What Is API Connectivity? a Guide for Finance Leaders

What is API connectivity? Learn how linking your financial software helps reduce DSO, improve cash flow, and automate accounts receivable for your firm.

Month-end often exposes the same problem.

Your team pulls invoice data from the PSA or CRM. Someone exports aging from QuickBooks. Someone else checks the bank portal to see what cleared. Then collections starts sending follow-ups from a spreadsheet that's already out of date. By the time leadership asks for a cash view, finance is working from three systems and too much judgment.

That's where many firms start asking a technical question that is really an operating question. What is API connectivity, and why does it matter to cash control?

For a CFO, controller, or firm owner, the answer isn't about code. It's about whether your billing, payments, and collections processes run as one system or as a chain of handoffs. In firms trying to improve cash flow, reduce DSO, and make accounts receivable automation work, that difference matters.

The Hidden Cost of Disconnected Systems

Disconnected systems rarely fail in dramatic ways. They fail subtly.

An invoice goes out from one system, but the collections tool doesn't see it until the next import. A client pays through a portal, but QuickBooks isn't updated until someone posts the receipt. Sales says the account is current. Finance says it's overdue. Both are looking at different data.

In professional services firms, this becomes an operating drag fast. The team spends time reconciling instead of collecting. Follow-ups go out late. Disputes take longer to resolve because no one has a complete record in one place. Cash forecasting gets softer because open AR and cleared payments don't line up cleanly.

Where the cost shows up

The cost isn't only labor. It shows up in control.

- Delayed outreach: If invoice status moves slowly between systems, reminders go out late or not at all.

- Duplicate work: Staff rekey data from one tool into another, then check it again because they don't trust the first pass.

- Weaker visibility: Leaders see snapshots instead of a current AR position.

- Collection risk: Clients receive inconsistent communication, which makes payment slower and relationships harder to manage.

Disconnected finance operations create small delays at every step. Those delays compound into slower collections and less confidence in the numbers.

This is why firms start moving toward tighter workflow design, not just better reporting. If you're already thinking about straight-through processing in finance operations, API connectivity is one of the structural pieces that makes that possible.

Why manual bridges stop working

Manual bridges work when volume is low and complexity is limited. They break when your firm adds more clients, payment methods, entities, or billing rules.

A controller can manage around a bad process for a while. A growing firm usually can't. Once AR depends on exports, imports, and inbox monitoring, the process becomes person-dependent. That means cash collection quality depends on who's in the seat and how careful they are that week.

API connectivity changes that. It replaces ad hoc handoffs with direct system-to-system communication.

What Is API Connectivity in Plain English

Your AR lead marks an invoice as paid. The customer record updates in one system, but not in the others. A collector follows up on a balance that is already settled. Finance loses time fixing the error, and the client gets a poor experience.

API connectivity reduces that kind of gap.

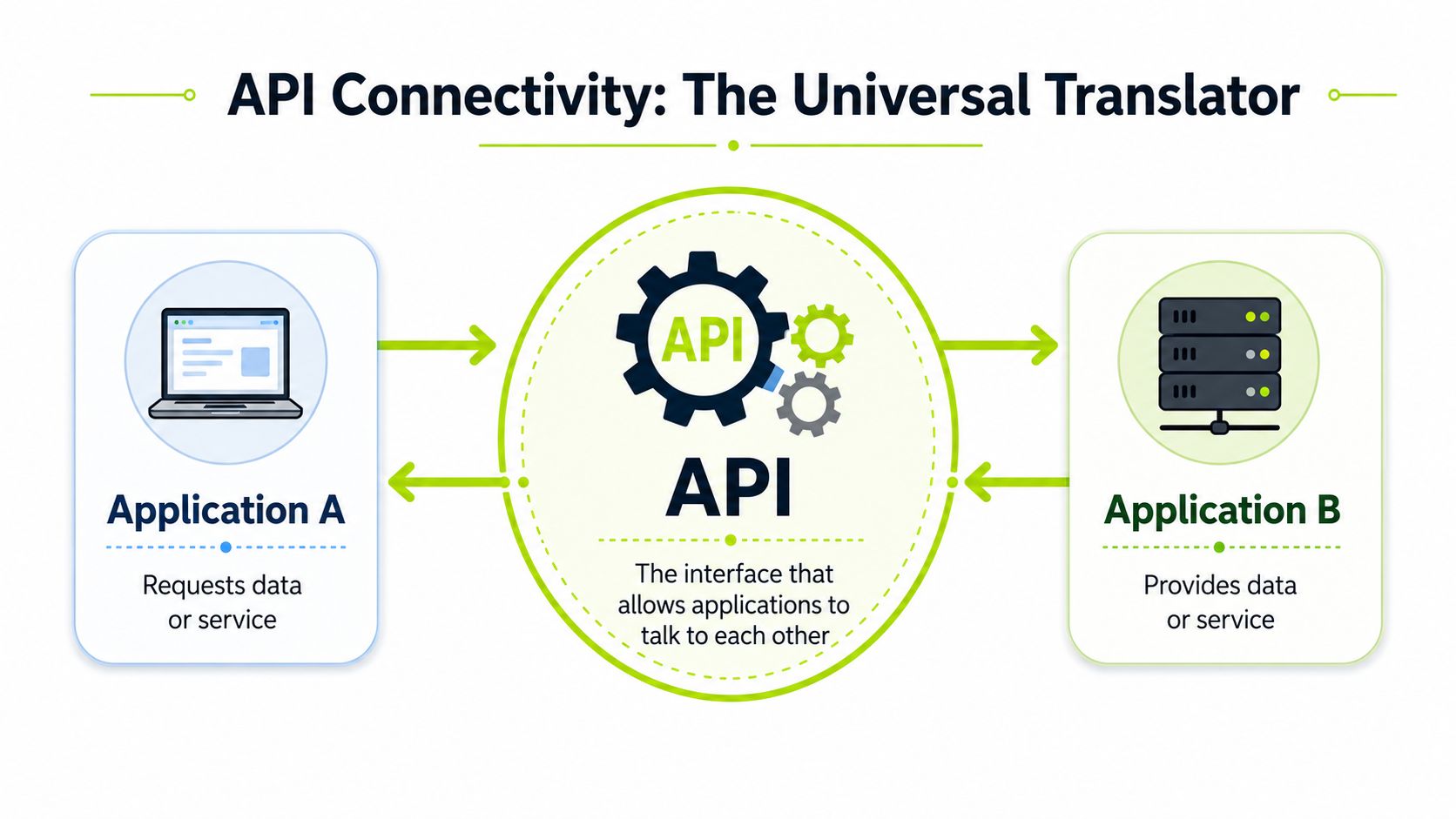

In plain English, API connectivity means one system can request data from another system, send an update, or trigger an action through a defined set of rules, without someone rekeying information. For a finance team, that means billing, payment, and AR systems can stay aligned as work happens.

An API works like a service menu with instructions. One application does not need access to another application's internal code. It needs a clear way to ask for the right data, in the right format, with the right permissions.

For CFOs and controllers, the operational point is simple. Predictable data movement supports predictable cash processes. If your ERP, AR platform, and payment workflow exchange updates the same way every time, you get fewer timing errors, fewer manual checks, and better confidence in the numbers.

The contract matters more than the code

The core of API connectivity is the contract.

That contract defines what each system can send, what it can receive, how access is approved, and what response should come back. It covers the endpoint, request type, data structure, authentication, and error handling. Good APIs are consistent. Weak integrations depend on patches, inbox monitoring, or manual cleanup when something changes.

That difference shows up fast in accounts receivable. If a payment posts through a hosted payment gateway for B2B collections, the next question is whether that payment status reaches the ledger, customer record, and collections workflow without delay. API connectivity is what makes that handoff reliable enough to support tighter collection control.

Practical rule: If a vendor cannot explain how data moves, who can access it, and what happens when a request fails, the integration will create finance work later.

For finance teams reviewing vendors, it helps to understand the basics of mastering API design best practices so you can separate a documented integration from a loose sync with manual dependencies.

For a visual explanation of how APIs work, see the video below.

What API connectivity is not

API connectivity is not a shared login across tools. It is not a nightly CSV export. It is not a staff member checking two systems and copying changes over.

A firm can buy modern software and still run a disconnected process. If staff must watch for payment updates by hand, trigger reminders manually, or reconcile exported files before they trust the balance, the systems are not connected in a way that improves control.

Finance leaders should focus on this operational distinction. The question is not whether a platform claims to integrate with QuickBooks. The question is whether the connection supports accurate records, timely action, and cleaner cash collection.

The Mechanics of a Securely Connected System

Month-end closes. Cash is in motion. Then a payment posts in one system but not the other, and AR staff start checking records by hand. That is usually the moment API connectivity stops feeling like an IT detail and starts looking like a control issue.

Securely connected systems rely on clear API contracts. The rules for what gets sent, who can send it, how it is validated, and how failures are handled need to be defined up front. The UK government's API technical and data standards outline common practices such as REST, JSON, HTTPS/TLS 1.2+, OAuth 2.0, input validation, and rate limiting, along with design principles that support stable production use.

For finance, those standards matter because they reduce avoidable exceptions. A connected AR process only helps if invoice status, payment activity, and customer actions move accurately enough to support collections and reconciliation without extra review.

The core moving parts

These are the terms finance teams are likely to hear in vendor reviews, and what they mean in operational terms:

- REST: A common way systems request and return information. It makes integrations easier to document, test, and maintain.

- JSON: A structured data format. It keeps records readable and consistent across systems.

- OAuth 2.0: A permission method that lets one system access another without exposing a shared username and password.

- Rate limiting: A control that caps request volume so one platform does not overload another or trigger avoidable failures.

- Input validation: A check on incoming data. It catches bad or incomplete values before they affect invoices, payments, or customer records.

- Webhooks: Event-driven notifications. One system sends an update when something happens, such as a payment posting or an invoice being viewed.

In AR, webhooks matter because timing affects collections. If a client pays, opens a payment request, or a reminder bounces, the next action can happen quickly instead of waiting for a scheduled sync or manual review.

What security looks like in practice

Security in connected finance systems comes down to controlled access and visible exceptions. The connection should be narrow, logged, and easy to audit.

A vendor should be able to answer these questions without hand-waving:

Control area | What you want to hear from a vendor |

|---|---|

Access | Only approved applications and named users can send or receive data |

Encryption | Data is protected in transit between systems |

Permissions | The connection only reaches the records and actions it is meant to handle |

Validation | Bad data is blocked or flagged before it changes balances or workflows |

Monitoring | Failed calls, retries, and exceptions are tracked so finance can trust the record |

A secure integration narrows access and makes failures visible.

The payment step deserves extra scrutiny. If your AR workflow includes payment links, customer portals, or stored payment methods, the handoff between invoice data and payment processing needs clear ownership and controls. Teams reviewing that part of the process should understand how a hosted payment gateway supports receivables workflows.

What usually goes wrong

The failures are usually predictable.

One common problem is over-customization. A vendor builds around one firm's process, but the field mappings, assumptions, and fallback rules are poorly documented. Then an ERP field changes, a CRM status is renamed, or a payment processor updates a response format. Finance often discovers the break after reminders stop, cash application stalls, or client balances no longer match.

Another problem is weak exception handling. The integration handles the standard invoice and full-payment case, but partial payments, short pays, disputes, duplicate records, and failed retries have no clear path. Controllers lose confidence quickly when teams have to investigate those cases in email threads and spreadsheets.

Good connected systems do not remove every exception. They keep ordinary transactions moving and make abnormal ones easy to spot, assign, and resolve.

The Financial Case for API Connectivity

Many firms still treat API connectivity as an IT line item. That's too narrow.

For finance, connected systems shape the speed and quality of cash conversion. If invoice creation, payment updates, reminders, and reconciliation move together, the team can act sooner and with better information. That's the core value behind accounts receivable automation and AI AR automation. Not novelty. Control.

Why this is now a business issue

The market has already moved past the idea that APIs are just back-end plumbing. Juniper Research projects operator revenue from network APIs at $283 million in 2025 and $8.1 billion in 2030, a projected compound annual growth rate of about 76% over that period, as reported in Juniper Research's network API market research.

That same source notes that major ecosystems such as the OECD and CME Group use APIs for data delivery. For a finance leader, the takeaway is simple. API connectivity is now infrastructure for how businesses distribute, access, and act on critical information.

What changes on the finance side

The benefit isn't “better tech.” It's a tighter operating model.

When systems connect well, firms can:

- Reduce manual reconciliation: Payment and invoice status move automatically instead of waiting for staff review.

- Improve cash flow visibility: Finance can see receivables activity closer to real time.

- Reduce DSO pressure: Follow-up timing improves because reminders are triggered by actual invoice and payment events.

- Lower process risk: Teams spend less time comparing reports from systems that don't match.

- Support scale without adding friction: More invoices and more clients don't automatically mean more admin work.

If your collections process depends on exports and inbox monitoring, you don't have an AR strategy. You have a labor strategy.

QuickBooks AR automation becomes financially relevant. A clean connection between the ledger, payment system, and outreach workflow reduces lag between what happened and what finance knows happened.

That doesn't mean every firm needs a large transformation project. It does mean finance should ask harder questions about where cash delays start. In many firms, the issue isn't invoice quality. It's the gap between systems.

What doesn't produce results

Buying another dashboard usually doesn't fix this. Neither does adding a collections tool that sits beside your accounting system without updating it reliably.

The firms that improve cash flow tend to fix the process backbone first. They connect source systems, define ownership for exceptions, and automate repetitive steps where timing matters most. That's where API connectivity earns its keep.

API Connectivity in AR Automation A Real-World Example

A real AR workflow makes the concept easier to evaluate.

Take a professional services firm that invoices from QuickBooks after a milestone is approved. The finance team wants less manual follow-up, cleaner reconciliation, and fewer “did they pay yet?” checks across systems.

How the workflow runs when systems are connected

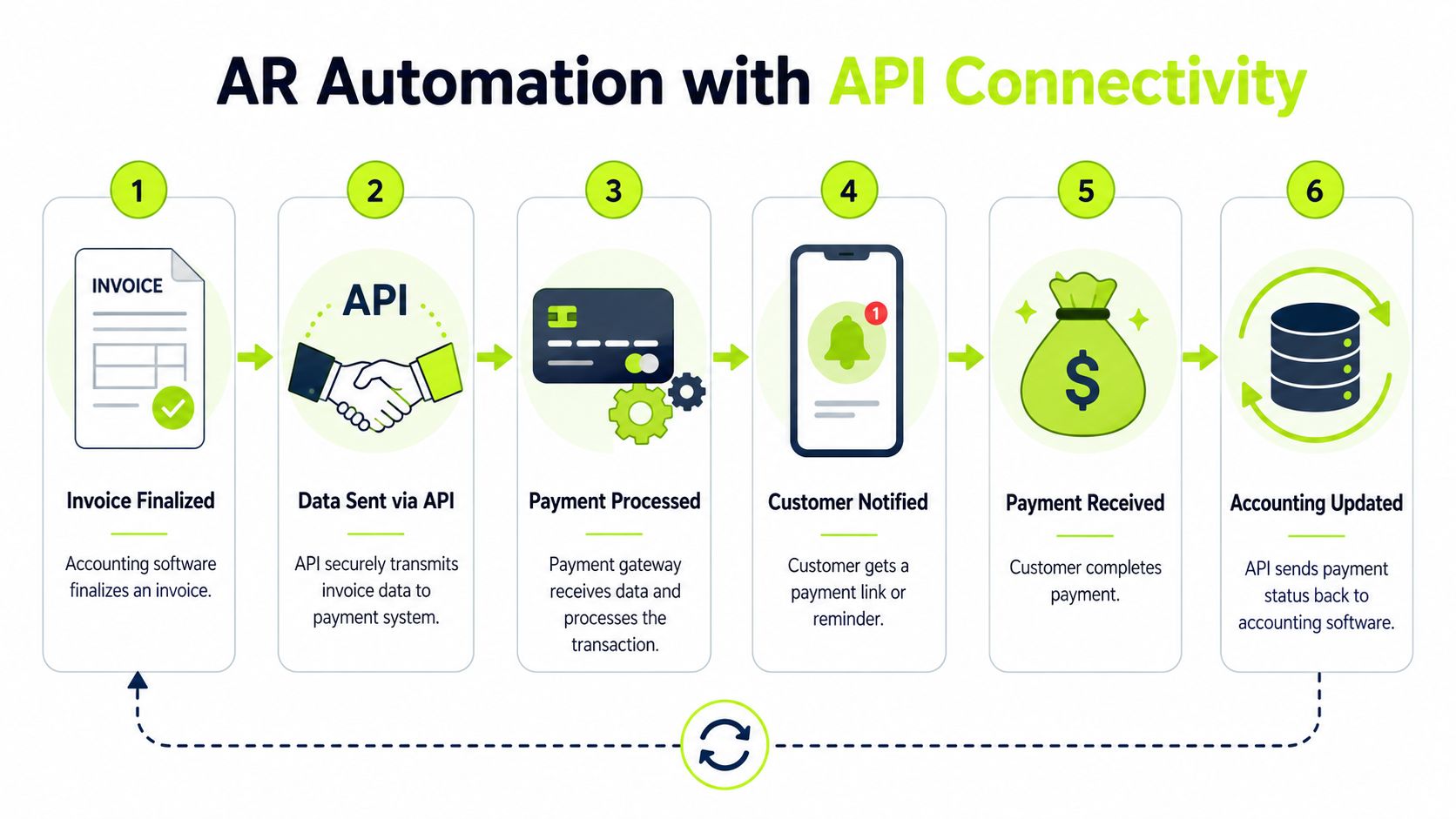

The invoice is finalized in QuickBooks. That event is sent through an API to the AR automation platform. The platform receives the customer record, invoice amount, due date, and any relevant billing metadata.

From there, the workflow can branch based on rules the finance team sets.

A long-standing client might get a polite reminder sequence that starts closer to the due date. A new client with tighter terms might receive earlier prompts. A strategic account might route exceptions to an account manager before escalation. The point isn't just automation. It's controlled automation.

When the client opens the payment link and pays through the payment portal, another API event confirms the transaction. That payment status then flows back to the AR system and to QuickBooks. The invoice is marked appropriately, collections outreach stops, and the finance team sees the updated status without manual posting.

What manual AR looks like beside it

The contrast is usually stark.

Step | Manual process | Connected process |

|---|---|---|

Invoice created | Team exports or rekeys invoice data | Invoice data passes automatically |

Reminder timing | Staff check aging and send manually | Rules trigger outreach from live invoice status |

Payment confirmation | Staff log into portal or bank to verify | Payment event updates connected systems |

Reconciliation | Accounting matches receipts later | Status sync supports faster cash application |

Exception handling | Problems surface through email chains | Exceptions are visible in workflow |

This is the operational core of accounts receivable automation. APIs do the transport work. The finance team sets the rules.

Why this matters for DSO and cash flow

A connected process doesn't guarantee every client pays on time. It does remove preventable delay inside your own firm.

Common gains show up in a few places:

- Faster first touch: Reminders start on schedule because they aren't waiting on spreadsheet prep.

- Cleaner customer communication: Paid invoices stop receiving chase emails once systems update properly.

- Better cash application: Payment data is easier to match when the systems share the same identifiers and timing.

- Less staff time on status checks: Teams focus on exceptions and high-risk accounts.

- More confidence in AR reporting: Finance works from a current operating picture, not a stitched-together snapshot.

For firms evaluating AI AR automation, this distinction matters. AI can help with prioritization, message timing, or workflow decisions. But if the underlying systems don't exchange invoice and payment data reliably, the automation layer sits on weak ground.

Good AR automation doesn't replace discipline. It enforces it consistently.

Where firms trip up

The most common failure isn't technical inability. It's designing around the wrong trigger.

Some teams automate reminders based on invoice export dates instead of actual invoice creation. Others treat a payment submission as the same thing as cleared payment. Some never decide who owns exceptions such as short payments, disputed line items, or unapplied cash.

Those design choices affect whether your QuickBooks AR automation effectively reduces workload or just moves it around.

A finance-grade connected AR process usually has these traits:

- A single source invoice event from the accounting system.

- Clear status definitions so “sent,” “viewed,” “paid,” and “reconciled” don't get mixed together.

- Rules for exception routing instead of relying on inbox memory.

- Feedback into accounting so collections activity and ledger status stay aligned.

That's the practical answer to what is API connectivity in finance. It's the infrastructure that lets AR software for professional services behave like part of the finance operation, not a separate tool.

Implementing a Connected AR Strategy in Your Firm

Most firms don't need to start with a platform search. They need to start with a process map.

List the systems that touch receivables today. Usually that includes your accounting platform, PSA or CRM, payment processor, bank visibility tools, and whatever the team uses for reminders. Then mark where data is re-entered, where status is checked manually, and where errors tend to appear.

Questions worth asking vendors

When you evaluate AR software for professional services, ask direct questions.

- Accounting connection: Does it connect natively with QuickBooks, and what invoice and payment events sync automatically?

- Payment status handling: What happens after a client pays. Does the system update status immediately, or only after a later batch process?

- Exception workflow: How are short pays, disputes, and unapplied cash surfaced?

- Security model: What authentication method is used, and how is access limited?

- Auditability: Can finance see what was sent, what changed, and when?

- Operational ownership: Can your team adjust rules without custom development?

If your firm uses multiple ledgers or service lines, ask how the platform handles those structures. If you're on Xero rather than QuickBooks, it also helps to review firms that specialize in Xero bookkeeping services so your system design stays aligned with how finance closes the books.

Start with one high-friction workflow

Don't automate everything at once.

A low-risk starting point is the path from invoice finalization to first reminder. Another is payment confirmation back into accounting. Those are narrow enough to manage and important enough to improve quickly.

For firms that want a practical roadmap, this guide on how to automate accounts receivable is a useful reference point.

The firms that get the most from API connectivity usually keep the scope disciplined. They fix one broken handoff, prove trust in the workflow, then expand. That's how you reduce DSO, improve cash flow, and make AI AR automation useful instead of ornamental.

Resolut automates AR for professional services. It helps firms run collections with more consistency, more accuracy, and a more human experience. If you want a cleaner path from invoice to cash, learn more about Resolut.