecting open balances, the business pays twice. Once in labor. Again in slower collections across the rest of the book.

What this means for services and B2B firms

Most service companies do not use physical COD, but many run the same cash drag through manual approval gates, delayed invoice release, offline payment confirmation, and spreadsheet-based reconciliation.

The mechanics differ. The finance effect does not.

Any process that delays receipt posting or increases exception handling will weaken cash visibility and stretch DSO. Firms that want to improve business cash flow should treat these workflows as receivables design problems, not admin inconvenience. My recommendation is simple: model COD and COD-like processes as high-friction AR, assign a cost to every extra day and every extra touch, then remove the steps that do not accelerate usable cash.

Strategic Levers to Mitigate COD Costs and Risk

If you have to offer COD, control it like a risk product.

Don’t offer it broadly. Don’t price it casually. Don’t let operations decide in isolation. Finance should set the rules because finance carries the downstream burden.

Restrict COD to accounts where it serves a clear purpose

COD makes the most sense when the payment risk is real and alternatives are weak.

For everyone else, it’s expensive habit. If a customer has a stable payment record, requiring COD may add friction without adding protection. That’s a bad trade.

Use account segmentation. Reserve COD for situations where the expected reduction in credit risk justifies the operational drag.

Put hard boundaries around the economics

The biggest mistake is allowing COD on orders that can’t carry the full cost structure.

A few policy levers matter immediately:

- Minimum order thresholds so low-margin transactions don’t absorb disproportionate handling cost

- Account eligibility rules based on payment history and dispute behavior

- Documented acceptance standards for what counts as collected, delivered, and closed

- Pre-delivery confirmation steps to reduce avoidable refusals

In some markets, refusal is especially expensive. Mamo Pay’s review of COD costs notes that refused deliveries can create return shipping fees equal to 50% to 100% of the original cost, and undelivered COD items may be held by USPS for 10 days, extending exposure and worsening DSO.

Shift customer behavior with incentives, not lectures

Customers rarely change payment behavior because you explain your back-office pain.

They change when the process is easier, faster, or more favorable to them. If you want to improve business cash flow, don’t frame prepayment or digital payment as an internal efficiency initiative. Frame it as a cleaner customer experience with fewer delivery issues and faster confirmation. This broader guide on how to improve business cash flow is helpful if you’re pairing payment changes with tighter receivables management.

Better payment behavior usually follows better process design, not stronger reminders.

Build a monthly COD review

COD should not sit in the business as a default option with no owner.

Review it monthly. Look at refusal patterns, return costs, exception volume, and posting delays. If a segment consistently creates more rework than collected cash value, remove COD or replace it with a digital pay-on-delivery alternative.

Finance discipline matters here. A payment option should earn its place by producing cash efficiently, not by surviving because no one challenged it.

The Modern Alternative Accounts Receivable Automation

The deeper issue isn’t COD itself.

The deeper issue is a receivables process that depends on manual confirmation, fragmented payment records, and delayed cash application. COD exposes those weaknesses faster than other payment methods do.

Replace manual collection logic with system logic

A modern AR process does three things well.

It gives customers flexible digital ways to pay. It automates cash application so receipts don’t sit in limbo. And it keeps collections activity consistent without forcing your team to chase every exception manually.

That’s why accounts receivable automation matters. It doesn’t just speed up reminders. It changes the operating model so the payment process no longer depends on spreadsheets, inbox monitoring, and one-off reconciliation work.

For firms running on QuickBooks or similar accounting systems, the value is especially clear. Good AR software for professional services should reduce administrative touchpoints, improve payment visibility, and make month-end less dependent on institutional memory.

What modern finance teams should expect

If you’re evaluating AI AR automation, look for practical capabilities rather than glossy dashboards.

The platform should help you:

- Automate cash application so payments post accurately and quickly

- Standardize collections workflows across email, SMS, phone, or portal activity

- Surface risk early when invoices or customers show signs of delay

- Support digital payment options that are easy for clients to use

- Integrate with your accounting stack so the ledger stays current

That’s a true alternative to COD. Not another payment gimmick. A cleaner system.

If you want a closer look at the broader model, this overview of accounts receivables automation gives a solid picture of how the process changes when payment capture, collections, and reconciliation live in one workflow.

Decision standard: If your AR team spends time confirming what got paid instead of influencing what gets paid next, the process needs redesign.

A short walkthrough can help make that concrete:

Why this matters for professional services

Professional services firms don’t usually think of themselves as payment operations businesses.

They are. Every hour of partner review, every invoice held for backup, every payment that arrives without clear remittance, every manual follow-up in QuickBooks or email becomes part of the cash cycle. That’s why QuickBooks AR automation and stronger collection orchestration aren’t nice-to-have tools. They are powerful operational assets.

The firms that improve cash flow most reliably aren’t always the firms with the strictest terms.

They’re the firms with the cleanest systems. They invoice on time, follow up consistently, reconcile quickly, and remove avoidable friction from the customer payment experience.

Resolut automates AR for professional services with a calm, controlled approach to collections, billing, and cash application. If you want a more consistent way to reduce DSO, improve cash flow, and replace manual follow-up with accurate, human workflows, Resolut is built for that.