Master Your Month End Close Playbook

Month end close - Streamline your month end close. Our playbook helps professional services CFOs & controllers reduce DSO, improve cash flow, and achieve a

On the last business day of the month, most professional services finance teams already know how the next week will feel. If billing is late, cash receipts are sitting unapplied, and project managers are still revising revenue inputs, the close turns into a recovery exercise. The books might still get closed, but not with much confidence.

That pattern is common. It also isn’t necessary.

A controlled month end close is less about endurance and more about design. For firms in the $3M to $50M range, the close is the operating rhythm that ties billing, collections, forecasting, and partner reporting together. If AR is sloppy, the close is slow. If the close is slow, cash visibility is weak. If cash visibility is weak, every staffing and hiring decision gets harder than it should be.

In professional services, timing errors rarely stay contained. A missed client invoice affects revenue recognition, AR aging, collections follow-up, and the quality of the management report. The same is true on the expense side. Teams that are also streamlining freelancer expense management usually discover that cleaner inputs upstream make month-end far less dramatic.

The firms that run a reliable close don’t rely on heroics. They build a system. They start before month-end, sequence reconciliations in the right order, and treat AR handoffs as a control point rather than an afterthought. That’s the playbook.

Introduction The End of Month-End Chaos

It is 9:30 a.m. on the first business day. Cash hit the bank overnight, but some receipts are still unapplied. Two project leads are asking for invoice revisions after billing files were already posted. Draft financials are circulating with caveats attached. At that point, the close is no longer a reporting process. It is damage control.

In a professional services firm, month end close sits at the center of cash flow control. Revenue, billing, collections, payroll cost, and project margin all meet here. If AR is incomplete or misapplied, the close slows down. If the close slows down, leaders lose a current view of cash and make staffing, hiring, and collection decisions with stale information.

A messy close usually means the team is finding exceptions too late, not that the accounting is unusually difficult.

That is why I treat close discipline as an AR discipline first. Firms rarely have a pure “close problem.” They have late billing approval, weak cash application, unresolved client disputes, and inconsistent handoffs between billing, project management, and accounting. Those issues surface during close, but they start earlier. Clean bank matching helps, and a standard bank reconciliation format for month-end review gives the team a consistent way to identify unapplied cash before it distorts AR aging and reporting.

Expense inputs matter too. Teams that are also streamlining freelancer expense management usually see the same result on the close side. Fewer coding errors, fewer late submissions, and fewer last-minute accrual debates.

What a controlled close changes

A controlled close improves more than reporting speed.

- Cash visibility improves: AR aging reflects actual collection risk, unapplied cash is cleared quickly, and collection follow-up starts from accurate balances.

- Decision quality improves: leaders can review margin, utilization, and net cash with fewer qualifications and fewer post-close corrections.

- Rework drops: the team spends less time reopening reports and more time resolving exceptions that affect cash.

The objective is a close the business can rely on, completed on schedule, with AR and cash fully tied out. That is how month-end stops being an accounting scramble and starts functioning as a control system for the firm.

Mastering the Pre-Close Setting Up a Seamless Month End

The close is usually won before the month ends. If the team enters day one still waiting on synced systems, unposted time, and half-reviewed billing schedules, the rest of the close will absorb that delay.

That’s why pre-close matters more than is often admitted. The month-end close process typically runs in three phases, and Phase 1 happens 1 to 2 days before month-end, focused on system synchronization and data validation. Starting early is a key factor in reducing errors and preventing mid-close gaps, as outlined in Vena’s month-end close checklist.

Build a pre-close rhythm, not a pre-close scramble

In a professional services firm, “continuous close” doesn’t need to mean a complex transformation. It means routine discipline.

By the 25th or so, finance should already know which projects are ready to bill, which retainers need review, and which matters or engagements have missing time. If your billing model depends on partner approvals, those approvals need an internal due date before the month ends. Waiting until the first business day creates a predictable bottleneck.

A practical pre-close rhythm often includes:

- Daily cash review: Apply receipts every day. Don’t let ACH, wire, or card receipts pile up in a suspense bucket.

- Weekly billing review: Confirm open WIP, draft invoices, and contract-specific billing rules with the people who own the client relationship.

- Expense cutoffs: Push employees and contractors to submit reimbursable items before month-end, not after.

- Payroll and benefits validation: Make sure recurring payroll entries, allocations, and benefit feeds are flowing correctly.

- System sync checks: Confirm CRM, PSA, billing platform, bank feeds, and accounting system are aligned.

Practical rule: If a task can be completed before the final day of the month, it shouldn’t wait for day one of close.

What pre-close looks like in the real world

For a firm using QuickBooks, a PSA platform, and separate banking portals, the failure point is usually not accounting knowledge. It’s fragmented timing. One system closes faster than another. A payment lands without remittance detail. A project manager approves billing after finance has already started draft reporting.

Pre-close solves that by giving each dependency a date and owner.

A simple structure works well:

Pre-close task | Owner | Timing |

|---|---|---|

Review unbilled time and expenses | Billing lead or controller | Before month-end |

Confirm bank feeds and imports | Staff accountant | Before month-end |

Validate payroll entries and recurring journals | Senior accountant | Before month-end |

Clear unapplied cash and suspense items | AR specialist | Daily, then final review before close |

Distribute close calendar and deadlines | Controller | Before month-end |

If you want a practical bookkeeping baseline, Allied Tax Advisors' guide is a useful external checklist to compare against your internal process.

Standardize the handoffs before they become exceptions

Most delays come from handoffs that were never formally defined. Billing assumes accounting will catch the issue. Accounting assumes operations already reviewed it. Collections assumes the aging report is final when it’s still moving.

That’s why I prefer a short written close calendar with explicit owners, due dates, and dependencies. It doesn’t need to be fancy. It does need to be visible.

Bank activity is a good example. If your team still reconciles cash in an inconsistent format, standardization alone can remove a lot of review friction. This bank reconciliation format guide is a useful model for documenting cash activity in a way reviewers can readily follow.

Pre-close checks that pay off later

A few checks prevent a surprising amount of rework:

- Scan for missing invoices tied to completed work.

- Review credit memos that haven’t been matched to open balances.

- Confirm deferred or prepaid items that need current-period treatment.

- Flag unusual contract terms that affect timing.

- Lock down late-entry policy so “just one more adjustment” doesn’t become routine.

Teams that do this well don’t eliminate all close issues. They eliminate the avoidable ones.

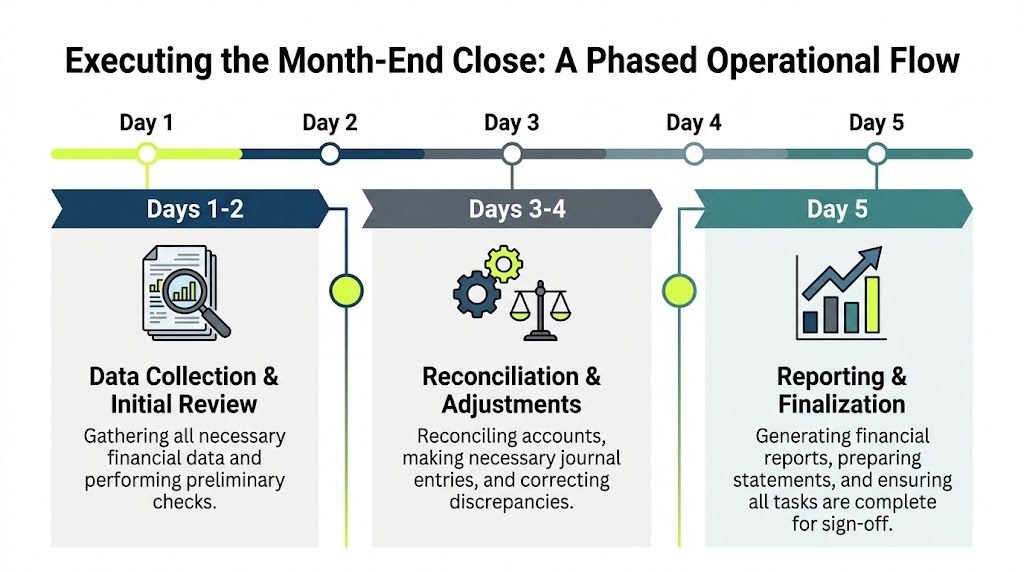

Executing the Close A Phased Operational Timeline

On the first business day after month-end, the risk is not that finance is busy. The risk is that three teams are updating the same story at different speeds. Billing is still issuing invoices, cash is still being applied, and leadership is already asking why revenue or collections moved. If the close sequence is loose, AR aging becomes unstable, reporting loses credibility, and collections starts the month with the wrong priorities.

A controlled close fixes that by forcing order. In a professional services firm, that order matters because the close is tied directly to cash flow. If AR is incomplete or cash receipts are posted late, DSO looks worse than it is in some cases and better than it is in others. Both are problems. One creates unnecessary escalation. The other hides collection issues until they get expensive.

Days 1 and 2 close the subledgers first

The first phase is about freezing the inputs that drive the rest of the close. Post final invoices for completed work. Record cash receipts through cutoff. Clear routine AP, payroll, employee expense, and contractor entries. Book standard accruals that can be supported quickly.

Do not start variance analysis yet. If the AR subledger is still changing, any revenue or working capital discussion will drift as soon as another invoice, write-off, or receipt posts.

For professional services firms, I want five outputs before the team moves on:

- Client invoicing complete for the period

- Cash receipts posted through cutoff

- AR and AP subledgers current

- Recurring journal entries booked

- Known accruals recorded with support

The trade-off is simple. Teams can rush to a draft P&L on day two, or they can hold that time for transaction completeness and avoid rework on days three and four. The second option is usually faster in total elapsed time.

Days 3 and 4 reconcile the accounts that affect cash control

After subledgers stop moving, the close shifts to reconciliation. Start with cash and bank activity. Then move to credit cards, clearing accounts, payroll liabilities, AR exceptions, and other balance sheet accounts that can distort the month if left unresolved.

That order is a control decision. If bank activity is not reconciled first, finance cannot tell whether an AR problem is a true collection delay, an unapplied receipt, a duplicate posting, or a timing item. The aging may be technically open while cash is already in the bank. That is exactly how collection teams waste time chasing clients who already paid.

Teams with heavy receipt volume should use a defined process for automated payment reconciliation workflows, especially when wires, ACH, checks, and card settlements land through different channels. The point is not speed alone. It is keeping the aging report reliable enough to drive collections action on day one of the new month.

A practical review structure looks like this:

Focus area | Why it happens here | What finance should produce |

|---|---|---|

Bank and cash accounts | Establishes the actual cash position and isolates timing items | Reconciled cash balances and open-item list |

AR and unapplied cash | Separates collection problems from posting or application problems | Aging tied to subledger, exception log, unapplied cash detail |

AP and accrued liabilities | Confirms unpaid obligations and expense cutoff | Updated AP support and accrual schedules |

Payroll and related liabilities | Prevents compensation and tax misstatements | Tied payroll entries and liability support |

Key balance sheet accounts | Catches misclassification before reporting goes out | Review-ready workpapers |

Ownership should be clear at this stage. Staff accountants prepare reconciliations. Senior accountants review support and clear routine exceptions. The controller decides on material judgments, approves nonstandard entries, and blocks late changes that would force the team to reopen completed work.

Day 5 turns closed records into useful reporting

By day five, the numbers should be stable enough to explain, not just print. Management reporting only has value when the underlying ledgers are controlled. Otherwise, every variance meeting turns into a hunt for posting errors.

For a services firm, the day-five review should connect operating activity to cash implications. If revenue increased, did billing keep pace? If utilization was strong, did unbilled time rise anyway? If AR aging worsened, was the cause concentrated in one client, one practice leader, disputed invoices, or delayed cash application? Those are close questions, not just collections questions.

This is also where policy issues surface. A late invoice posted after cutoff is not just a close miss. It pushes out collection timing, weakens the next aging report, and can add days to DSO. Repeated enough times, it becomes a cash forecasting problem disguised as an accounting process issue.

What disciplined execution looks like

A good close has visible gates. People know which tasks are complete, which exceptions remain open, and who can approve the next step.

The team is not chasing support across inboxes and chat threads. Review comments are attached to workpapers. The aging report is issued once it is tied out, not while cash is still being applied. Leadership gets numbers that hold up the next morning.

That consistency improves cash control as much as reporting quality. A five-day close with stable AR, reconciled cash, and documented exceptions gives collections a clean starting point for the new month. A faster close with unresolved receipts and shifting aging usually costs more time later, and it almost always costs visibility.

Navigating Critical AR Reconciliations and Handoffs

For professional services firms, AR is where the close either tightens up or starts to drift. Revenue may be earned correctly and invoices may be issued on time, but if cash application is messy, the balance sheet won’t tell a clean story.

That matters because the AR subledger has to tie to the general ledger before the aging report becomes a useful collections tool.

A major challenge in the close process is the integration between the AR subledger and the general ledger. Unmatched cash applications from partial or multi-channel payments can lengthen close times by 20 to 30 percent, and AI-driven automation can reduce that issue by up to 40 percent through better omnichannel payment reconciliation, according to Ramp’s month-end close process guide.

Where AR breaks during close

Most AR reconciliation issues aren’t dramatic. They’re small mismatches that stack up.

A client sends one wire for multiple invoices. Another deducts a disputed line item without clear remittance. A card payment settles quickly, but the invoice application lags. Someone posts a credit memo after the aging was already circulated. Each item is manageable on its own. Together, they slow review and weaken confidence in the aging.

The common exception categories are usually:

- Unapplied cash: Money is in the bank, but not matched to invoice detail.

- Partial payments: One invoice remains open, but no one has documented whether the short pay was intentional.

- Timing differences: Cash clears before the subledger update or vice versa.

- Credit memos in transit: The customer balance looks overstated until the memo is posted and applied.

- Batch remittance issues: One payment covers several matters, invoices, or entities.

The AR to GL tie-out has to be formal

Teams often say AR is reconciled when what they mean is “close enough to review.” That standard is too weak.

The tie-out should be explicit. The ending AR subledger balance should match the receivables control account in the general ledger, with any difference documented and resolved before the aging report goes to collections or leadership.

A simple handoff standard works well:

- Close cash application for the period

- Resolve or log all unapplied items

- Tie the AR subledger to the GL

- Review aging for stale credits, duplicate balances, and disputed invoices

- Release a dated aging report as the official collections worklist

The collections team should never work from an aging report that finance still considers provisional.

What improves DSO versus what just creates noise

In many firms, collections effort is wasted because the aging report is technically current but operationally unreliable. Collectors call on invoices that were already paid, already disputed, or already offset by a credit. That irritates clients and doesn’t improve cash flow.

The better approach is disciplined payment reconciliation before outreach. If your team is evaluating workflow options, this automated payment reconciliation guide is a practical reference for tightening the handoff between incoming cash and receivable reporting.

For firms using accounts receivable automation, AI AR automation, or QuickBooks AR automation, the gain isn’t just labor savings. It’s cleaner exception handling. The software should separate true collections risk from posting noise, so your team focuses on the invoices that require action.

Common Close Pitfalls That Erode Control and Cash Flow

Most close problems aren’t random. They repeat because the process allows them to repeat.

The biggest misconception is that errors are part of month-end. They aren’t. A large share comes from preventable process design issues. An estimated 88% of errors in the month-end close process originate from manual data entry, according to HighRadius on the month-end close process. When teams rely on copy-paste work across reconciliations, statements, and journal support, both speed and accuracy suffer.

Symptom and correction

A practical diagnosis format helps.

- Symptom: Draft financials keep changing after initial review. Correction: Set a hard internal cutoff for invoices, accrual inputs, and manual journals. Route late items through controller approval.

- Symptom: Finance keeps discovering transactions after bank reconciliation starts. Correction: Confirm bank feeds, card feeds, and manual imports before close begins. Don’t start reconciliation on incomplete data.

- Symptom: AR aging doesn’t match what collections sees in practice. Correction: Clear unapplied cash, review credits, and release one official aging report with a timestamp and owner.

- Symptom: The team depends on one person who “knows how it works.” Correction: Document the close calendar, workpapers, approval path, and review notes in a shared system.

The control failures underneath the symptoms

The visible delay is rarely the root cause. Underneath it, there’s usually one of these issues:

Failure point | What it causes |

|---|---|

Undefined ownership | Tasks stall because no one feels accountable |

Disconnected spreadsheets | Different versions of the same balance circulate |

Weak cross-functional communication | Billing, payroll, and accrual inputs arrive late |

No variance review | Errors survive into final reporting |

Manual rekeying | The same transaction is handled multiple times |

A close process doesn’t become reliable because the team works harder. It becomes reliable because the work is sequenced, assigned, and reviewed the same way every month.

What doesn’t work

Adding another checklist to a broken workflow rarely fixes the problem. Neither does asking the team to “be more careful” with manual entry.

What works is reducing the number of manual touchpoints, tightening review gates, and making late changes visible. If the same issue appears three months in a row, it should become a process change, not a recurring annoyance.

From Chore to Strategy Automation and KPIs to Improve Cash Flow

At a certain point, a manual close stops being a badge of toughness and becomes a drag on the business. Senior finance talent shouldn’t spend its best hours chasing remittance details, reformatting reconciliations, or rebuilding the same AR review every month.

Best-practice close processes use a hierarchical checklist that sequences reconciliations correctly, and automation platforms help enforce that structure with standardized templates and validation. Done well, organizations can reduce close cycles from 7 to 10 days down to 3 to 5 days, according to InScope on month-end close methodology.

Where automation belongs first

Not every accounting task should be automated at once. Start with the high-volume, rules-based work that slows review.

Good candidates include:

- Cash application: Especially where clients pay by ACH, wire, card, or mixed methods

- Bank reconciliations: High-frequency matching with exception routing

- Recurring accrual support: Standard entries with repeatable logic

- AR follow-up workflows: Structured reminders, escalation paths, and handoff tracking

- Template-based close workpapers: One format, one owner, one review path

For professional services teams using QuickBooks, QuickBooks AR automation can be especially valuable when billing volume grows faster than headcount. The point isn’t to eliminate judgment. It’s to stop wasting judgment on clerical cleanup.

If you’re looking at process design in this area, this guide on how to automate accounts receivable is a useful starting point.

The KPIs that actually matter

A close should be measured like any other operating process. The most useful KPIs are simple and behavioral.

Track:

- Time to close

- Number of post-close adjustments

- Open reconciliation items at sign-off

- Aging quality at handoff to collections

- Impact on DSO and short-term cash forecast confidence

If you improve cash application and reduce AR noise, your collections team works better. If collections works better, you start to reduce DSO. If DSO improves, cash planning gets easier. That’s why the month end close is not separate from working capital. It is one of the main mechanisms that shapes it.

A short demonstration of workflow thinking can help make the point:

What good automation feels like

The best AR software for professional services doesn’t make finance invisible. It makes the process dependable.

People still review exceptions. Controllers still approve judgment calls. CFOs still decide what matters. But the team stops spending the first half of close assembling data and starts spending more of it interpreting results.

That’s the shift from chore to strategy.

Conclusion A Predictable Close is a Strategic Asset

A disciplined month end close gives a professional services firm more than timely financials. It gives leadership a reliable view of cash, receivables, margin, and operating risk.

The firms that close well usually follow the same pattern. They prepare before month-end, execute in phases, treat AR reconciliation as a formal control, and automate the repetitive work that slows review. That’s how teams improve cash flow without losing accuracy or judgment.

A predictable close provides operational advantage. It helps finance move earlier, communicate more clearly, and make better decisions with less noise.

Resolut helps professional services firms automate AR with a practical balance of control and efficiency. If you want a cleaner handoff from billing to cash application to collections, Resolut is built for that. Consistent, accurate, and human.