Sales on Credit: A CFO's Guide to Reducing DSO

Master sales on credit. Our guide for CFOs covers credit policy, risk management, and AR automation to reduce DSO and improve cash flow at your firm.

Extending terms is routine. Losing control of cash isn’t. That’s the line finance leaders have to hold.

The scale of the issue is larger than many firms admit. Over 60% of retail credit balances are held by borrowers with nonprime credit scores, and nearly 85 million U.S. adults hold retail credit accounts according to the Federal Reserve. Consumer markets aren’t the same as professional services, but the operating lesson carries over cleanly. Every time a firm invoices instead of collecting upfront, it is financing the sale.

For a professional services firm, sales on credit often feels harmless because there’s no inventory leaving a warehouse. The team did the work. The invoice went out. Revenue is booked. But cash is still delayed, and delayed cash changes how aggressively you can hire, how comfortably you can make payroll, and how much room you have when a client pays late or disputes a bill.

The firms that handle credit well don’t treat accounts receivable as a passive asset. They treat it as an operating system. Terms are defined early. Risk is assessed before work scales. Invoices are accurate. Follow-up is consistent. Exceptions are rare and visible.

That matters most in the middle market. A professional services firm between $3M and $50M can grow fast enough for weak AR habits to become a real drag, but it usually doesn’t have enough slack to absorb preventable delays forever.

Introduction The Strategic Balance of Credit Sales

Sales on credit creates a useful tension. It helps win work, smooth client buying decisions, and support larger engagements. It also pushes cash collection into the future.

That trade-off isn’t theoretical. It sits at the center of firm operations. When a consulting, legal, accounting, engineering, or agency client signs with net terms, the firm is making a financing decision alongside a sales decision.

Why this matters in professional services

In product businesses, leaders usually feel the cost of delayed cash through inventory and fulfillment. In professional services, the pressure shows up differently.

It shows up in payroll timing. It shows up in partner draws. It shows up when a project team has already delivered most of the work but the invoice is still moving through the client’s approval chain.

Revenue can look healthy while cash stays tight. That’s why sales on credit needs tighter management than many firms give it.

Practical rule: If a client needs terms, finance needs a process. Courtesy without structure turns into aging receivables.

Control beats optimism

Most firms don’t get into trouble because they offered terms once. They get into trouble because terms were granted informally, invoices went out inconsistently, and collections depended on memory.

The better approach is simple. Decide who qualifies for credit. Define the terms. Monitor behavior early. Escalate without drama.

That’s what keeps credit sales useful instead of expensive.

The Dual Nature of Sales on Credit Growth Engine and Cash Flow Risk

A sale on credit improves revenue immediately. It does not improve liquidity immediately. Those are different outcomes, and finance has to manage both.

If your firm completes a project and invoices the client, the P&L recognizes revenue. The balance sheet records accounts receivable. Cash doesn’t move until the client pays. In practice, that means a strong sales month can coexist with a stressed bank balance.

What the accounting says and what the bank account says

Take a simple project example.

Event | Accounting impact | Cash impact |

|---|---|---|

Work is delivered and invoiced | Revenue is recognized and AR increases | No cash yet |

Client pays on time | AR decreases | Cash increases |

Client pays late or disputes | Revenue may remain booked while AR ages | Cash remains delayed |

This is why accounts receivable deserves more scrutiny than many firms give it. It is an asset, but it is also a record of cash you do not yet have.

A useful way to explain this to non-finance leaders is to compare it to building a bridge before traffic arrives. The structure exists. The value may be real. But until cars cross and tolls are collected, the cash benefit hasn’t materialized.

Credit sales expand revenue and expose liquidity

Professional services firms often extend terms for reasonable commercial reasons:

- Client procurement requirements: Larger buyers often expect net terms as standard.

- Competitive positioning: A flexible billing arrangement can help close a deal.

- Relationship management: Longstanding clients may get more latitude.

- Project economics: Milestone billing can align with delivery better than full prepayment.

None of that is wrong. The problem starts when commercial flexibility outpaces cash discipline.

Historical evidence shows how exposed credit sales can become when conditions tighten. In the 1954 U.S. recession, total sales volume fell by $15.2 billion while bank credit contracted by $300 million, illustrating how closely credit sales and liquidity move with broader economic stress, as noted in the Oxford Research Encyclopedia of American History.

That lesson still holds. If your clients feel pressure, approvals slow, disputes increase, and payment behavior changes. Firms that treated receivables as “money in the bank” usually find out too late that it wasn’t.

The operating view that works

Good finance teams look at sales on credit through three lenses at once:

- Revenue quality Is the sale collectible under normal conditions?

- Timing risk How long will cash realistically take to arrive?

- Concentration risk What happens if one large client pays late?

A growing AR balance can mean growth. It can also mean your firm is becoming your clients’ lender.

That’s why credit sales should never sit only inside accounting. It belongs in the operating cadence of finance, sales leadership, and delivery management.

Building a Resilient Credit Policy for Your Firm

A credit policy should remove ambiguity before the first invoice goes out. If your team is debating exceptions client by client, you don’t have a policy. You have a habit of negotiating after risk has already entered the business.

A strong policy doesn’t need to be long. It needs to be clear, enforced, and tied to how your firm sells.

The core decisions your policy must settle

Most professional services firms need written answers to a small set of questions:

- Who can approve terms: Sales shouldn’t grant payment terms on its own if finance carries the collection risk.

- Which clients qualify: New clients, small engagements, and expansion work may need different treatment.

- What documents are required: Signed engagement letter, billing contact, legal entity name, purchase order rules, and dispute protocol.

- How credit limits are set: Even service firms need exposure limits by client.

- When work pauses: This is one of the most important controls and one of the least documented.

A practical policy should also define what happens when a client requests something outside standard terms. If exceptions are allowed, name the approver and the reasoning required.

Terms are leverage, not boilerplate

Many firms copy “net 30” into every contract because it’s familiar. That isn’t strategy. It’s default behavior.

Credit terms should match the client, the size of the engagement, and the firm’s appetite for delay. Sometimes a retainer is the right answer. Sometimes milestone billing is safer than monthly arrears. Sometimes a client with uneven payment behavior needs shorter cycles and tighter approval checkpoints.

Early payment incentives can work well when used selectively. Standard terms such as 2/10, net 30 mean payment is due in 30 days, but the buyer gets a 2% discount for paying within 10 days. The implied annualized cost of skipping that discount is over 36%, and this structure has been shown to accelerate cash inflows by 20 to 30 days on average, according to Corporate Finance Institute’s explanation of credit sales terms.

For finance leaders, the point isn’t to offer discounts everywhere. It’s to understand that terms shape behavior. A term on paper is an economic signal.

If you’re revisiting your own structure, this guide on payment terms and condition is a useful reference point for tightening language and aligning terms with collection realities.

A policy format that works in practice

Here’s a straightforward structure that’s workable for most firms:

Policy area | What to define |

|---|---|

Client onboarding | Required legal, billing, and approval information |

Credit approval | Who approves terms and exposure |

Billing rules | Invoice timing, required backup, PO handling |

Payment terms | Standard terms and allowed exceptions |

Collections triggers | Reminder timing, escalation thresholds, work stoppage rules |

Dispute handling | Who owns resolution and billing correction steps |

Where policies usually fail

They rarely fail because the firm chose the wrong template. They fail because nobody follows them when a large client pushes back.

Watch for these weak points:

- Sales-led exceptions: Revenue pressure can override sensible controls.

- Late invoicing: Good terms mean little if invoices go out late.

- Missing client setup data: Wrong entity names and unclear approval contacts slow payment before collections even starts.

- No consequence for delinquency: If work continues unchanged regardless of aging, the client learns your terms are optional.

The best credit policy is the one your team can apply on a busy Tuesday without a meeting.

Assessing and Managing Customer Credit Risk

Credit policy gives you the rules. Risk assessment applies them to real clients.

That matters because not every customer deserves the same terms, and not every profitable client is low risk. In professional services, the danger often isn’t obvious at the outset. A client may have budget, urgency, and a well-known brand, yet still have slow approval cycles or weak internal billing discipline.

Traditional signals still matter

A clean risk review usually starts with standard inputs:

- Trade references: Useful if you verify them.

- Basic financial information: Especially for privately held clients on larger engagements.

- Payment history with your firm: Usually the strongest signal if it exists.

- Contract structure: Fixed-fee, recurring, milestone-based, and change-order-heavy work carry different risks.

- Buyer process clarity: If nobody can tell you who approves invoices, expect friction later.

For many firms, payment behavior matters more than polished paperwork. A client that consistently pays smaller invoices late will often do the same on larger ones.

Why traditional credit files are often incomplete

A common problem in professional services is the small or newer client that lacks an established credit history but may still be a good payer. That’s where old methods can become too blunt.

Over 45 million U.S. consumers are credit unserved or underserved, including 32 million adults who are unscoreable, according to TransUnion’s newsroom data. The consumer statistic isn’t a direct B2B credit measure, but it mirrors the same issue finance teams see with thin-file small businesses. Traditional scoring often misses viable buyers.

Alternative data helps fill the gap. In a B2B context, that can include transaction consistency, deposit behavior, cash flow patterns, and operational history. The point is not to lower standards. It’s to assess risk with more context.

A client can be unscored without being uncreditworthy. Finance needs a method for telling the difference.

A simple risk matrix for professional services

You don’t need a complex model to improve decisions. A practical matrix is often enough.

Risk tier | Typical profile | Terms approach | Monitoring approach |

|---|---|---|---|

Low | Strong history, clear billing process, predictable engagement | Standard terms | Routine review |

Medium | Limited history, some approval complexity, moderate invoice size | Tighter limits or milestone billing | More frequent aging review |

High | Past delinquencies, unclear approver path, dispute-prone work | Retainer, partial prepay, or short billing cycle | Active oversight |

The value is consistency. Once clients are assigned a risk tier, the team can align terms, billing cadence, and escalation.

A useful primer on the underlying concepts sits below.

What finance should revisit during the engagement

Risk isn’t fixed at onboarding. It changes when scope expands, when the client changes controllers, or when invoices begin to age.

Reassess when you see any of these:

- Invoice approvals slowing down

- Repeated short-pays or deductions

- Rapid increase in monthly billings

- Turnover at the client’s finance team

- More disputes tied to vague statements of work

That review discipline is what keeps sales on credit from turning into unmanaged exposure.

From Invoice to Cash Optimizing the Collections Cycle

Most collection problems start before collections.

They start with a vague statement of work, a delayed invoice, the wrong legal entity, missing backup, or a billing format the client’s AP team can’t process. By the time the invoice is “late,” the actual issue may be administrative, not financial.

That’s why effective collections begins with invoice quality.

Clean invoices reduce avoidable delay

For professional services firms, the invoice has to answer the client’s likely questions before they ask them.

A good invoice package usually includes:

- Correct billing entity: The legal name has to match the contract and the client’s vendor record.

- Clear service period: Ambiguity invites review delays.

- Relevant backup: Time detail, milestone reference, approved change orders, or PO information.

- Payment instructions: Make it easy to pay without follow-up.

- Named contact for disputes: Don’t route everything through the partner by default.

If your collections team spends time explaining basic invoice details after every send, the issue is upstream.

Collections should run on cadence, not mood

Ad hoc follow-up doesn’t scale. It also creates uneven client experience. One account gets multiple reminders because a collector knows the contact personally. Another gets silence because nobody noticed the due date passed.

A better model is a structured dunning process with defined stages and message tone. In plain terms, that means a repeatable reminder sequence tied to due dates, aging, and account risk.

One workable cadence looks like this:

- Pre-due reminder Short, polite, factual. Confirm receipt and surface any issue early.

- Due-date notice Professional and neutral. Include invoice, amount due, and payment options.

- Early past-due follow-up More direct. Request payment date and identify any approval blocker.

- Escalation notice Involve the account owner or finance lead if there’s no response.

- Final internal escalation Decide whether work pauses, leadership calls, or formal recovery steps apply.

This protects the relationship better than irregular chasing. Clients respond better to consistency than to sudden bursts of pressure after weeks of silence.

Good collections feels orderly to the client. They know what’s due, when it’s due, and what happens if it slips.

Preserve the relationship without softening the control

A common mistake in professional services is assuming that firm follow-up will damage a client relationship. Usually the opposite is true. Clear expectations reduce friction.

Collections gets harder when teams mix roles poorly. Partners want to protect the relationship, so they delay hard conversations. Finance wants payment, but may not have enough context to address a dispute. Delivery teams know the account best, but often aren’t looped in until late.

The fix is role clarity:

Stage | Primary owner | Support role |

|---|---|---|

Invoice issue | Billing or finance | Delivery lead |

Routine reminder | AR team | None unless issue emerges |

Delinquency discussion | Finance lead | Account owner |

Commercial dispute | Account owner | Finance for documentation |

Work stoppage decision | CFO or firm owner | Sales and delivery leadership |

For firms looking to operationalize this, guidance on how to automate accounts receivable can help translate a manual reminder habit into a controlled workflow.

What doesn’t work

Several habits reliably weaken collections:

- Waiting too long to follow up: Silence teaches clients that your due dates are flexible.

- Sending generic reminders with no context: Useful for volume, weak for resolution.

- Letting unresolved disputes sit in aging: Disputed invoices need ownership, not passive reporting.

- Allowing new work while old balances drift: That raises exposure without increasing control.

The firms with better cash conversion don’t necessarily sound tougher. They behave more predictably.

Key Metrics to Master for Healthier Cash Flow

If you can’t measure receivables well, you’ll end up managing by anecdote.

One partner says collections are fine. Another says a major client is “always slow.” The controller sees aging drift. The owner sees revenue growth and assumes cash will catch up. Metrics settle those arguments quickly.

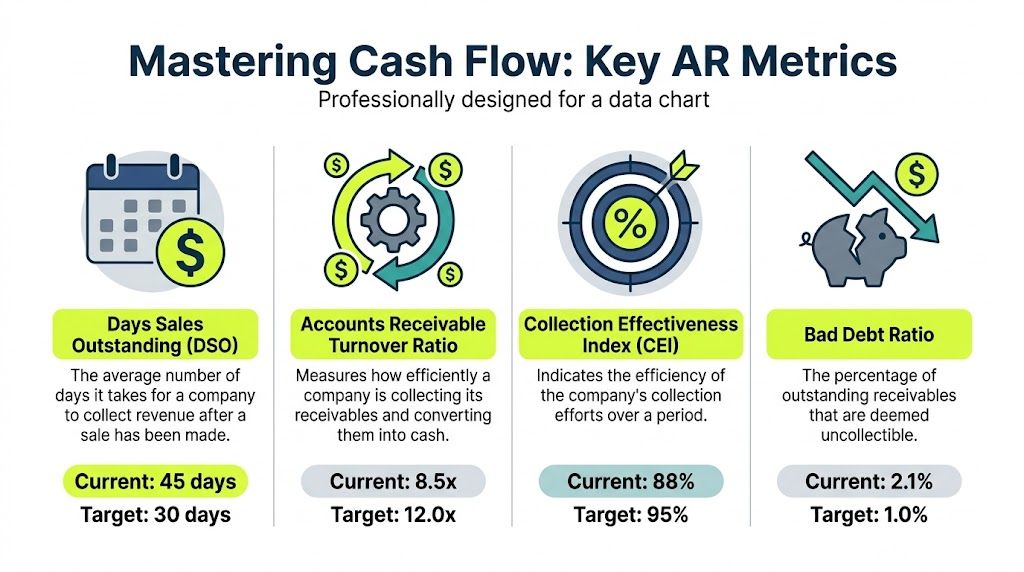

Start with DSO

Days Sales Outstanding, or DSO, tells you how many days it takes on average to collect revenue after a sale is made. For firms that sell on credit, it is one of the clearest indicators of how fast booked revenue turns into usable cash.

The formula is straightforward:

DSO = (Accounts Receivable / Credit Sales) × Number of Days

The number alone isn’t enough. You need trend and context. A rising DSO may signal slower client payment, weaker invoice quality, loose credit discipline, or a shift in customer mix.

For a practical walkthrough, this explanation of what is dso is useful if you want to align the formula with day-to-day finance operations.

Pair DSO with collection quality metrics

DSO is important, but it can hide detail. That’s why I prefer to track it alongside a small set of supporting indicators.

A simple dashboard should include:

- Accounts receivable turnover ratio: How efficiently receivables convert into cash over time.

- Collection Effectiveness Index: Whether the team is collecting what was collectible in the period.

- Aging by bucket: Especially current, slightly past due, and materially delinquent balances.

- Bad debt ratio: A reality check on credit quality, not just collection speed.

The infographic above shows a sample target structure. Use it as a visual management tool, not just a board slide.

If your team is building reporting discipline more broadly, this guide to understanding key performance indicators is a good companion for deciding which measures are worth management attention.

How to read the metrics like an operator

Metrics matter less as isolated figures and more as patterns.

Metric movement | Likely interpretation | Management response |

|---|---|---|

DSO rising | Cash conversion slowing | Review terms, invoice timing, and dispute volume |

CEI weakening | Collections process losing consistency | Audit follow-up cadence and accountability |

Aging worsening in one segment | Concentrated client or industry issue | Tighten terms and review exposure |

Bad debt increasing | Underwriting or escalation is weak | Revisit client qualification and reserve approach |

Many firms achieve quick improvement here. Not because they discovered a new formula, but because they started linking each metric to an action.

When DSO moves, treat it like a symptom. Ask what changed operationally, not just what changed mathematically.

Don’t overbuild the scorecard

You don’t need a sprawling finance dashboard to improve cash flow. You need a scorecard that someone reviews regularly and uses to make decisions.

For most professional services firms, that means:

- a receivables aging report that’s current,

- one owner for collection review,

- a short list of accounts needing intervention,

- and trend lines management can understand without translation.

The firms that improve cash flow usually get disciplined before they get advanced.

The Role of AR Automation in Modern Credit Sales

Manual AR management breaks in predictable ways. Follow-ups depend on individual memory. Billing data sits in separate systems. Risk signals appear late. Cash application lags because remittance details are messy. None of this is dramatic on its own, but together it slows collection and weakens control.

That’s why accounts receivable automation matters. Not as a buzzword, but as operating infrastructure.

What automation should actually do

A modern AR stack should support the full credit-to-cash cycle.

That includes:

- Policy enforcement: Terms, approval paths, and escalation logic should not live only in someone’s head.

- Risk visibility: The team needs earlier signals on which invoices or clients deserve attention.

- Collections orchestration: Communication should run on schedule across channels without becoming robotic.

- Payment convenience: Clients should have simple, professional ways to settle invoices.

- Cash application: Reconciliation should happen quickly enough for reporting and follow-up to stay accurate.

When these functions stay manual, firms usually compensate with labor. More spreadsheets. More calendar reminders. More internal chasing.

Where AI AR automation changes the game

The most useful shift in the last year has been the application of AI to collections timing, message selection, and risk prioritization.

Recent AI advances now support dynamic, omnichannel collections for at-risk invoices, combining risk flagging, personalized outreach across email, SMS, and phone, and fast cash application. These tools are being used against a real global problem where 1 in 10 B2B invoices go unpaid, creating over $200B annually in administrative waste and bad debt, as described in this overview of the financially underserved market and collections technology.

For a finance operator, the important point isn’t the label. It’s the workflow improvement.

A solid AI AR automation system can help answer practical questions such as:

- Which invoices are most likely to slip if no one acts today?

- Which clients respond better to a reminder before the due date versus after?

- When should a message come from AR, and when should it come from an account lead?

- Which balances are stuck because of a dispute signal rather than inability to pay?

That changes collections from broad effort to directed effort.

Why this matters for professional services firms

Professional services firms often have a harder collections environment than product companies. Invoice amounts can vary widely. Billing support may be detailed. Payment approval can involve project leads, procurement, and AP. Relationship sensitivity is high.

Automation helps by making the process more consistent without making it more impersonal.

A well-designed system supports:

Need | Manual approach | Automated approach |

|---|---|---|

Reminder timing | Calendar-based and inconsistent | Triggered by due date, behavior, and risk |

Client communication | Email drafted ad hoc | Standardized but adaptable outreach |

Visibility | Aging reviewed after the fact | Alerts on at-risk accounts earlier |

Payment handling | Separate links and manual posting | Integrated payment flow and faster application |

That is how firms reduce DSO and improve cash flow without turning collections into a blunt instrument.

QuickBooks AR automation and system integration

Many middle-market firms already run core accounting in QuickBooks. The challenge is that QuickBooks records AR well enough, but it doesn’t, by itself, create a disciplined collections engine.

That’s where QuickBooks AR automation becomes useful. When AR tools integrate directly with the accounting ledger, finance gets a cleaner operating loop:

- invoices sync without manual re-entry,

- reminder status reflects current balances,

- payment activity updates faster,

- and collections reporting is tied to real ledger data.

The result is not just less admin work. It’s fewer mismatches between what the AR team says, what the client sees, and what the books show.

What good automation does not replace

Automation should not remove judgment. It should remove avoidable manual work and surface the moments where judgment matters most.

Finance still needs to decide:

- when a client deserves an exception,

- when a dispute is commercial rather than administrative,

- when to pause work,

- and when a relationship needs executive involvement.

The strongest AR software for professional services doesn’t pretend to run the business alone. It gives the CFO, controller, and collections team tighter timing, better visibility, and more consistent execution.

That’s the core value of automation in sales on credit. It makes control repeatable.

Conclusion Achieving Controlled Growth Through Smarter Credit

Sales on credit is not a bookkeeping detail. It’s a strategic choice about how your firm grows and how much cash risk it is willing to carry.

For professional services firms, the answer usually isn’t to stop offering terms. It’s to stop offering them casually.

A disciplined approach has a few clear parts. Set a credit policy that people follow. Assess client risk with more than instinct. Invoice cleanly and on time. Run collections on a consistent cadence. Measure the output with a small set of AR metrics that management reviews regularly.

Technology strengthens each of those steps when it’s applied well. It helps enforce terms, focus attention on the right accounts, support client-friendly payment options, and reduce the manual friction that slows collections.

That’s how firms create room to grow without letting receivables dictate the pace of the business.

Credit can help win work. Control is what lets you keep the cash.

Resolut automates AR for professional services with a practical focus on consistency, accuracy, and human judgment. If you’re looking to tighten collections, reduce DSO, and improve cash flow without making client interactions feel mechanical, Resolut is worth a look.