Retainer Billing: A Guide to Predictable Firm Revenue

A guide for CFOs on implementing retainer billing. Learn about retainer models, revenue recognition, and how AR automation can reduce DSO and improve cash flow.

Most advice on retainer billing is too small. It treats the model as a payment preference or a sales packaging choice.

That misses the finance issue. For a professional services firm, retainer billing changes how cash enters the business, how quickly receivables convert, how confidently leadership can forecast, and how the market values the firm. If you're running a firm in the $3M to $50M range, that's the conversation worth having.

The practical test isn't whether clients like the word “retainer.” The test is whether your agreement, billing operations, revenue recognition, and collections process create a cleaner path from work performed to cash collected. When they do, retainer billing can reduce volatility, improve visibility, and make accounts receivable automation far more effective than in a pure project model.

The Strategic Case for Retainer Billing

Retainer billing is often framed as a way to smooth workload. For CFOs and Controllers, that's the least interesting benefit.

The core value is financial structure. Revenue that starts the month committed behaves differently from revenue that depends on project completion, invoice approval, and follow-up. It gives finance a better base for forecasting, staffing decisions, partner distributions, and working capital planning. If you're trying to build positive cash flow discipline, retainers belong in that conversation.

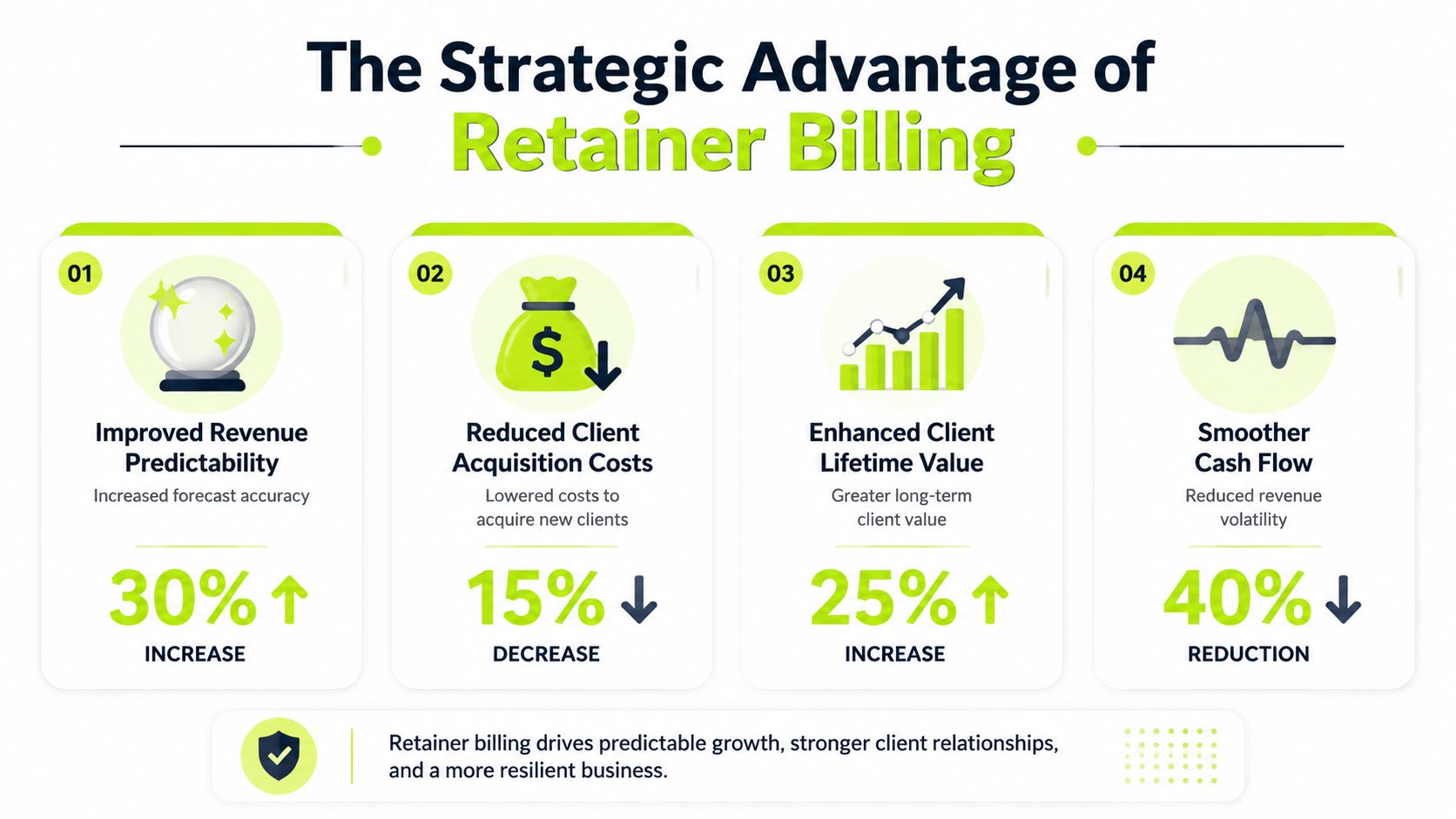

An analysis cited by IOTA Finance's summary of McKinsey research on agency retainer vs project billing found that agencies with at least 40% of revenue from retainer arrangements had 1.3x to 1.6x higher enterprise value multiples than peers, and these firms achieved median EBITDA margins of 20–25%, compared with 12–15% for project-based agencies.

The valuation point matters because buyers, lenders, and investors don't just look at revenue volume. They look at revenue quality. A firm with a meaningful retainer base usually presents less earnings volatility, fewer surprise collection delays, and stronger visibility into near-term cash.

What finance leaders should actually care about

A retainer model changes more than invoice timing.

Financial lens | Project-heavy model | Retainer-heavy model |

|---|---|---|

Forecasting | Revenue depends on variable starts, approvals, and completion | More revenue is committed before delivery |

Collections | AR builds after work is performed | Cash is collected earlier or protected by prepaid balances |

Capacity planning | Hiring often reacts to demand swings | Staffing can follow committed book of business |

Firm value | Revenue quality can look uneven | Predictability typically improves buyer confidence |

That doesn't mean every service should move to a retainer. Commodity project work, one-time implementations, and highly episodic engagements may still belong in milestone or project billing. But many firms underuse retainers because they think of them as a client convenience instead of a capital discipline.

Practical rule: If a service line is recurring, advisory, compliance-based, or requires priority access, it's a candidate for retainer billing.

Where firms get this wrong

Some firms claim to have retainers when they really have delayed project billing. They invoice a “monthly retainer,” but scope is loose, consumption isn't tracked, and overages are discussed after the fact. Finance ends up with the worst of both worlds. Client expectations of continuity, but no real protection on cash.

A real retainer system creates three outcomes:

- Committed cash earlier: Payment is collected before or alongside service delivery.

- Cleaner AR behavior: The team can separate prepaid work from true receivables.

- Operational discipline: Partners, client leads, and finance all know when the balance is low, when scope is exceeded, and when pricing needs to be reset.

That's why retainer billing deserves a seat in valuation and margin discussions, not just in billing administration.

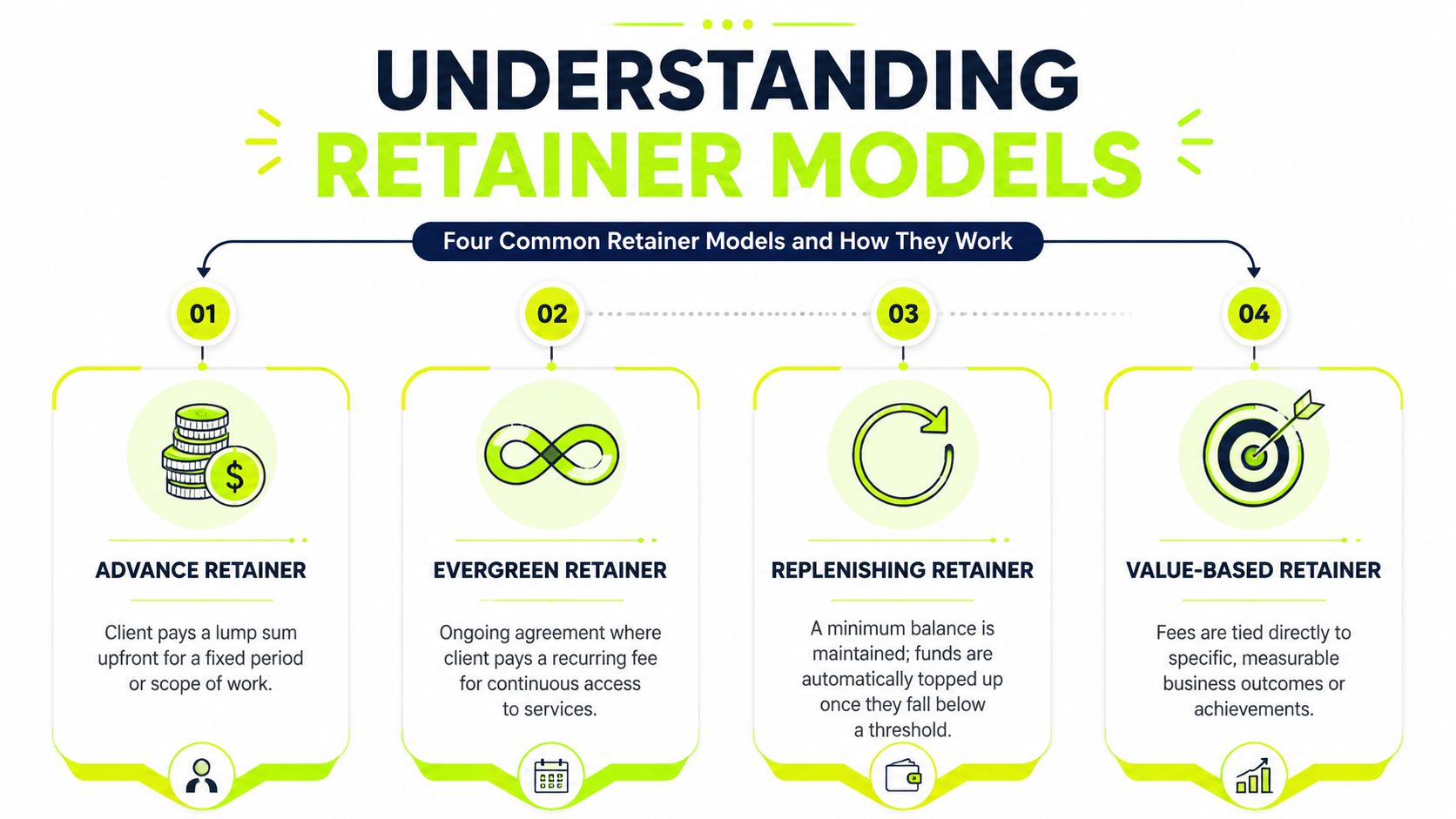

Common Retainer Models and Their Mechanics

Retainer billing isn't one model. Firms use several structures that behave very differently on the balance sheet and in daily operations.

The mistake I see most often is choosing a model based on what feels easiest to sell. Finance should choose based on service pattern, utilization visibility, reconciliation burden, and how much protection the firm needs against slow pay.

If your team is already evaluating recurring billing infrastructure, it helps to compare retainer workflows with subscription invoicing software approaches, because some firms need subscription simplicity while others need draw-down controls.

Advance retainers

An advance retainer is the simplest version. The client pays upfront for a defined period or scope, and the firm earns that amount as the work is performed.

This model works well when the monthly service is stable and the scope is tightly defined. A marketing strategy advisory package, a recurring finance support engagement, or a fixed monthly compliance support arrangement can fit here.

The strength is simplicity. The weakness is drift. If the service expands unnoticed, the retainer turns into an underpriced flat fee.

Evergreen and replenishing retainers

An evergreen retainer behaves more like a funded balance. The client deposits funds, the firm draws down against hours or tasks, and the client replenishes when the balance drops below the agreed floor.

The mechanics matter. As explained in Voklaw's discussion of evergreen retainers and hourly billing, firms often require replenishment once the remaining balance falls to 20–30% of the initial amount. That threshold is what keeps the retainer from becoming a one-time prepayment that runs out.

This model suits legal, consulting, technical advisory, and specialized agency work where effort fluctuates but ongoing access matters.

The evergreen model only works when someone owns the threshold. If no one watches the balance, finance learns the retainer is depleted after the work is already done.

Replenishing retainers as an AR control

A replenishing retainer is a more formalized evergreen model. The agreement spells out the minimum balance, top-up trigger, overage treatment, and whether work pauses when funding isn't restored.

That last point is where cash discipline either survives or collapses.

A replenishing structure is usually strongest when the firm can answer these questions in the contract and in the billing workflow:

- When is the balance considered low

- Who gets notified first

- Whether work continues during replenishment delay

- How out-of-scope work is approved and billed

For firms using QuickBooks AR automation or practice management tools, this is also where integration starts to matter. If top-ups live in email threads and consumption lives in spreadsheets, the retainer is exposed.

Value-based retainers

A value-based retainer ties fees to defined outcomes or strategic access rather than a pure hourly draw-down.

This can work well for high-trust advisory relationships, but only when scope language is unusually clear. Otherwise finance struggles to explain margin compression, and delivery teams struggle to defend what was included.

A simple way to choose among models is this:

Model | Best fit | Main finance risk |

|---|---|---|

Advance | Stable recurring scope | Quiet scope creep |

Evergreen | Variable ongoing usage | Missed replenishment |

Replenishing | High-touch advisory with active balance monitoring | Operational follow-through |

Value-based | Strategic outcome-focused work | Ambiguous performance boundaries |

The right model is the one your firm can price, track, reconcile, and enforce without exceptions every month.

Contract and Revenue Recognition Guardrails

A retainer agreement should make finance operations easier. Too many firms do the opposite. They use friendly language, vague inclusions, and soft overage terms, then ask accounting to clean it up later.

That approach creates disputes, delays revenue decisions, and muddies AR reporting. The contract needs to tell operations exactly what to bill, what to defer, what to refund, and when the engagement can be paused or terminated.

The legal distinction that changes accounting treatment

Retainers aren't all the same legally. In many jurisdictions, the rules distinguish between a true retainer, paid to secure availability, and an advanced payment retainer, which covers future services and may need to be returned if unearned. That distinction is reinforced in the San Francisco Bar Association's discussion of true and refundable retainers, including reference to In re Caesars Entertainment Operating Co. (2015).

If you're in legal services, this isn't technical trivia. It determines whether funds belong in trust, when they can be recognized as earned, and what must be refunded at the end of the engagement. Even outside law, the lesson carries over. If a payment is for future work, don't treat it as earned revenue just because cash hit the bank.

A signed engagement letter doesn't cure weak accounting. Revenue is earned by performance, not by optimism.

What the agreement has to define

Controllers need the contract to answer operational questions without interpretation.

For creative and agency work, a useful companion to retainer terms is a well-built scope document. Orsane's creative agency project scope is a good reference because it forces specificity around deliverables, boundaries, and approval assumptions that often get glossed over in retainer deals.

At minimum, the agreement should cover:

- Scope boundaries: What is included, what is excluded, and what triggers a separate fee.

- Billing cadence: Whether the charge is monthly, quarterly, or tied to balance replenishment.

- Overage handling: Whether excess work is paused, approved, or billed automatically.

- Termination mechanics: Notice period, final reconciliation, and treatment of unused funds.

- Refund logic: When unearned balances are returned.

Revenue recognition and liability discipline

Under standard revenue recognition logic, cash received before service delivery is generally a liability until the firm performs the work. That means the retainer may begin as deferred or unearned revenue, then move into revenue as obligations are satisfied.

For finance teams that need a cleaner refresher, this guide to the revenue recognition principle is useful context.

The practical control is straightforward. Separate these three events in your system:

- Cash receipt

- Work performed

- Revenue recognized

When firms collapse those steps into one journal habit, reporting becomes unreliable fast. The result is usually a month-end scramble, partner confusion, and a hard conversation with the auditor.

Operationalizing Retainers for Predictable Cash Flow

Retainer billing only improves liquidity when finance runs it as an operating system, not a contract archive.

The biggest blind spot is measurement. Firms often know total retainer revenue, but they don't know whether retainers are helping them reduce DSO, improve cash flow, and tighten forecast accuracy. That's where execution separates a disciplined model from a cosmetic one.

A useful benchmark appears in the verified industry data: professional services firms shifting from project-based invoicing to structured retainer arrangements can see DSO drops of 20–40%, yet a 2023 ACCP survey found 61% of firms still mis-track retainers in AR reports, which inflates DSO and distorts liquidity views.

Build the monthly operating cadence

Retainers work best when finance owns a recurring monthly rhythm with delivery leaders.

That cadence usually includes:

- Start-of-period billing: Invoice or collect the recurring retainer before the service window begins.

- Mid-cycle usage review: Check draw-downs, time capture, and pending overages before the balance problem becomes an end-of-month surprise.

- End-of-period reconciliation: Match work performed to retained funds, book earned revenue, and address excess or carryforward according to the agreement.

If any one of those steps is informal, AR gets noisy. The client receives mixed messages, and the retainer stops functioning as a cash-flow tool.

Track the right KPIs

Retainer programs should be judged on operating outcomes, not just topline revenue.

A finance dashboard should show at least these measures:

KPI | Why it matters |

|---|---|

DSO by client type | Tells you whether retained clients are actually paying faster |

Retainer utilization | Shows if pricing and delivery effort are aligned |

Replenishment compliance | Reveals whether balances are maintained on time |

Deferred versus earned revenue movement | Keeps reporting clean and audit-ready |

Overage recovery rate | Exposes scope creep that isn't being monetized |

In such cases, accounts receivable automation starts to matter. Once you measure retained work separately from open receivables, your DSO trend becomes more useful, and your collections team stops chasing balances that were effectively prepaid.

Operator view: Treat retained balances and unpaid invoices as different populations. If you blend them, every AR metric gets weaker.

Client-facing billing has to be explicit

Clients don't object to replenishment nearly as often as firms expect. They object to ambiguity.

A strong retainer invoice or statement should show the period covered, current retainer amount, usage against that amount, overages if any, and the remaining balance. If the agreement is based on access or deliverables rather than hours, the statement should still make consumption visible through milestones, service units, or defined outputs.

For teams using AR software for professional services, clarity at this stage is what supports consistent follow-up later.

The video below gives useful context on structuring billing operations around recurring service work.

What usually fails in practice

Three failure patterns show up repeatedly:

- Underpriced retainers that don't reflect actual delivery load.

- Late time capture that prevents accurate draw-down and replenishment.

- Finance-owned reporting with no delivery accountability, which means the team sees the problem but can't stop it.

Retainer billing is operational finance. If delivery, billing, and collections aren't aligned, the model won't hold.

Automating Retainer Management to Reduce DSO

Manual retainer management breaks in ordinary ways. A balance drops below threshold, but no one notices. Time is logged late, so the statement goes out wrong. A partner promises flexibility, and collections has to guess whether to follow up. By quarter end, the firm still has retainers on paper but not the cash control they were supposed to create.

This is why AI AR automation is becoming part of the retainer conversation. Not because the strategy changed, but because manual execution is inconsistent.

The verified industry data points to the same operational gap. A 2025 report found that 42% of professional services firms using automated retainer tracking and replenishment workflows reduced client payment delays by at least 30%, compared with 17% of firms using manual tracking.

What automation should actually do

Good automation doesn't just send reminders. It enforces the billing logic your contract already requires.

For retainer billing, that usually means:

- Monitoring balances continuously: The system should know when a draw-down crosses the replenishment threshold.

- Triggering the right message at the right time: Not every client needs the same reminder cadence or tone.

- Keeping AR and accounting in sync: The team shouldn't have to reconcile portal payments, invoices, and retainer balances by hand.

- Separating exceptions from routine work: Finance should review edge cases, not babysit every recurring top-up.

That matters whether you're using QuickBooks AR automation, a practice management platform, or a broader collections stack.

Where automation fits in the workflow

A practical retainer workflow usually looks like this:

Workflow step | Manual pain point | Automated control |

|---|---|---|

Usage posted | Delayed or incomplete updates | Balance updates immediately after usage is recorded |

Threshold reached | Trigger missed or noticed too late | Alert and top-up request generated automatically |

Client follow-up | Inconsistent reminders | Sequenced outreach through configured channels |

Payment received | Manual matching and posting | Cash application updates the account automatically |

Exception handling | Finance reacts after aging worsens | Team steps in only when the workflow flags risk |

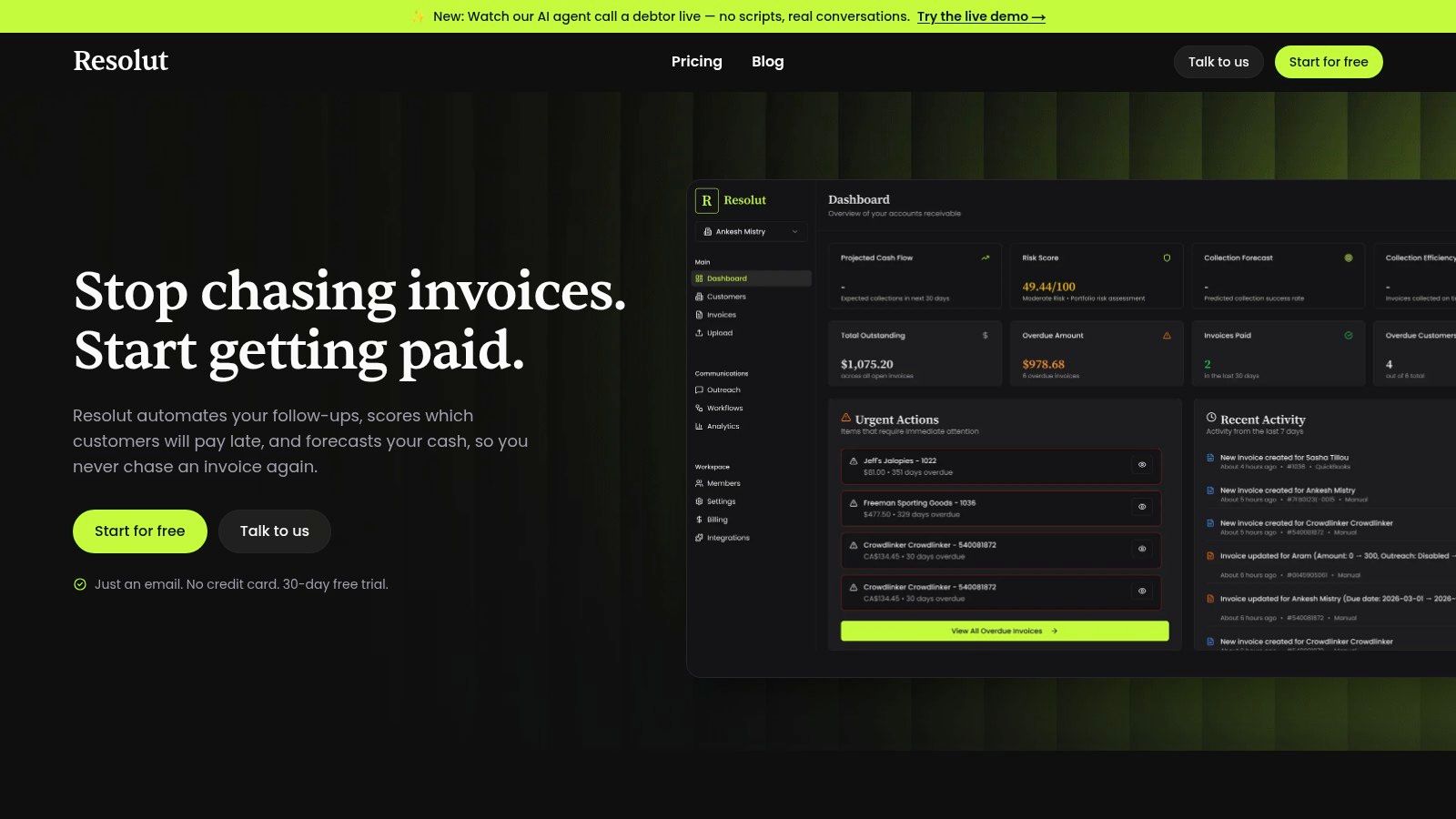

One option in this category is Resolut, which combines dynamic billing, collections orchestration, payment workflows, and automated cash application for professional services firms. In a retainer model, that kind of setup is useful because it can connect balance thresholds, outreach, payment collection, and reconciliation in one AR process.

Manual retainer management doesn't usually fail because the model is bad. It fails because no one can execute the model consistently across dozens or hundreds of clients.

The control point CFOs should insist on

The key design choice isn't “should we automate?” It's where human judgment still belongs.

Automation should handle routine threshold alerts, reminder cadence, and posting logic. Humans should still decide on exceptions such as disputed scope, temporary client accommodations, or strategic account treatment. That's the balance that protects relationships while still using accounts receivable automation to reduce DSO.

If your current process depends on someone remembering to review low balances every Friday, you don't have a retainer system. You have a person trying to hold a system together.

Resolut automates AR for professional services, including retainer-heavy workflows where firms need consistent follow-up, accurate reconciliation, and a more human approach to collections. If you're looking to improve cash flow, tighten billing discipline, or make AI AR automation practical inside an existing finance stack, Resolut is worth a look.