What Does It Mean to Remit Payment? A CFO's Guide

What does it mean to remit payment? For CFOs, it's more than a transaction. It's a key control for reducing DSO and improving cash flow. Learn how to master it.

A payment hits your bank account at 9:12 a.m. The amount is large enough to matter. The problem is that nobody on the AR team knows what it pays.

Now the work starts. Someone checks the ERP. Someone else searches email for invoice references. A collector reaches out to the client contact and hopes the remittance advice is sitting in an inbox somewhere. Until that happens, the cash is real in the bank but unclear in the ledger, and your forecast is less reliable than it looked an hour earlier.

That’s the operational reality behind the question, what does it mean to remit payment. In practice, it doesn’t just mean sending money. It means sending money in a way the recipient can identify, post, and reconcile without delay.

The True Meaning of a Remitted Payment

A remitted payment is a payment that has been sent to settle an obligation. In a business setting, that usually means a client paying an invoice by ACH, wire, card, or check.

But controllers know its definition has two parts. The funds have to arrive, and the payment has to be understandable.

If a client sends $42,000 and gives you no invoice detail, that’s not a clean remittance process. That’s a bank event followed by an investigation. Your team has to determine who paid, what invoices were covered, whether any discounts or deductions were taken, and whether the amount should close specific items or sit unapplied.

Why finance teams care about the word remit

In day-to-day finance operations, “remit” is tied to control. A payment becomes useful only when AR can apply it quickly and correctly.

That matters well beyond collections. Unapplied cash distorts aging, hides client behavior, and weakens short-term cash visibility. It also creates avoidable friction with clients. Nothing undermines confidence faster than asking a good payer whether they’ve paid an invoice they already cleared.

A payment without context is not a finished transaction. It’s unfinished accounting.

This shows up in other finance processes too. If you want a simple example of how operational definitions matter, the Explorer Computer LLC payroll insight is useful. Payroll sounds basic until you look at the controls, timing, records, and downstream accounting behind it. Remittance works the same way. The word is simple. The process is not.

The practical definition that holds up in AR

For CFOs, controllers, and firm owners, the best working definition is this:

- Funds are transferred to settle a bill or invoice.

- Payment information travels with the funds or arrives in a reliable linked format.

- The recipient can post the cash with confidence and handle only true exceptions.

That’s the version that improves cash flow. It turns remittance from a clerical detail into a control point inside the cash conversion cycle.

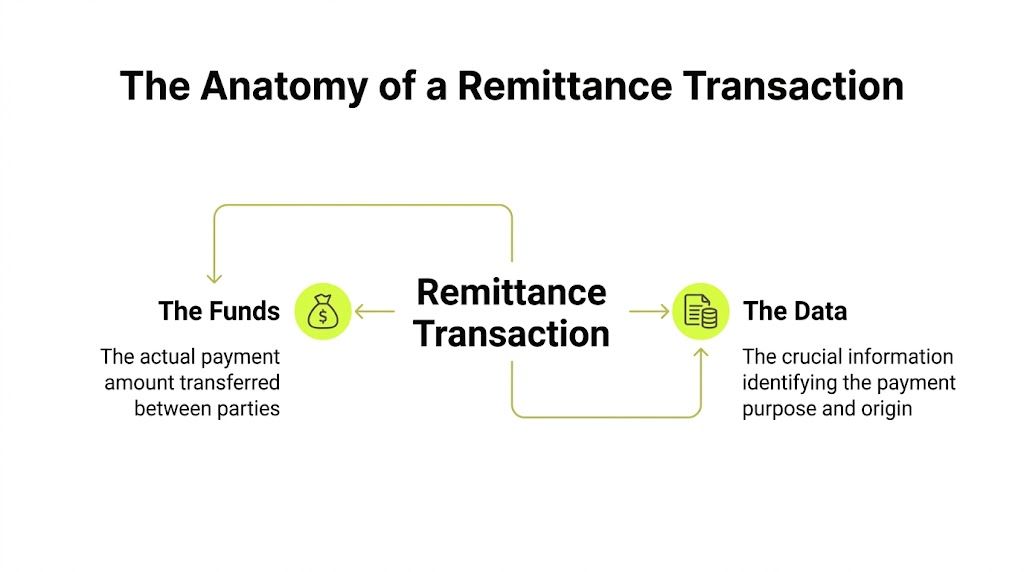

The Anatomy of a Remittance Transaction

A remittance transaction has two components. Think of it as a package and a packing slip.

The package is the money. The packing slip is the data that tells your AR team what the money is for.

If the package arrives without the slip, your warehouse can’t route it. AR works the same way. A deposit without usable advice forces manual review.

The funds

The funds are the actual transfer. In B2B receivables, that usually means ACH, wire, card, or check.

That part is visible. Treasury sees it in the bank. The client sees it leave their account. Finance leadership sees the cash balance move.

What they don’t always see is whether the payment can be applied cleanly.

The data

The second component is the remittance advice. This is the structured or semi-structured information that tells the recipient how to apply the payment.

In B2B accounts receivable, remitting payment involves both the electronic funds transfer and the remittance advice, which can take formats such as EDI ANSI X12 820 and includes invoice numbers and deductions. Without that data, 60-70% of AR teams spend over 20 hours weekly on exception handling, according to Relay’s payment remittance overview.

A useful remittance advice typically includes:

- Payer identity. The legal entity or client name that sent the funds.

- Payee identity. The recipient entity, especially important in multi-entity groups.

- Invoice references. Invoice numbers, credit memo references, or matter IDs.

- Amounts. The amount paid against each invoice, not just the total transfer.

- Adjustments. Discounts taken, deductions, short-pays, or disputed line items.

- Payment method and date. So AR can trace timing and settlement behavior.

Practical rule: If the remittance advice can’t tell a new AR specialist how to post the cash, it isn’t complete enough.

Formats that work and formats that create work

Some remittance data arrives in clean formats. EDI files, portal submissions, XML, and well-structured payment notifications are easier to automate.

Other formats create friction. PDF attachments, email bodies, screenshots, or sparse bank references can still be processed, but they usually require parsing, review, or follow-up.

That’s where process design starts to matter. Teams that want better control don’t just ask clients to pay. They define how clients should send payment detail and how that detail will enter the workflow. A deeper look at automated payment reconciliation is useful here because the actual bottleneck usually isn’t receiving funds. It’s matching them accurately and fast.

Choosing Payment Methods for Data Richness Not Just Speed

Controllers often evaluate payment methods on the wrong axis. They ask which method is fastest for the payer or cheapest per transaction. Those matter, but they aren’t enough.

The better question is this. Which method gives your team usable remittance data with the least cleanup afterward?

A controller’s lens on common methods

Wire transfers are fast. For urgent, high-value payments, they’re often the right choice. But speed alone doesn’t solve the posting problem.

According to Allianz Trade’s remit payment analysis, wire payments settle same-day for $15-50, while ACH takes 2 days for an average of $0.26. The more important issue is data. International wires can take up to 5 days and often lack structured advice, which leads to mystery payments and delays in cash application.

Checks still exist in professional services, especially with long-standing clients or trust-based workflows. They can work if the backup documentation is disciplined. In practice, they often depend on someone mailing or emailing support separately, which introduces timing gaps.

Payment portals tend to perform better operationally because they can require the payer to select invoices, enter reference details, and confirm the intended application before submission. That’s a very different control environment from hoping a wire note field contains enough information.

Remittance Method Trade-Offs

Method | Typical Speed | Average Cost | Remittance Data Quality |

|---|---|---|---|

ACH | 2 days | $0.26 | Often better than checks, but depends on how advice is submitted |

Wire | Same-day domestically; up to 5 days internationally | $15-50 | Often weak or unstructured unless supported by a separate process |

Check | Varies | Qualitatively higher handling burden | Usually dependent on manual backup and internal intake discipline |

Payment portal | Varies by funding method | Varies by setup and payment rail | Usually strongest because data can be required at the point of payment |

What works in real life

The best payment method isn’t always the fastest one. It’s the one your team can reconcile with consistency.

For many firms, that means setting clear preferences:

- Use ACH for routine domestic payments when clients can provide invoice-level support reliably.

- Use wires selectively for urgency or large values, but require remittance details through a separate defined channel.

- Reduce check dependency where possible, especially if supporting documents arrive inconsistently.

- Push clients into structured portals when you want cleaner cash application and less internal rework.

A lot of teams stop at transaction cost. That’s too narrow. The internal cost of reconciliation matters just as much. If a “cheap” payment creates fifteen emails, a manual research trail, and delayed posting, it wasn’t cheap.

For firms comparing rails, payment timing, and bank transfer workflows, sending ACH payments online is part of the decision. But from the receiver’s side, data discipline usually matters more than speed on paper.

Fast money with poor data can be slower to post than slower money with good data.

How Poor Remittance Inflates Your Days Sales Outstanding

DSO doesn’t rise only because clients pay late. It also rises because finance teams can’t apply cash quickly.

That distinction matters. A client may have paid on time, but if the payment lands without enough detail, your ledger still shows open invoices. Collections follow-ups go out. Aging reports stay overstated. Finance leadership sees noise instead of signal.

The chain reaction inside AR

A poor remittance process usually follows the same pattern:

- Cash arrives with little or no invoice detail.

- AR holds the payment unapplied while someone investigates.

- Collectors contact the client to ask what was paid.

- Client response takes time, especially if the original payer, approver, and AP contact are different people.

- Invoices remain open in the system even though cash is already in the bank.

This doesn’t just create extra work. It changes management reporting. Your aging becomes less trustworthy because some receivables are operationally unresolved, not economically unpaid.

The measurable drag on DSO

An estimated 60-70% of B2B payments arrive without sufficient remittance data, forcing 40% of finance teams to spend over 20 hours weekly on manual reconciliation. That drag can inflate DSO by an average of 10-15 days, according to DepositFix’s overview of remit payment operations.

For a professional services firm, that delay affects several decisions at once:

- Cash forecasting gets weaker because unapplied receipts sit in limbo.

- Collections prioritization gets messy because open items may not be unpaid.

- Client communication gets riskier because your team may chase money that has already been sent.

- Month-end close takes longer because unapplied cash requires review and cleanup.

The fastest way to distort AR performance is to treat cash receipt and cash application as the same thing. They aren’t.

Why this hits services firms hard

Professional services firms often invoice by project, retainer, phase, or matter. Clients may combine invoices into one payment, net credits, or dispute only certain lines.

That makes remittance quality more important, not less. If your invoice references and payment references don’t align, AR specialists spend time interpreting intent instead of controlling the ledger. That’s exactly how DSO creeps up while everyone insists clients are “mostly paying.”

Establishing a Remittance Best Practices Framework

A strong remittance process starts before the payment is sent. It begins on the invoice, continues through the payment experience, and ends only when cash is applied cleanly.

This is one of the quieter disciplines inside accounts receivable automation. It doesn’t get much attention until the volume grows and the cracks become expensive.

Global remittance flows reached $831 billion in 2022. In that environment, disciplined processes matter. EBANX’s remittance overview notes that automated remittance matching can cut manual reconciliation time by up to 80%, addressing part of the $200B wasted annually by enterprises on AR burdens.

Build the process on your side first

Many firms ask clients for “payment details” but never define what good looks like. That leaves too much to interpretation.

A better internal framework includes the following:

- State remittance instructions clearly on every invoice. Tell clients exactly where to send payment advice, what references to include, and how to handle partials or deductions.

- Create one intake point for remittance advice. A shared mailbox or structured portal beats scattered messages to partners, project managers, and AR staff.

- Define exception rules. Decide who reviews short-pays, what gets auto-posted, and what requires client confirmation.

- Separate posting rules from relationship management. AR should have a standard operating process, not a different method for every “important” client.

- Track repeat failure patterns. If a specific customer regularly pays without usable backup, that’s a process issue to solve, not a mystery to relive every month.

Make it easier for clients to do the right thing

Clients are more likely to send usable remittance data when the path is obvious. The burden should be low.

That usually means:

- Give them a simple instruction set with examples of acceptable remittance detail.

- Offer a payment channel that supports invoice selection instead of free-form references.

- Acknowledge receipt clearly so AP teams know their payment and support were received.

- Follow up on exceptions quickly while the transaction is still fresh on their side.

Good remittance discipline is a client service issue too. Clean posting prevents unnecessary dunning and avoids awkward payment disputes.

What doesn’t work

Some practices look manageable at low volume but break as the firm grows:

- Letting partners forward payment emails ad hoc

- Allowing multiple remittance inboxes with no ownership

- Accepting partial information and relying on team memory

- Treating unapplied cash as a month-end cleanup item

Those habits are exactly why firms start searching for AR software for professional services after the pain has already spread into close, forecasting, and collections.

How AI AR Automation Achieves Touchless Cash Application

The hard part of remittance isn’t receiving money. It’s handling the variety of ways payment information arrives.

Some clients send structured files. Others email PDFs. Some type invoice numbers into a portal. Others put fragments in bank references or bury details in an email thread. In such scenarios, AI AR automation starts to matter.

What touchless cash application actually means

Touchless cash application means the system ingests incoming payment information, interprets it, matches it to open invoices, and routes only genuine exceptions to a person.

That workflow is practical, not theoretical. Emagia’s glossary on remit payment reports that modern AR platforms with AI-driven parsing achieve a 98% first-pass match rate, compared with 70% for manual processes. The same automated workflow reduces manual intervention by 70-90% and can lower DSO by 15-20%.

That matters for firms running lean accounting teams. It reduces dependency on tribal knowledge and makes posting quality less vulnerable to staffing changes.

How the workflow operates

The underlying mechanics are straightforward:

- Ingestion. The platform collects remittance from email, PDFs, portal submissions, EDI, and bank-related records.

- Extraction. OCR and parsing models pull out payer names, invoice numbers, dates, deductions, and totals.

- Matching. The system compares those details against open AR in the ERP.

- Exception handling. Only partial payments, mismatches, or ambiguous references go to a human queue.

- Posting and visibility. Applied cash updates the ledger faster, and finance leaders get clearer reporting.

QuickBooks AR automation can become meaningful for smaller firms. The value isn’t just “AI” as a label. The value is that incoming remittance from several channels can be normalized into one posting workflow.

Systems create leverage when they absorb format chaos and return accounting clarity.

There’s a broader shift here as well. The idea behind agentic AI for smart controllers is useful because modern finance teams need tools that do more than record transactions. They need systems that evaluate, route, and support decisions while preserving control.

Why this changes the role of AR

When cash application becomes largely touchless, AR staff stop spending most of their day on detective work. They can focus on exceptions that require judgment, such as deductions, disputes, and client-specific arrangements.

That’s a better operating model for a controller. It means fewer manual handoffs, faster close support, and cleaner aging. It also creates the foundation for stronger cash application workflows in accounting.

A short walkthrough helps make the process concrete:

From Remittance Transaction to Strategic Control

Remitting payment sounds administrative. In practice, it sits close to the center of working capital control.

When firms define remittance clearly, choose payment methods with data quality in mind, and build disciplined intake and application workflows, they don’t just clean up AR. They improve cash visibility, reduce noise in collections, and make DSO a truer reflection of customer behavior.

That’s why this topic matters to CFOs and controllers. A remittance process is not just about receiving money. It’s about whether your finance operation can convert incoming cash into reliable accounting quickly and consistently.

If you want tighter control over cash flow, start here.

Resolut helps professional services firms automate AR with a steady operator’s mindset. If your team wants more consistent cash application, cleaner reconciliation, and less manual follow-up, Resolut brings that together in a way that’s accurate, controlled, and still human.