What Is Billing Information: Your Firm's Cash Flow Engine

What is billing information? Learn components, why accuracy reduces DSO, & how AR automation streamlines collections for better cash flow.

Billing information is the complete, structured dataset required to identify a payer, execute collection, and reconcile the payment afterward. In a payment environment that handled 4.96 billion transactions in Ireland in 2025, including 3.30 billion card payments, that data isn't administrative clutter. It's a control surface for cash flow.

Most finance teams start with the wrong mental model. They think billing information means a billing address, maybe a contact name, and whatever sits on the invoice template. That view is too narrow for any firm that cares about speed to cash.

For a professional services firm, billing information determines whether an invoice routes to the right approver, whether a card authorizes, whether an ACH instruction is usable, whether a payment matches cleanly in the ledger, and whether collections can proceed without a week of email cleanup. If the data is incomplete, stale, or inconsistent, the invoice may still go out. But cash won't move with the same reliability.

That's why this matters at the CFO level. If you want to reduce DSO, improve cash flow, and get more value from accounts receivable automation, you have to treat billing data as a managed financial asset, not as a form field someone filled in once during onboarding.

Introduction Beyond the Address Line

Billing information decides how quickly revenue turns into cash. When it is wrong, incomplete, or stale, the invoice may still go out, but approval slows, payment fails, and cash application turns into manual repair work.

The expensive part is rarely the original error. It is the operational drag that follows. A bad contact record sends the invoice to the wrong inbox. A missing purchase order reference stops approval. Expired card or bank details trigger failed collection attempts. Then AR staff spend time clearing exceptions, reissuing documents, and answering preventable emails instead of accelerating receipts.

Controllers usually see the pattern before it reaches the board deck. New CFOs often encounter it later, when aging slips, collections become less predictable, and the cash forecast starts carrying more judgment than evidence. On paper, each issue looks minor. Across a quarter, it becomes a working capital problem.

What billing information includes

Billing information is the structured payment and payer data needed to bill, collect, and reconcile correctly. That includes the payer's legal identity, invoice destination, payment method details, bank or card credentials where appropriate, required customer references, and any routing fields that determine who can approve and release payment.

That definition matters because finance teams often maintain invoice data and payment data in separate places, with separate owners and different update cycles. Customers do not experience those handoffs. They see one payment journey. If the invoice record, customer master, and payment profile do not align, the break shows up in the middle of the cash cycle.

Practical rule: If a field can delay approval, prevent authorization, interrupt settlement, or create a cash application exception, it belongs in your billing data control framework.

Why the definition changed in practice

The cleanest way to separate the issue is data versus workflow. Billing information is the record. Billing is the process of issuing, collecting, posting, and reconciling. Finance teams need that distinction because process improvement stalls when the underlying record is unstable.

In professional services, this gets real fast. Retainers, milestone invoices, reimbursable expenses, split billing across entities, and client-specific approval chains all depend on accurate billing records behind the invoice. If those records drift, automation rates fall, exception queues grow, and DSO moves in the wrong direction.

Use this test:

- Billing information is the structured record of who pays, where the invoice goes, how payment is made, and which references must appear.

- Billing process is the sequence of invoice creation, delivery, collection activity, posting, and reconciliation.

- Financial impact shows up when poor data forces the process to absorb avoidable manual work.

The question is not what billing information means in a glossary. It is whether your firm treats it with the same control discipline as any other asset that affects liquidity.

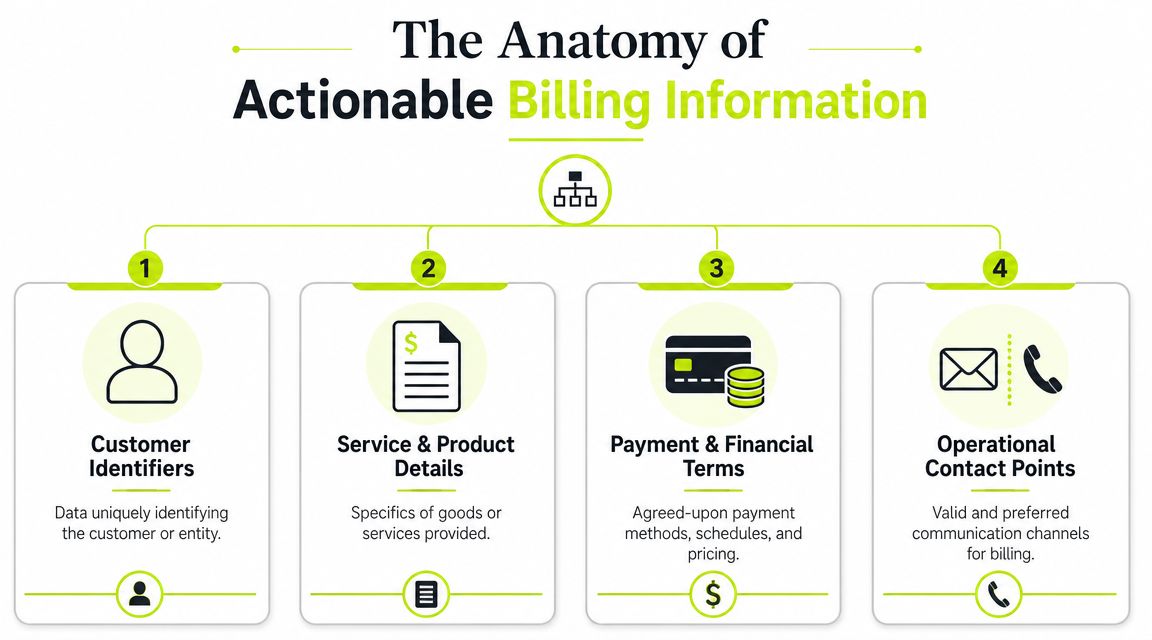

The Anatomy of Actionable Billing Information

A useful billing record is built for collection, not just documentation. It has to help your team issue the invoice correctly, present the right payment options, satisfy customer requirements, and close the loop in the ledger without unnecessary touches.

Payer identity and routing

The first group is payer identity. That includes the legal customer name, billing entity, billing contact, billing email, physical address where needed, and any customer code the buyer uses internally.

This is the part most firms think they've covered. Often they haven't. The common failure isn't that the customer name is wrong. It's that the paying entity, approver, or invoice destination changed and no one updated the file.

Invoice detail and commercial context

The second group is invoice detail. This includes invoice number, invoice date, service descriptions, quantities where relevant, pricing, tax treatment, payment terms, and customer-specific references such as matter number, engagement code, or purchase order.

Service firms create avoidable friction. A technically correct invoice can still be operationally unusable if it lacks the reference the client's AP team requires. If your firm pulls data extracted from receipts into expense or reimbursable billing workflows, you already know the value of structured fields over PDF archaeology.

For firms tightening process discipline, this is also where a clean definition of the invoice itself helps. Resolut's guide to what a payment invoice is is a practical reference for distinguishing the commercial document from the surrounding collection workflow.

Payment method data and richer transaction fields

The third group is payment method data. That includes card credentials where permitted, ACH or EFT details, bank account identifiers, routing information, and stored preferences about which rail the customer will use.

In card processing, the data can become more detailed than many finance teams realize. Marqeta explains that Level 1 transaction data typically includes the card number, transaction amount, currency code, merchant name, merchant category code, and transaction date. Level 2 and Level 3 fields add details such as tax amount, customer code, merchant postal code, product descriptions, quantities, and item-level pricing. In major card networks, those richer data sets are especially relevant in business and government transactions, where more complete submission can support better processing economics, according to Marqeta's overview of Level 1, 2, and 3 data.

That matters for professional services because richer data improves more than acceptance. It improves traceability. Better structured inputs usually mean cleaner customer conversations later.

Compliance and tax controls

The fourth group is compliance and tax data. This may include tax IDs, exemption status, jurisdictional information, consent records for stored payment methods, and evidence that billing instructions were captured through an approved process.

A concise operator view looks like this:

Billing data group | What it supports |

|---|---|

Payer identity | Invoice routing, payer verification, account ownership |

Invoice detail | Approval, dispute prevention, matching to services delivered |

Payment method data | Authorization, settlement, recurring collection |

Compliance and tax data | Valid storage, correct tax handling, audit readiness |

When teams ask what works, the answer is simple. Capture only the fields that drive approval, payment, and reconciliation. Then keep those fields current.

How Billing Data Quality Governs Cash Flow

Billing data quality is a cash flow control. Treat it like clerical hygiene and DSO drifts up. Treat it like production data for revenue conversion and cash arrives faster, with fewer touches and fewer write-offs.

A services firm can finish the work, approve the time, send the invoice, and still miss its cash target because one field was wrong before the invoice left the system. The failure rarely sits in revenue recognition. It shows up in invoice acceptance, approval routing, collection timing, and cash application. AR aging reports the result. Billing master data is often the source.

The cause and effect path

The operating chain is straightforward. Accurate billing records reduce invoice exceptions. Fewer exceptions mean fewer holds inside the customer's AP process. That shortens the time between invoice release, collection, and posting cash to the right account.

In practice, the failure points are predictable:

- Wrong billing contact sends the invoice to someone with no approval authority.

- Missing customer reference or PO number gives AP a clean reason to reject or park the invoice.

- Outdated payment instructions cause scheduled collections to fail and push the account into manual recovery.

- Incorrect terms or payer entity create avoidable disputes that delay payment and consume staff time.

One bad field does not look strategic on its own. Across hundreds of invoices, it becomes a working capital problem.

Clean AR performance starts with issuing the right invoice to the right legal entity, through the right channel, with the right supporting data, the first time.

Why automation underperforms on weak records

AR automation can speed a good process. It cannot rescue a bad billing record. If payer instructions, approval routing, or customer references are wrong, software will send reminders faster and escalate exceptions more neatly. The invoice is still defective.

That is why experienced finance teams judge automation upstream first. Can the process catch billing errors before invoice release. Can it stop an invoice that is missing a required reference. Can it flag a mismatch between the contracted payer and the bill-to entity before the customer sees it.

The same discipline also improves the back end. Teams that tighten invoice data usually see fewer unapplied receipts, faster posting, and less manual research in cash application. A useful companion process is automated payment reconciliation, because clean invoice data and clean receipt matching rely on the same controls.

A short walkthrough can help make the point concrete:

What good looks like in a services firm

For project and retainer billing, the standard is controlled reliability. Finance needs a pre-bill check that confirms the payer entity, billing destination, required references, tax treatment, and payment terms still match the current engagement and customer setup.

That review should happen before release. After a customer rejects an invoice, the team is already paying the penalty through delay, rework, and weaker collection ability.

The strategic point is simple. Billing data is not back-office exhaust. It is an operating asset that governs how quickly booked revenue becomes usable cash. CFOs who want lower DSO should ask for billing data accuracy by customer, by team, and by invoice exception type, then manage it with the same discipline applied to pipeline, margin, and forecast accuracy.

Securing Billing Data for Compliance and Trust

Weak billing-data controls create two expensive failures at once. They slow collections, and they create avoidable compliance exposure.

Billing information belongs in the same control conversation as cash, revenue recognition, and vendor bank changes. It identifies who should pay, where the invoice should go, which payment method is valid, and in many cases which account can be charged or credited. If those records are wrong, finance feels it through delayed settlement, disputed invoices, failed payment attempts, and time lost proving which record is current.

Security starts with restraint.

The safest billing record is the one designed for the transaction you need to process. Teams get into trouble when they collect more than operations require, then scatter that data across ERP notes, shared inboxes, CRM fields, ticket threads, and spreadsheets. At that point, the control problem is not only confidentiality. It is record authority. AR cannot collect cleanly if three systems disagree on the payer entity or remittance instruction.

A practical review usually starts with four questions:

- What billing data is required to invoice, collect, apply cash, and support audit review?

- What payment data should never be stored by finance because a processor or portal should hold it instead?

- Who can view versus change payer details, tax settings, and payment instructions?

- What verification step is required before a bank account, card, or billing-contact update becomes active?

The billing address deserves more respect than it usually gets. In card environments, it can affect address verification, authorization success, and chargeback handling. In B2B invoicing, it also signals whether the invoice is tied to the right legal entity, location, and tax treatment. A stale address field can start as a data-entry issue and end as a cash-collection issue.

Changes to billing records should follow a controlled workflow. Email requests alone are not enough for bank instruction changes, payer-entity updates, or contact swaps tied to active collections. The risk is straightforward. Fraudsters target weak handoffs, and internal teams under collection pressure often bypass review steps to get an invoice out.

Finance does not need to run the security program, but it does need to define the control requirements. If your team is comparing standards, this overview of key differences for compliance audits is a useful reference for how PCI-focused payment controls differ from broader governance frameworks.

For a professional services firm, a workable governance model usually includes clear ownership of the billing master, role-based access, approved change controls, and retention rules that remove outdated payment data on schedule. Those are not abstract policy items. They protect cash conversion. The more confidence customers have in your invoicing and payment handling, the less friction collections teams face when it is time to get paid.

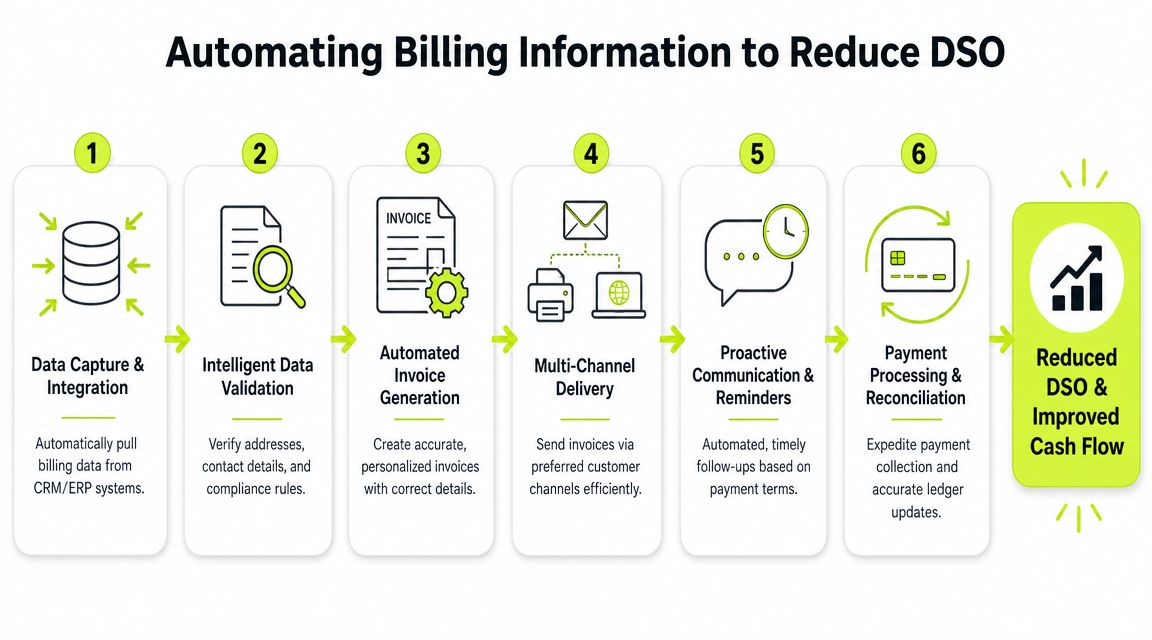

Automating Billing Information to Reduce DSO

Billing automation is not a clerical upgrade. It is a cash conversion control.

Teams reduce DSO when billing data moves through the order-to-cash process without breaking at handoffs between sales, finance, customer success, and collections. If the billing contact changes in the CRM but not in the accounting system, the invoice goes to the wrong inbox. If the legal entity changes but tax and payment records do not, AP rejects the invoice. Those delays look like collection problems on a dashboard. In practice, many of them start as poor data flow.

What automation should do

Automation should enforce discipline at the points where AR teams lose time and invoices lose momentum. The goal is not more notifications. The goal is fewer preventable exceptions before an invoice is issued and fewer avoidable disputes after it lands with the customer.

A finance team needs billing data, payment method data, and invoice data to stay aligned across recurring billing, customer portals, and collections workflows. That matters most in environments where charges depend on current contract terms, active approvals, and current payer information, as discussed in Ordway's analysis of billing address and recurring billing operations.

In practice, good QuickBooks AR automation or broader AR tooling should do four jobs well:

- Capture changes early when a client updates billing contacts, payer entity, purchase order rules, or payment preference.

- Validate required fields before invoice release, especially the records that determine delivery, tax treatment, and cash application.

- Sync approved changes across CRM, ERP, accounting, and payment systems so the collections team is not working from stale records.

- Route exceptions to finance when invoice data, contract terms, and payment profiles no longer match.

If you want the wider operating model behind this, what is business process automation is a useful reference. The point is process reliability across systems, not isolated task automation.

Where AI helps and where it doesn't

AI has value here, but only in the right layer of the process. It can flag anomalies, identify stale records, detect missing fields before billing runs, and suggest which accounts need outreach after a failed invoice delivery or payment attempt. That saves collector time and helps finance intervene before an issue turns into aged receivables.

It does not set policy. Finance still has to define the billing master, decide which fields are required by customer type, and specify which changes need review before they touch live invoicing.

That is why firms evaluating invoice automation software should look past feature lists. The better question is whether the tool supports your control design, exception handling, and ownership model across the full AR cycle.

Resolut is one example in the market. It combines collections workflows, payment options, and automated cash application in one AR operating layer. For a services firm, that matters because billing data maintenance, customer follow-up, and payment matching often fail when each step sits in a separate system with separate owners.

A practical automation sequence

The rollout does not need to be complex. It does need to be disciplined.

- Define the billing record by customer type, contract type, and payment method.

- Assign system ownership so one field has one source of truth.

- Set validation rules before invoice release, not after a dispute is opened.

- Build customer update workflows for contact, entity, and payment changes.

- Push exceptions into AR queues with clear accountability and aging targets.

That is how automation lowers DSO in practice. Faster reminders help. Fewer bad invoices help more.

Conclusion From Data Point to Strategic Asset

The question “what is billing information” sounds basic. In practice, it's one of the sharper diagnostic questions a CFO can ask. If the answer inside your firm is “name, address, and where to send the invoice,” your cash process is probably carrying more hidden friction than it should.

At scale, small data problems don't stay small. In Ireland, payment service providers recorded 4.96 billion payment transactions in 2025, up 8.8% from 2024, with total payment value reaching €12.16 trillion, and 3.30 billion of those transactions were card payments, according to the Central Bank of Ireland's payment services statistics. In high-volume environments like that, even minor errors in payer name, address, or invoice reference can delay reconciliation and collections. The same logic applies inside a midsize services firm. The volume is lower. The operational truth is the same.

The CFO lens

A mature finance team treats billing information as part of revenue operations, cash management, and internal control. It defines the record carefully, secures it appropriately, and maintains it continuously.

That changes the conversation from “Why are customers paying late?” to more useful questions:

- Did we invoice the right legal entity with the right references?

- Did the customer receive the invoice where their AP workflow operates?

- Did our payment method data still match how they intended to pay?

- Did our systems keep billing, invoice, and payment records synchronized?

Strong cash performance often starts with a quiet discipline. Accurate customer billing data, maintained consistently, before anyone sends the invoice.

What to inspect next

If you want better collections performance, start upstream. Review the fields required at client onboarding. Check whether billing contacts and payment instructions are being refreshed on a schedule. Look at every invoice exception from the last quarter and identify how many were preventable with cleaner source data.

That's the practical shift. Billing information stops being a back-office detail and becomes a strategic asset that supports cash velocity, client trust, and financial control.

Resolut automates AR for professional services with a focus on consistency, accuracy, and human oversight. If your team wants cleaner billing records, tighter collections workflows, and a more reliable path from invoice to cash, Resolut is built for that operating model.