CFO's Guide to AR Regulatory Requirements 2026

CFO's guide to key regulatory requirements for AR. Master rules for data, payments, & collections. Ensure compliance with AR automation in 2026.

Firms that treat compliance as a back-office legal task usually pay for it in slower collections, more write-offs, and more time spent fixing preventable errors.

For a professional services firm, accounts receivable is one of the clearest places to see that cost. AR touches invoice accuracy, client records, payment handling, communication logs, dispute documentation, and collections activity. If those steps are inconsistent, cash slows down and risk rises. The problem is not regulation itself. The problem is an undercontrolled process.

That is the right way to frame regulatory requirements. They are part of operating design. Strong controls in AR improve billing speed, document every client interaction, reduce rework, and give your team a clean audit trail when a dispute or regulator question lands on your desk.

This also affects vendor decisions and outside support. If your process breaks down late in the cycle, even assistance with commercial collections becomes harder because the record is incomplete and the account history is inconsistent.

Treat compliance as a cash flow system. Build it into how invoices are issued, approvals are captured, payment data is stored, and exceptions are resolved. Once compliance lives inside the workflow, you get faster collections, fewer avoidable errors, and a finance function that scales without adding chaos.

The True Cost of Regulatory Mismanagement in AR

A single weak AR process can slow cash, increase write-offs, and leave you exposed the moment a client dispute, audit request, or payment issue surfaces. Treating compliance as an operating control instead of a legal side task fixes all three.

Why this hits finance first

AR failures show up in finance before they show up anywhere else. Days sales outstanding rises. Billing disputes sit open longer. Staff spend time reconstructing account history from inboxes, spreadsheets, and side conversations instead of collecting cash.

That is not an admin problem. It is a control problem.

If your team sends invoices manually, stores client data in scattered systems, and handles payment follow-up without standard documentation, you are running revenue through a process you cannot defend or scale. The immediate cost is slower collections and more rework. The larger cost is management blindness. You cannot fix what you cannot see, and you cannot defend what you did not document.

AR turns regulatory requirements into daily operating decisions. Invoice terms, approval records, payment methods, communication logs, fee disclosures, and dispute files all affect whether cash comes in cleanly. Even a policy choice like adding a card surcharge or service fee needs disciplined execution and clear disclosure. If you are reviewing fee practices, start with this guide to a convenience fee on credit card payments.

Practical rule: If a task affects invoice delivery, payment capture, client communication, or account escalation, treat it as a cash control.

Where the leakage starts

In professional services firms, AR compliance usually breaks down in four places.

- Fragmented records: Account history sits across email threads, accounting notes, CRM entries, and personal reminders. Finance loses time. Collections lose credibility.

- Inconsistent outreach: Different employees use different language, timing, and escalation standards. That creates avoidable disputes and uneven client treatment.

- Weak payment handling: Staff collect card details through ad hoc channels or send uncontrolled payment requests. That raises security risk and increases exception work.

- Poor escalation discipline: Aging accounts drift because nobody owns the decision to pause work, escalate internally, or seek assistance with commercial collections.

The last point is where firms usually lose margin. Delayed escalation extends aging, lowers recovery odds, and forces partners to spend time on accounts that should already be in a defined collections path.

Well-run AR compliance produces measurable financial outcomes. It shortens the time from invoice to cash. It reduces avoidable errors. It gives leadership a reliable record when a client challenges a bill, a payment fails, or outside counsel needs a complete file. That is what good compliance should do. It should improve operating performance while reducing risk.

The Four Pillars of AR Regulatory Compliance

You don't need a law degree to manage regulatory requirements in AR. You need a usable framework.

The modern environment didn't emerge by accident. It was shaped by major rules including HIPAA (1996), the Sarbanes-Oxley Act (2002), PCI DSS, and GDPR, effective in 2018, with newer obligations such as DORA becoming effective in January 2025 for EU entities and the SEC cybersecurity disclosure rule requiring reporting of material incidents within four business days, as summarized in MetricStream's regulatory compliance guide. The takeaway for finance leaders is clear. Annual policy reviews aren't enough anymore.

Data privacy and security

AR teams handle names, emails, billing contacts, service histories, and sometimes sensitive supporting documents. That data has to be governed, not just stored.

For a professional services firm, this means limiting access to client records, defining retention rules, and making sure payment-related information stays inside approved systems. If your collectors are copying account details into personal notes or forwarding client records freely, your process is too loose.

The practical question is simple. Who can see what, and why?

Payment processing integrity

Card payments and bank debits move AR out of bookkeeping and into controlled payment operations. That changes your risk profile.

If your firm accepts cards, payment capture should happen through secure portals and approved workflows, not by email or casual phone handling. If you manage recurring pulls or mandates, the rules around authorization and communication need to be documented. Teams dealing with managing direct debit operations usually learn this quickly because small process errors create avoidable disputes.

If you charge clients for card use, policy design matters too. Firms often create compliance issues by layering fees inconsistently. A useful reference is this guide to convenience fees on credit cards, because the operational issue isn't just whether a fee exists. It's whether the fee is applied, disclosed, and recorded consistently.

Financial reporting accuracy

AR compliance also sits inside your close process. Invoice timing, credits, write-offs, unapplied cash, and dispute status all affect financial reporting quality.

This pillar is less dramatic than privacy or payments, but it's where controllers lose confidence fast. If your aging report doesn't match reality, your collection strategy won't either. Teams start chasing the wrong accounts, revenue forecasting gets noisy, and bad debt decisions lag.

A clean AR ledger is a compliance asset because it produces defensible records, not just cleaner reports.

Consumer protection and collections discipline

Professional services firms sometimes assume collections law only applies to high-volume debt shops. That's too casual.

Any firm that sends repeated payment notices needs rules for message timing, tone, dispute handling, and escalation. The issue isn't just legality. It's consistency. One aggressive collector can create more risk than ten late-paying accounts.

The right model is controlled outreach. Approved templates. Defined escalation paths. Written rules on when to stop, when to call, and when legal review starts.

How Automation Changes the AR Compliance Equation

Automation doesn't make AR compliant. Configuration does.

That distinction matters because a lot of firms buy AR software for speed, then discover they've accelerated bad process. An automated reminder sequence that ignores account disputes, client communication preferences, or regional payment rules can create a cleaner dashboard and a worse compliance posture at the same time.

Bad automation scales mistakes

I've seen firms automate invoice reminders without deciding basic policy questions first. Should reminders pause when a billing contact changes? Should they stop when a dispute is opened? Should they route certain accounts to a relationship manager instead of collections? If those rules aren't built in, the system just repeats avoidable errors faster.

The same problem shows up in AI AR automation. If the tool drafts messages dynamically but your team hasn't defined guardrails on tone, approval, and escalation, you've introduced variability where you needed control.

That's also why firms operating across jurisdictions need to think operationally, not cosmetically. If your invoicing obligations differ by market, process design has to reflect that. Teams looking at improving invoice processing for UAE businesses run into this issue quickly. The lesson applies more broadly. Local invoicing rules and workflow design have to match.

Good automation embeds policy

Well-built accounts receivable automation does something manual teams rarely do consistently. It applies the same rule set every time.

That means you can encode practical controls such as:

- Communication logic: Pause outreach when an account is disputed or already assigned for personal follow-up.

- Approval thresholds: Require review before changing terms, issuing credits, or waiving balances.

- Audit capture: Record who sent what, when it was sent, and which action triggered it.

- Access control: Limit who can edit client records, resend invoices, or alter payment arrangements.

AI AR automation earns its place. Not because it sounds modern, but because it can help enforce timing, consistency, and documentation at scale when the underlying rules are sound.

The best AR automation reduces variability. That's good for compliance, and it's good for cash collection.

What to ask before you buy

Don't evaluate AR software for professional services only on workflow demos. Ask harder questions.

Use this short decision filter:

- Can the system document every client interaction?

- Can it enforce communication rules by account status?

- Can it separate automation from approval when judgment is required?

- Can it support audit readiness without manual reconstruction?

If the answer is no, you're buying activity, not control.

If you want a clearer view of where AI belongs and where it needs supervision, this perspective on AI for debt collection is worth reviewing. The main point is right. Automation works best when finance owns the operating rules.

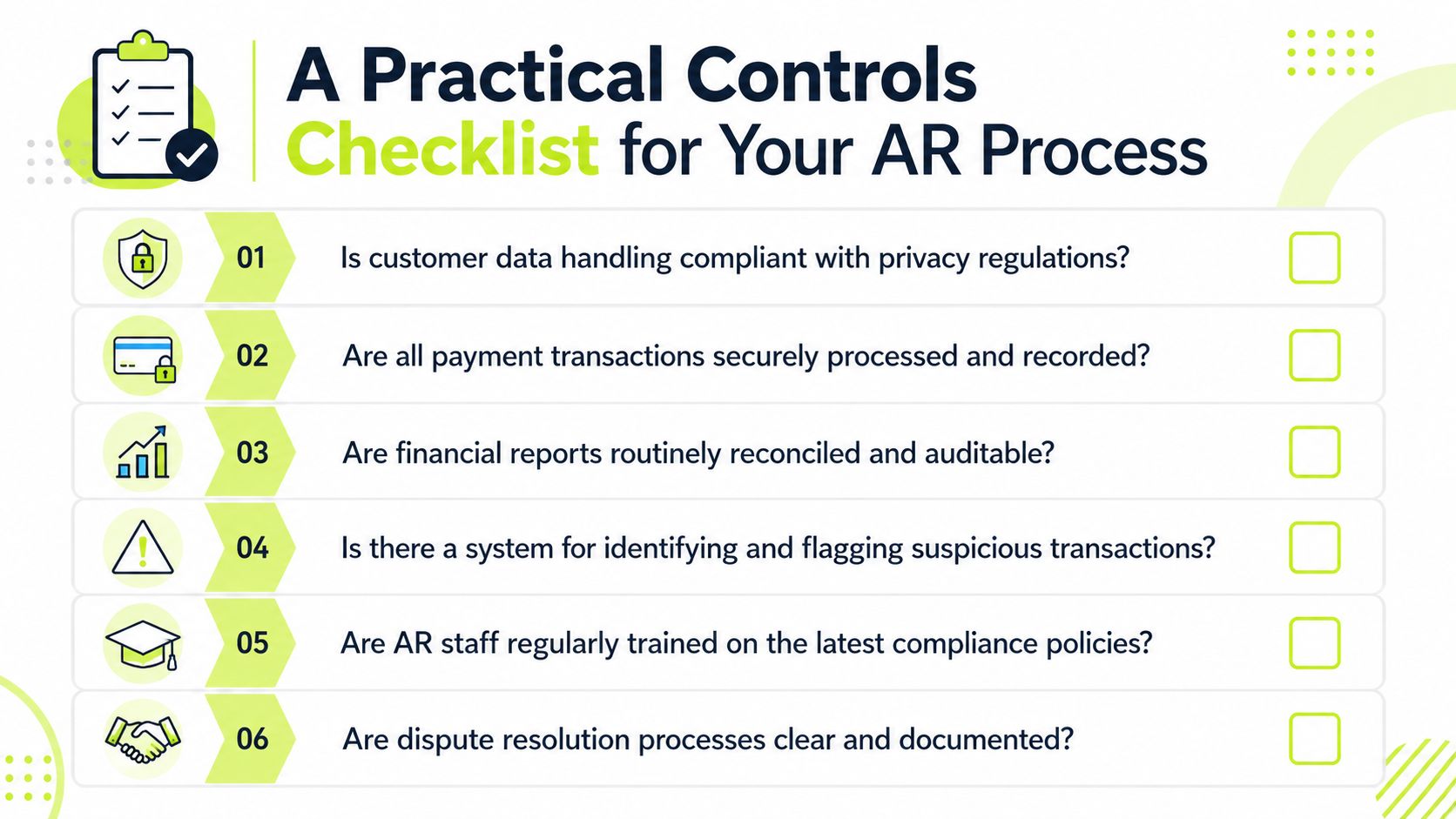

A Practical Controls Checklist for Your AR Process

Most AR teams don't need more policy documents. They need tighter controls and clearer evidence.

That starts with one mindset shift. Process documentation isn't administrative fluff. In regulated environments, technical specifications function as compliance artifacts that map requirements to the underlying rule set with traceability and evidence, as reflected in UK guidance on technical specifications. Your AR playbook should work the same way.

Questions a CFO should ask the team

Don't ask whether the team is “following process.” Ask for proof that the process can be verified.

- How do we control client data access? Show who can view billing contacts, payment details, dispute notes, and account history. If access is broad by default, tighten it.

- How do we send payment requests securely? Show the approved channels, approved tools, and what the team is forbidden to do.

- How do we document communication preferences? If a client asks for billing to go only to a portal, shared inbox, or specific contact, where is that rule stored?

- How do we stop outreach when an invoice is disputed? If your collectors have to remember this manually, the control is weak.

- How do we prove what happened on an account? Produce the audit log. If the story depends on searching inboxes, you don't have a reliable record.

- How do we train and update the team? Policies change. New clients create exceptions. Staff turnover creates drift.

What strong control design looks like

A good AR control environment has three traits. It's explicit, it's testable, and it's hard to bypass casually.

Use this operating checklist:

Control area | What good looks like |

|---|---|

Invoice generation | Standardized terms, approval for exceptions, documented client-specific requirements |

Client communications | Templates, timing rules, dispute pause logic, centralized history |

Payment acceptance | Approved processors, secure links, restricted handling of sensitive data |

Cash application | Reconciliation routines, exception queues, documented adjustments |

Disputes and credits | Clear ownership, approval workflow, timestamped resolution trail |

Operator's view: If a control can't be demonstrated on demand, assume it will fail when pressure rises.

A useful benchmark is to compare your current process against a more formal internal control framework. This guide to accounts receivable internal controls gives a practical structure finance teams can apply without turning the process into bureaucracy.

Where firms usually fall short

The failure usually isn't a missing policy. It's weak execution between systems.

QuickBooks AR automation, for example, can help with consistency if it's tied to documented approval and reconciliation rules. But if the accounting system, inboxes, and payment workflows all tell different stories, the process remains fragile.

The standard should be higher. Your AR system should let a controller verify account status, outreach history, and payment evidence without asking three people and opening six tools.

Using AR Platforms to Operationalize Compliance

Spreadsheets don't operationalize regulatory requirements. They hide process gaps until a dispute, audit request, or collection issue exposes them.

A dedicated AR platform changes that because it turns policy into workflow. Rules stop living in tribal memory and start living in the system.

What a platform should actually enforce

The right platform does more than send reminders. It should control the sequence, the channel, the approvals, and the evidence trail.

That includes capabilities such as:

- Configurable workflows: Outreach changes based on account status, dispute flags, or customer segment.

- Role-based access: Billing clerks, controllers, and leadership don't all need the same permissions.

- Centralized audit history: Every invoice touchpoint, promise to pay, resend, and note lives in one record.

- Secure payment experience: Clients pay through controlled portals instead of improvised requests.

- Exception management: High-risk, high-value, or sensitive accounts route for human review.

That's how you reduce DSO without creating compliance drift. You make the compliant path the default path.

Why this matters for professional services

Professional services firms have a specific AR problem. Client relationships are valuable, invoice amounts are often material, and disputes are usually nuanced. That makes informal follow-up dangerous.

A partner may want a softer touch. A controller may want tighter collections. An account manager may promise an extension without documenting it. A platform gives finance one operating model that still allows judgment where judgment is appropriate.

Here's the practical gain. Teams spend less time figuring out what happened on an account and more time deciding what to do next. That improves cash flow because aging review becomes cleaner, follow-up gets faster, and exceptions are visible earlier.

A short product walkthrough is useful here because it shows what workflow enforcement looks like in practice.

The decision standard I'd use

If you're evaluating accounts receivable automation, don't ask whether it saves clicks. Ask whether it gives your finance team more control.

Use this standard:

- Does it improve cash visibility?

- Does it reduce inconsistency in collections behavior?

- Does it produce an audit-ready record without manual cleanup?

- Does it support QuickBooks AR automation or your core ERP cleanly enough to avoid duplicate work?

If the platform can't answer those questions well, it won't simplify your regulatory requirements problem. It will just move it.

From Regulatory Burden to Operational Excellence

The firms that handle regulatory requirements well don't obsess over rules in the abstract. They build disciplined operating systems.

This is the fundamental shift. AR compliance isn't a side task for legal or a once-a-year review item for finance. It's part of how you invoice, communicate, collect, document, and close. When those activities are controlled, the payoff isn't just lower risk. You get cleaner reporting, fewer disputes, faster decisions, and more predictable cash flow.

For CFOs, controllers, and owners, the message is straightforward. Treat AR as a controlled production process. Define the rules. Assign approvals. Centralize records. Automate what should be consistent. Keep humans where judgment matters.

That's how you reduce friction without relaxing standards. And that's how compliance stops feeling like drag and starts working like an operational advantage.

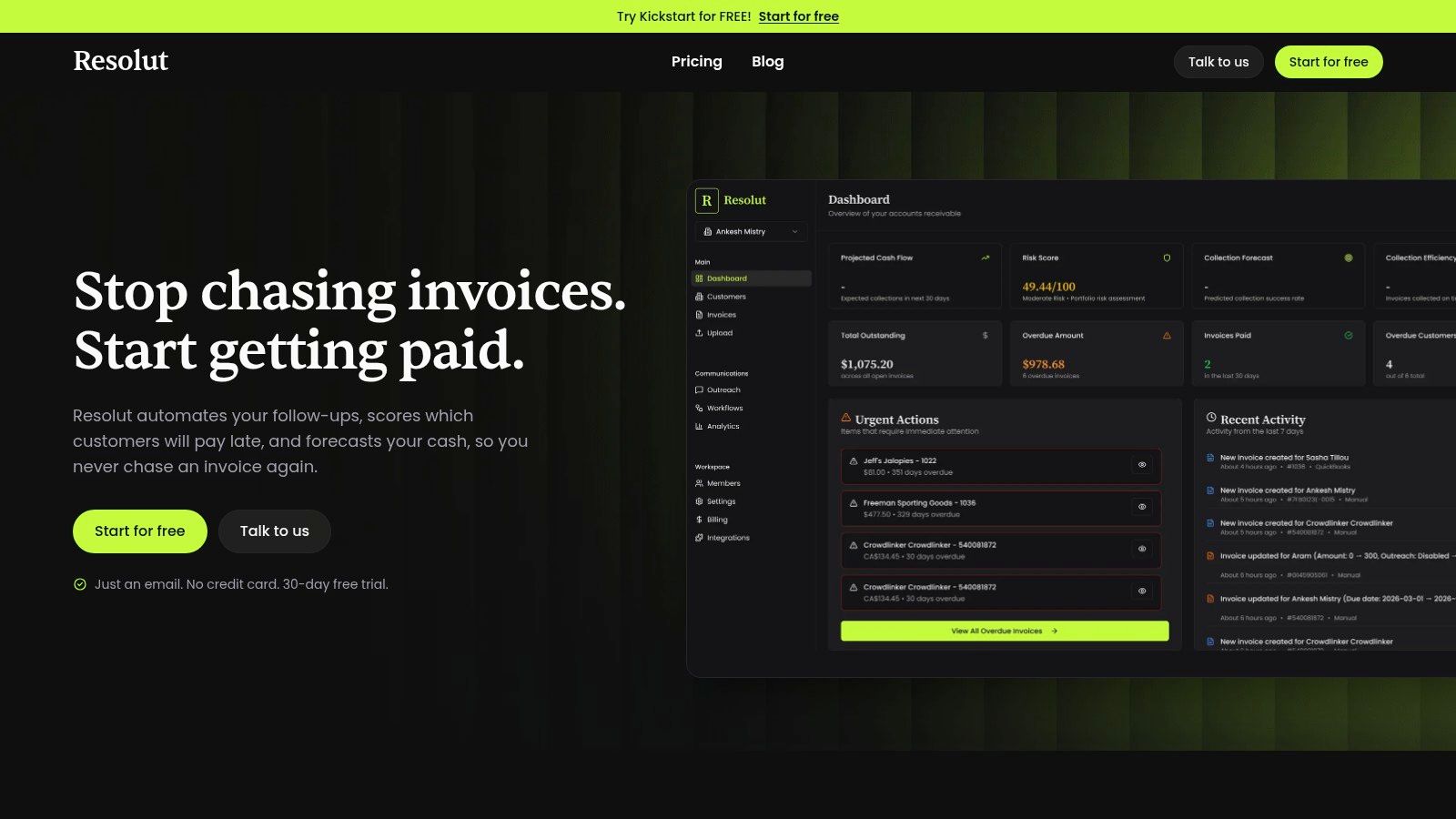

Resolut automates AR for professional services. It helps finance teams run a more consistent, accurate, and human collection process with stronger control over workflows, outreach, and cash application. If you want to reduce DSO, improve cash flow, and bring order to regulatory requirements inside AR, Resolut is worth a look.