Sample Letter to Debt Collector: 8 Expert Templates

Sample letter to debt collector - Find the perfect sample letter to debt collector. Access 8 CFO-approved templates for debt validation, settlement, and

Stop Chasing Payments. Start Orchestrating Them.

For every ten invoices your firm sends, one may go unpaid without significant effort. This drain on resources, part of a multi-billion dollar problem for businesses, isn't a cost of doing business. It's a process failure. Effective accounts receivable is about clear, systematic communication, not aggression.

That matters even when the search term is consumer-oriented. A strong sample letter to debt collector is really a control document. It defines what's being requested, what gets documented, when the clock starts, and how the account should move through dispute, validation, payment, or escalation. For finance leaders, that's the difference between scattered follow-up and a repeatable collections process that can reduce DSO and improve cash flow.

Consumer law is a useful model here. Under FDCPA Section 809(b), if a consumer disputes a debt in writing within 30 days of receiving a collector's notice, the collector must stop collection until it mails verification of the debt. That's operationally important because it reveals the power of timing, documentation, and sequence.

Professional services firms can borrow that discipline. Whether you're running accounts receivable automation, evaluating AI AR automation, or tightening QuickBooks AR automation workflows, your letters should trigger actions, not just sit in a file. If you already use automated outreach in other parts of the business, the same orchestration mindset applies to collections. Teams that boost sales with automated outreach usually recognize the pattern quickly.

1. Initial Debt Collection Notice Letter

The first letter sets the tone for the entire file.

If it's vague, emotional, or missing core invoice details, your team will spend the next few weeks fixing preventable errors. If it's clear, dated, and easy to act on, many balances resolve without a second round. In professional services, that matters because the same client who's late today may still be a strategic account next quarter.

I prefer an initial notice that reads like a finance document, not a threat. It should identify the customer, invoice number, service period, due date, amount due, payment methods, and a firm response date. If you're using a modern dunning letter workflow, this is the message that begins the paper trail.

What belongs in the first notice

A good sample letter to debt collector style notice should remove ambiguity:

- State the exact obligation: Name each overdue invoice and the related matter, project, or retainer.

- Give one path to resolution: Include payment instructions and a contact for billing disputes.

- Preserve relationship tone: Keep the language professional, especially for clients with ongoing work.

- Set a next step: If payment won't be made immediately, ask for a confirmed payment date.

This is also where finance teams often overcomplicate things. They add legal phrasing too early, stack multiple threats into one letter, or bury the call to action under policy language. That usually slows payment, not speeds it up.

Practical rule: Your first notice should make payment easier than ignoring you.

For firms using AR software for professional services, this template works best when tied to workflow rules. Day-based triggers, invoice-level detail, and payment links all reduce back-and-forth. If your team is still manually exporting aging data from QuickBooks and drafting one-off emails, this is usually the first place to automate.

A visual worth adding here is a simple timeline graphic: invoice issued, due date missed, first notice sent, customer response, payment posted. CFOs don't need more theory. They need to see the process.

2. Overdue Account Statement Letter

One overdue invoice is a reminder problem. Multiple overdue invoices are a reporting problem.

When a client has several open balances, scattered reminders create noise. The customer disputes one line, ignores two others, and asks your team for a consolidated statement anyway. Sending that statement earlier tightens control and limits excuses.

This template should work like a mini account reconciliation. It should show all open invoices, aging status, credits if any, and the current total due. The most useful versions also point out which items are oldest and require immediate action.

Why this letter matters operationally

In debt collection practice, collectors must send a validation notice within 5 days of first contacting a consumer, and well-built templates commonly request itemized details such as balance at placement, added interest or fees, delinquency date, and last payment date. That structure is worth copying in B2B AR because itemization prevents arguments later.

For a law firm, agency, or consulting firm, the equivalent is straightforward:

- List by invoice date: Oldest balances first.

- Show aging bands clearly: Separate current, late, and seriously past due items.

- Tie entries to work performed: Matter names, projects, or monthly service periods help clients reconcile internally.

- Call out disputed items distinctly: Don't bury them among collectible balances.

A statement letter is where accuracy matters more than tone. If your statement is wrong, every later reminder loses credibility. If your cash application is sloppy, you'll train customers to delay while they “check with AP.”

Send the account statement only after reconciling unapplied cash, credits, and recent remittances. Otherwise you're asking the client to do your internal cleanup.

This is one place where accounts receivable automation earns its keep. A system that pulls invoice detail cleanly, applies payments correctly, and assembles a usable statement reduces friction for both sides. For firms pursuing reduce DSO goals, that's often more valuable than writing tougher emails.

A good visual here is a clean aging waterfall by client, with color bands showing where balances have accumulated over time.

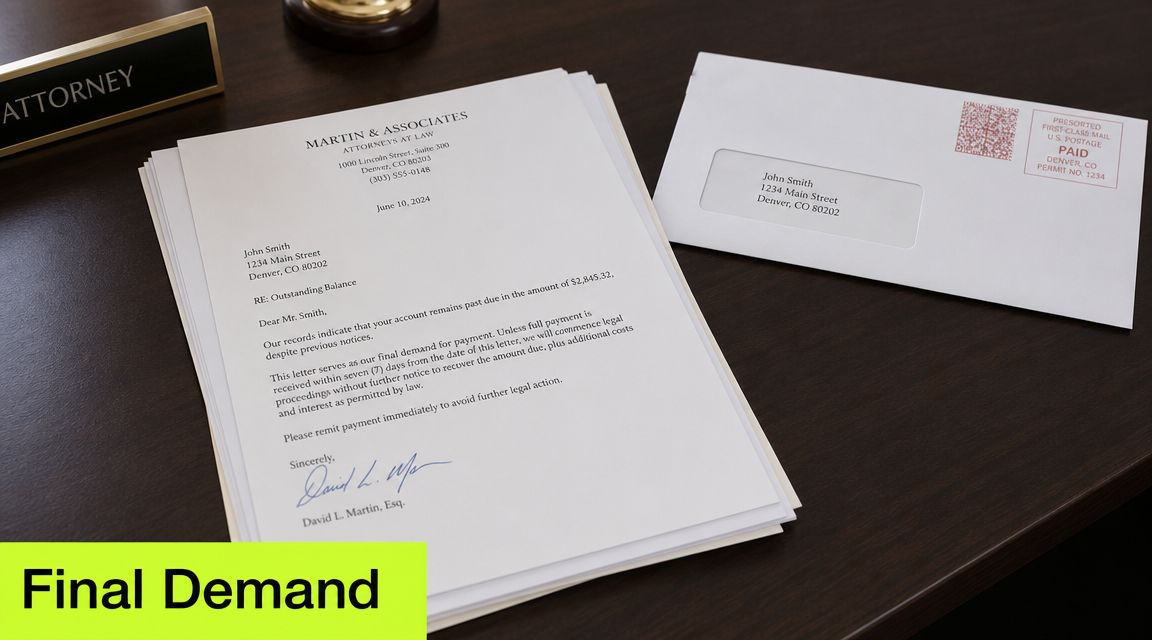

3. Demand Letter from Legal Counsel

Some balances won't move until the tone changes.

That doesn't mean jumping to legal posture at the first missed invoice. It means recognizing when standard follow-up has run its course and when a lawyer-signed demand, or a carefully structured legal-style escalation, is the right next move. In my experience, timing matters more than theatrics.

This letter should be reserved for files where you've already documented invoice delivery, reminders, account statements, and at least one direct attempt to resolve the matter commercially. If you escalate too early, you increase legal noise on accounts that may still pay. If you escalate too late, you normalize delay.

What legal escalation should do

A proper demand letter should narrow the debtor's choices:

- Pay in full by a stated date

- Propose a documented payment arrangement

- Raise a specific dispute with supporting grounds

It should also avoid amateur legal drafting. Unsupported threats, inflated balances, and vague references to “further action” make the sender look unserious. If you need language benchmarks, use a legal demand letter for payment framework and have counsel review anything that could trigger state-specific issues.

Ballard Spahr's consumer template highlights another smart operational point. It instructs recipients to preserve a copy, request cessation of contact, and require the collector to report the debt as disputed if forwarded or reported to a bureau, which helps create a downstream paper trail for account handling in the underlying template packet.

That same discipline applies in B2B collections. Every legal-stage letter should be logged, version-controlled, and tied to a decision rule. If the account pays, close it cleanly. If the client disputes, route it. If nothing happens, move to the next approved step.

The value of a legal letter isn't the language. It's the clarity it creates around consequences and documentation.

4. Payment Arrangement Proposal Letter

Some clients can't pay in full today, but they can still become collectible accounts.

Finance teams that treat every late balance as binary, pay now or go legal, usually leave money on the table. A structured arrangement letter gives you another option. It protects cash flow while preserving client relationships that may still matter commercially.

The strongest arrangement letters are specific. They don't say, “Let us know what works.” They present terms. Installment amount, due dates, payment method, default language, and who must approve it. That turns a soft conversation into an enforceable process.

Structure the plan before you send it

The letter should answer four questions fast:

- What is being resolved: Identify the invoices or total balance included.

- How it will be paid: Spell out installment timing and payment method.

- What happens if a payment is missed: Define default and re-escalation.

- What the customer must do to accept: Signed return, portal acceptance, or written confirmation.

That's where a payment plan agreement template becomes useful. It gives your team a standard starting point so arrangements don't vary wildly by collector, account manager, or partner.

This is also one of the clearest use cases for AI AR automation. A system can identify clients who repeatedly miss standard due dates but still pay under structure, then route them toward installment offers instead of generic pressure. That's better for forecast accuracy and usually better for client retention.

Use caution with concessions. If you offer reductions or waived charges too early, clients learn to wait for discounts. If you never offer flexibility, some collectible balances turn into write-offs. The right answer depends on account history, strategic value, and documentation quality.

A useful visual here would be a side-by-side flow: full-balance demand on one side, payment arrangement path on the other, each ending with either payment, default, or escalation.

5. Debt Validation Request Response Letter

Weak recordkeeping gets exposed.

If a customer, consumer, or their representative asks you to validate a debt, your response can't be improvised. You need the support file. Contract or engagement terms, invoice history, credits, payments, and the calculation behind the current balance. If any piece is missing, the account may still be collectible, but your bargaining power lessens.

Under FDCPA practice guidance, consumers should request verification within 30 days of receiving validation information, and a valid request should stop a collector from proceeding without first providing the required details. The guidance also stresses that the request should ask for the amount of the debt, the current creditor, and supporting documentation.

What a solid validation response looks like

In operational terms, your response packet should include:

- A concise cover letter: State what is enclosed and what balance it supports.

- Underlying documents: Engagement agreement, invoice copies, statement history, and payment ledger.

- Balance calculation: Show how the current amount was derived.

- Ownership clarity: Identify the current creditor or collecting entity.

If you manage a professional services portfolio, document discipline directly affects cash flow. A partner may remember the work. That doesn't help if the signed engagement letter is buried in email or if invoice revisions weren't versioned properly.

CFPB sample letters also make an important point many teams miss. Even when someone says their income is protected from garnishment, collectors may still legally communicate, ask for payment, offer a plan, or attempt settlement, as the agency notes in its sample debt collector letter language. In other words, a validation request changes workflow. It doesn't erase the need for one.

If your team can't assemble a validation packet quickly, you don't just have a collections problem. You have a records problem.

For firms using QuickBooks AR automation, the lesson is simple. Accounting entries alone aren't enough. The system has to connect ledger data with customer-facing documents.

6. Settlement and Release Letter

Settlement letters are useful when the balance is real, the file is supportable, and full recovery is unlikely on a reasonable timeline.

That often happens with former clients, strained relationships, terminated projects, or matters where both sides want finality more than they want a prolonged fight. A good settlement letter trades some amount of value for speed, certainty, and closure.

This is not a casual email. It should be drafted as a controlled offer with acceptance terms, payment mechanics, and release language that your legal team is comfortable enforcing. If the account later resurfaces in a dispute, sloppiness here becomes expensive.

When settlement makes sense

I'd consider settlement when one or more of these are true:

- The account is aging badly: The probability of full, fast recovery is declining.

- Legal cost will outrun incremental recovery: You need net cash, not symbolic victory.

- The client relationship is already broken: Preserving goodwill is no longer the main objective.

- Documentation is adequate but not ideal: A negotiated outcome may beat a contested one.

This is also where many teams make a basic mistake. They negotiate by phone, accept partial payment, and never document whether the payment was in full settlement or just a partial remittance. That ambiguity creates downstream accounting and legal risk.

For a CFO, the right frame is portfolio economics. Some accounts deserve continued pursuit. Others should be settled, closed, and removed from forecast distortion. That isn't softness. It's capital discipline.

A settlement and release letter should also coordinate with accounting treatment. Once accepted, your team should know exactly when to mark the remaining balance adjusted, written off, or fully resolved. AR software for professional services helps here if it can track agreement status and payment completion against the customer ledger.

7. Cease and Desist Letter for Disputing Debtor

This is the most dangerous template on the list, and most firms should use it rarely.

When a debtor makes false accusations, threatens baseless counterclaims, or tries to derail collection with disruptive conduct, the instinct is to push back hard. Sometimes that's appropriate. Often it isn't. The wrong letter can escalate conflict, undermine your position, or create compliance risk.

The first question isn't what you want to say. It's whether sending anything helps recover the balance. If the debtor's behavior is merely irritating, silence and documentation may be better than a reactive letter. If the conduct is clearly harmful and documented, counsel should decide whether a cease-and-desist style response is warranted.

Keep the demand narrow

If this letter is sent at all, it should:

- Identify specific conduct: False statements, harassment, or interference should be described precisely.

- Avoid broad threats: Don't promise action your firm won't take.

- Preserve the collection objective: The file still needs a path to resolution.

- Route through counsel: This isn't a standard collections email.

Consumer guidance consistently distinguishes among validation requests, ownership disputes, and requests to stop contact. The problem with many templates is that they blur these legal actions together, as discussed in this validation request letter guidance. That same confusion shows up in business collections when teams mix rebuttal, demand, and contact restrictions in one message.

If you're dealing with a consumer-facing matter or a sensitive debtor situation, it's also worth understanding broader debt relief and dispute context, including practical legal considerations discussed in BDJ Express Law's debt relief guide.

Narrow letters are safer letters. Ask for less, say only what you can support, and leave room for counsel to act later.

8. Internal Collections Follow-up Letter

Most recovery work doesn't happen in the dramatic moments. It happens in the middle.

That's the part many firms still run manually. Someone exports aging, sends a reminder, sets a calendar note, forgets to follow up after a promised payment date, then starts over a week later. If you want to reduce DSO, at this point your process either holds or breaks.

An internal follow-up letter isn't meant for legal escalation. It's the operating rhythm between invoice due date and formal demand. The best versions are short, consistent, and sequenced. They assume the client may be busy, but they also tighten language as the account ages.

Here's a useful reference point for format and pacing:

Build the sequence, then automate it

A practical sequence usually includes:

- Early reminder: Confirm the invoice is outstanding and provide a payment path.

- Mid-stage follow-up: Reference prior outreach and ask for a firm payment date.

- Late-stage notice: Advise that the account is moving toward escalation or hold.

- Exception handling: Route disputes, short-payments, and broken promises differently.

Here, accounts receivable automation and AI AR automation can do real work. Not by writing clever copy, but by enforcing timing, preserving tone rules, and adapting channel choice across email, SMS, and phone. For finance leaders, that's the operational core of improve cash flow efforts.

Consumer templates are useful here because they force clarity about outcomes. Some letters are meant to dispute. Some request validation. Some seek cessation of contact. Some are designed for wrong-party or identity-theft situations, as reflected in IdentityTheft.gov and related consumer templates discussed through the Ballard Spahr materials noted earlier. In AR operations, your equivalent discipline is deciding whether each follow-up is asking for payment, backup, confirmation, or settlement.

If every reminder says everything, none of them works very well.

8-Sample Debt Collection Letters Comparison

Template | 🔄 Implementation Complexity | ⚡ Resource Requirements | 📊 Expected Outcomes (⭐) | 💡 Ideal Use Cases | Key Advantages / Tips |

|---|---|---|---|---|---|

Initial Debt Collection Notice Letter | Low–Moderate, standard template and tone | Low, automated AR systems, basic staff time | ⭐ Moderate, ~30–50% immediate response when sent at day 30 | Early-stage collections; routine past-due invoices | Preserve relationships; include direct payment link; use email+SMS for higher engagement |

Overdue Account Statement Letter | Moderate, requires accurate itemization and aging | Medium, accounting integration and PDF generation | ⭐ Good, clearer debt picture; 45–55% recovery on multi-invoice accounts | Accounts with multiple invoices or long payment history; CFO/controllers | Format clear aging buckets; attach PDF; offer settlement/prioritization guidance |

Demand Letter from Legal Counsel | High, legal drafting and compliance review required | High, attorney fees, certified delivery | ⭐ High, 50–65% response pre-litigation; strong legal foundation | Final escalation before litigation; chronic non-payers | Use after documented attempts; ensure FDCPA/state compliance; consider certified mail |

Payment Arrangement Proposal Letter | Moderate, customized terms and monitoring needed | Medium, billing system support, payment processing | ⭐ Very High for preserved accounts, 60–75% recovery via arrangements | Debtors in financial distress where relationship preservation is priority | Offer 2–3 plan options, require written acceptance, enable automatic payments |

Debt Validation Request Response Letter | Moderate–High, compile contracts, invoices, payment history | Medium–High, document retrieval, certified delivery recommended | ⭐ High (compliance-critical), protects against FDCPA claims; can increase payments | When debtor requests validation under FDCPA Section 809 | Respond promptly (ideally ≤15 days); send copies of docs; keep delivery proof |

Settlement and Release Letter | High, requires precise legal language and accounting treatment | Medium–High, legal review and settlement processing | ⭐ High for recovery speed, 50–80% recovery common; faster than litigation | High-balance accounts unlikely to pay in full; desire to close accounts | Require signed release, set clear deadline, use payment portal for frictionless payment |

Cease and Desist Letter for Disputing Debtor | High, high legal risk if misdrafted | High, legal counsel strongly recommended | ⭐ Mixed, effective if justified but risky (possible FDCPA exposure) | Cases of demonstrable false claims, threats, or harassment | Use rarely; require counsel review; be specific and document misconduct; send certified mail |

Internal Collections Follow-up Letter | Low, templated sequence, easily automated | Low, automation platform; minimal manual effort | ⭐ Moderate, 20–35% on first contact; improves with progressive touches | High-volume routine follow-ups (Day 30/50/70/90 sequences) | Automate sequences, vary tone by stage, include direct payment link and omnichannel follow-up |

From Templates to Automation: A System for AR Control

These templates are useful because they create consistency. They help your team say the right thing, at the right point in the account lifecycle, with a record that can support audit, dispute handling, and escalation. That alone is an improvement over ad hoc collection emails drafted in the moment.

But templates aren't enough.

Advantage comes from turning each letter into a controlled workflow step. Initial notice. Consolidated statement. Payment arrangement. Validation response. Legal escalation. Internal follow-up. Each one should have a trigger, an owner, a service-level expectation, and a documented next action. That's how finance teams move from reactive collections to predictable AR control.

For professional services firms, this matters more than it does in many product businesses. Your invoices often reflect partial periods, retainer replenishments, pass-through costs, staged projects, or partner-managed exceptions. That complexity makes manual follow-up fragile. One missed credit, one misapplied payment, or one poorly timed escalation can slow payment and damage a client relationship at the same time.

Good systems solve for both discipline and flexibility. They standardize communication without flattening judgment. They let routine reminders run automatically while routing disputed, strategic, or legally sensitive accounts for review. They preserve the paper trail. They surface accounts that need action before they become write-offs. And they help finance leaders tie communication quality back to the outcomes that matter, including reduce DSO, improve cash flow, cleaner forecasting, and fewer hours lost to manual chasing.

That's also the right way to think about a sample letter to debt collector in a B2B context. It isn't just a form. It's a decision point in a broader receivables process. If the letter asks the wrong thing, goes out at the wrong time, or lands without supporting data, the process breaks. If it's integrated into accounts receivable automation, the letter becomes an instruction that moves the account forward.

One visual I'd add to the conclusion is a dashboard view: open AR by aging band, disputes in validation, active payment plans, and accounts pending escalation. Another is a cinematic operations image of a controller reviewing a morning exception queue with only a handful of accounts needing manual intervention. That's what mature AR should feel like. Quiet, controlled, and measurable.

If you're evaluating systems, keep the standard simple. Can the platform help your team send the right message consistently, maintain documentation quality, coordinate channels, and support human review where needed? If it can, it has a place in the stack. Resolut is one option built around that model for professional services. Resolut automates AR for professional services, consistent, accurate, and human. It also pairs well with adjacent workflow thinking, including efforts to automate PDFs using OkraPDF and Zapier.

If you want more control over collections without adding more manual work, Resolut is worth a look. It helps professional services firms orchestrate outreach, payment options, escalation, and cash application in one AR workflow so finance teams can stay consistent, move faster, and keep client communication human.