What Is Credit Underwriting: CFO Guide to Cash Flow

Discover what is credit underwriting & its impact on your firm's cash flow. This 2026 guide helps CFOs manage B2B credit risk & reduce DSO effectively.

A client signs the engagement letter. The work starts fast. Delivery is on track, the partner is happy, and revenue looks booked.

Then the invoice ages. The client asks for extra time. Your team follows up politely, then more firmly. What looked like a sales win turns into a working capital problem.

That's why CFOs should care about credit underwriting. In a professional services firm, underwriting isn't bank jargon. It's the discipline of deciding who gets terms, how much exposure you'll carry, and what controls you need before receivables start drifting. If you're asking what is credit underwriting, the useful answer isn't “a credit check.” It's a risk management process that shapes cash flow, client experience, and the amount of time your team spends chasing money that should've arrived on time.

Deconstructing Credit Underwriting

Credit underwriting is the process of assessing whether a borrower is likely to repay and under what terms credit should be extended. In practice, that means it's less about approval and more about risk structuring.

For a professional services firm, the question usually isn't whether a client can pay a consumer loan. It's whether they can pay your invoices consistently while managing payroll, taxes, debt, and the demands of their own customers. That requires a broader view than a simple score.

Modern underwriting also sits on top of a large data infrastructure. In the U.S., the CFPB reported that major credit reporting agencies receive information from approximately 10,000 furnishers and monthly updates on over 1.3 billion consumer credit accounts, while the average consumer credit file contains 13 past and current credit obligations. That scale shows why underwriting relies on aggregated history, not a single datapoint, according to the CFPB credit reporting white paper.

The five Cs still matter

The classic framework is the Five Cs of Credit. It's old, but it still works if you translate it into B2B reality.

- Character means payment behavior. Has this client paid firms like yours on time, or do they stretch terms as a habit?

- Capacity is the client's ability to generate enough cash to cover your invoices alongside every other obligation.

- Capital asks whether the business has enough financial resilience to absorb a bad quarter without pushing vendors out.

- Collateral matters less in many service engagements, but substitutes exist. Deposits, retainers, milestone billing, and personal guarantees can all serve a similar protective function.

- Conditions cover the surrounding context. A profitable client in a weakening sector deserves a different structure than a stable client with recurring revenue.

Practical rule: If your team can't explain why terms were granted, you don't have underwriting. You have optimism.

What this looks like in a services firm

A law firm, agency, consultancy, or accounting practice usually extends trade credit without calling it that. Net terms, phased billing, and work started before cash is collected are all credit decisions.

The mistake is treating those decisions as relationship exceptions. Good underwriting turns them into a repeatable operating process. That's where a clear definition of credit worthiness matters. It gives finance, partners, and client service leads the same standard for evaluating risk before exposure grows.

A practical underwriting decision in professional services might include:

- A credit limit tied to expected billings.

- A payment structure such as retainer, milestone, or monthly invoicing.

- Escalation conditions if balances age past an internal threshold.

- Review triggers when scope expands or payment behavior changes.

That's the difference between controlled growth and accidental lending.

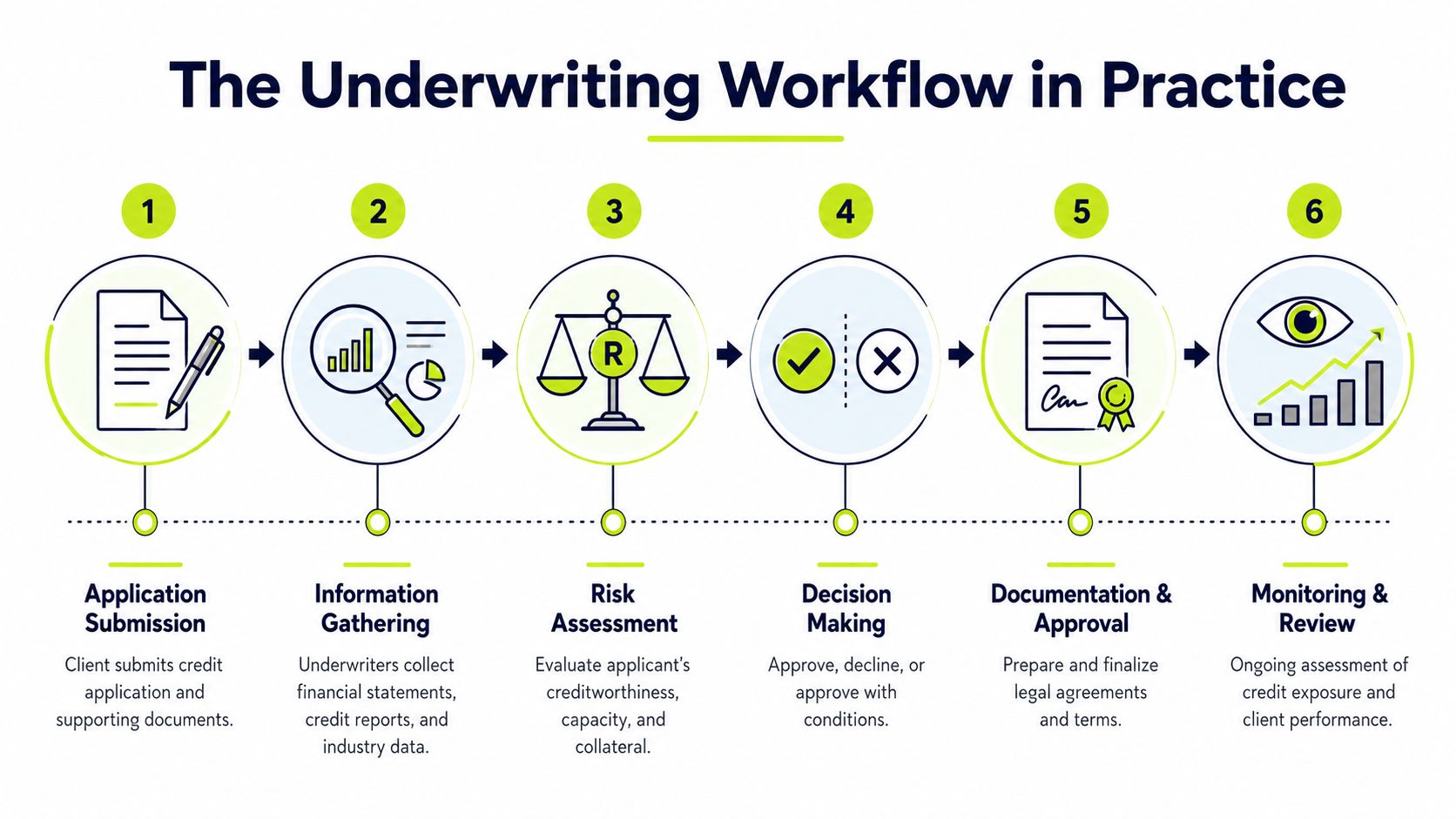

The Underwriting Workflow in Practice

The cleanest underwriting processes look unremarkable from the outside. A client submits paperwork. Finance reviews the file. Terms get set. Work begins.

What separates strong operators from reactive ones is that every step produces an enforceable decision, not just a file in a folder.

A typical workflow for a new business client

Start with a common scenario. A new corporate client wants immediate onboarding, asks for standard net terms, and expects work to begin this week.

A disciplined finance team usually moves through the workflow in stages:

- Application intake The client completes a credit application and provides the basics. Legal entity, billing contacts, ownership details, trade references, and, where appropriate, financial statements.

- Information gathering The controller or AR lead pulls external and internal signals. Existing payment history if the client has worked with you before. Public records. References. Bank or accounting data when available and permissioned.

- Risk assessment The team evaluates the file against internal policy. Not just “good” or “bad,” but how much exposure is acceptable and under what conditions.

- Decision There are usually three outcomes. Approve, decline, or approve with conditions.

- Documentation Terms go into the engagement documents and billing setup. Credit limit, due dates, retainers, milestones, and any exceptions need to be explicit.

- Monitoring Once invoicing starts, the original decision is tested against actual behavior. Here, many firms stop too early.

The outcome is terms, not just approval

The OCC makes an important point that many firms miss. Credit underwriting sets binding terms such as financial requirements, repayment programs, maturities, pricing, and covenants, and those terms directly shape expected loss and cash flow. A weaker risk profile leads to tighter terms to contain risk, as noted in the OCC guidance on commercial credit underwriting.

That principle applies directly to services firms, even if you're not issuing term loans.

Client profile | Sensible structure |

|---|---|

Strong payer, stable business | Standard net terms, normal limit, regular billing cadence |

Mixed payment history | Lower limit, tighter billing cycles, deposit or milestone billing |

Thin information, urgent start | Partial prepayment, short review window, partner approval |

Existing client showing stress | Hold scope expansion, shorten terms, require balance reduction |

Approved business can still be badly structured business.

What works and what doesn't

What works is a workflow that finance can run consistently, even when sales pressure is high.

What doesn't work is treating every exception as a one-off act of judgment. That leads to scattered terms in emails, unclear approvals, and AR teams discovering too late that nobody defined the limit, billing cadence, or consequence for slow payment.

For firms focused on improve cash flow and reduce DSO, the underwriting workflow matters before the first invoice goes out. Once the balance is overdue, your options narrow quickly.

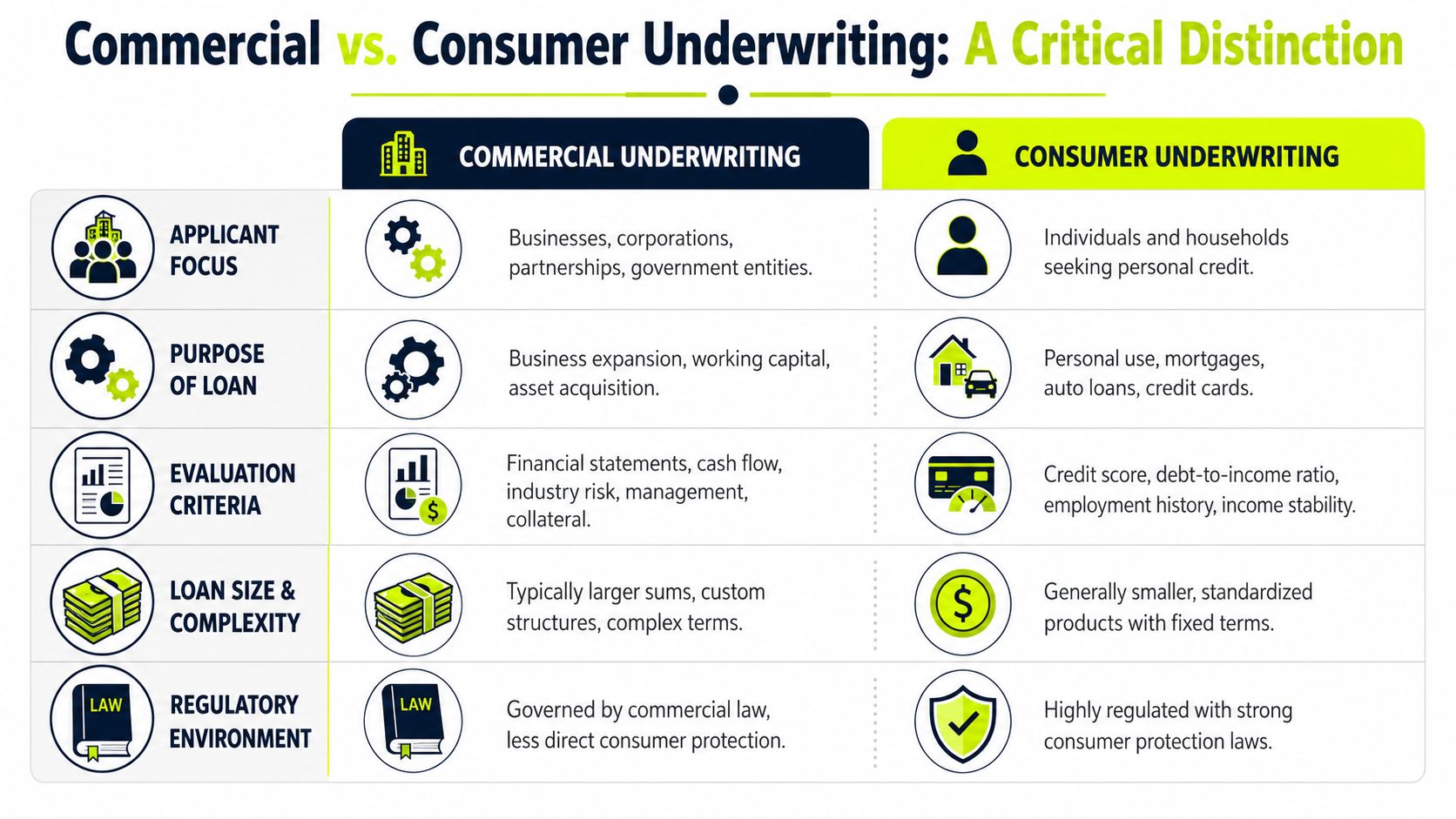

Commercial vs Consumer Underwriting A Critical Distinction

A lot of confusion around underwriting comes from borrowing consumer credit language and applying it to business clients. That's where finance teams get false comfort.

Consumer underwriting is designed for scale and standardization. Commercial underwriting is designed for context.

Side by side

Here's the practical difference:

Category | Commercial underwriting | Consumer underwriting |

|---|---|---|

Applicant focus | Business entity, ownership, management, operating model | Individual borrower or household |

Core question | Can this business support trade or loan obligations over time? | Can this person repay a standard credit product? |

Inputs | Financial statements, cash flow, industry exposure, references, structure | Credit score, income, employment, debt obligations |

Terms | Often tailored to the account and risk | Usually standardized by product |

Judgment | Higher level of qualitative review | Higher level of automation |

A services firm extending terms to another business is doing commercial credit underwriting, even if the dollar amount feels routine.

Why the distinction matters

A business can have a decent-looking file and still be a poor credit risk for your firm. Maybe revenue is concentrated in one customer. Maybe leadership turns over often. Maybe the company funds growth by stretching every vendor.

Those details matter because B2B receivables aren't just a credit decision. They're an operating exposure. Your firm has already delivered labor, time, and margin before collections trouble becomes visible.

Consumer logic asks, “Did they repay before?” Commercial logic asks, “Will this business stay able and willing to pay under the terms we're offering?”

That's why a consumer-style pass/fail screen isn't enough for professional services. It may help with triage, but it won't tell you how to structure retainers, invoice cadence, or exposure limits for a growing client with uneven cash movement.

A better mindset for firm owners and finance leaders

If you run a services business, don't ask only whether the client is creditworthy. Ask whether the relationship can be financed safely.

That shifts the conversation from approval to design:

- How much work should be in progress before invoicing?

- Which services require advance funding?

- When should terms tighten automatically?

- Who can approve exceptions, and how are they documented?

That's the commercial lens. It's less elegant than a score, but it's much closer to reality.

The Metrics That Matter for B2B Credit Risk

Historical credit data still has value. It tells you how a client has behaved. But in B2B services, delayed payment problems often show up first in current cash movement, not in old bureau history.

That's why the strongest underwriting teams don't stop at retrospective files. They look for evidence of financial behavior that is current enough to support a live decision.

Why cash flow tells you more

FinRegLab found that cash-flow data from deposit, card, and accounting systems is predictive of credit risk and offers a more timely picture of financial behavior than traditional credit reports, making it especially useful in automated underwriting. Their cash-flow underwriting fact sheet is worth reading if you're revisiting how your team assesses client risk.

For a CFO, that conclusion is practical. A client's payment capacity is easier to judge when you can see how money moves through the business.

The signals worth watching

In professional services, these are usually more revealing than a single score:

- Recent payment behavior If a client has already paid your smaller invoices late, don't assume larger balances will improve.

- Billing-to-cash alignment A client may be profitable on paper and still struggle because customer receipts arrive unevenly.

- Customer concentration If one customer drives most of their collections, your invoices are exposed to someone else's payment discipline.

- Scope growth versus payment discipline A client asking to expand work while carrying aging balances is signaling strain or weak controls.

- Internal process quality Missing purchase orders, invoice disputes, and frequent AP contact changes often predict collection friction before outright delinquency.

Turning metrics into operating decisions

Teams often overcomplicate things. You don't need a perfect model to improve underwriting. You need a short list of indicators that can trigger action.

For example:

Signal | What it may mean | Credit response |

|---|---|---|

Slower recent payments | Liquidity pressure or low invoice priority | Reduce exposure, tighten follow-up |

Rising dispute volume | Weak client process or stalling behavior | Pause new work until billing path is clear |

Expansion request with open balance | Relationship is growing faster than collections | Move to milestone billing or prepayment |

Inconsistent financial data | Limited visibility into capacity | Start with conservative terms |

If your team is building a more systematic review process, AI can help organize and interpret messy financial inputs. A practical overview of top AI tools for data analysis can help finance leaders think through where analysis software fits and where human judgment still matters. For a deeper look at the operating side, these credit risk assessment tools show how finance teams turn risk signals into day-to-day controls.

The point isn't to automate away judgment. It's to stop relying on backward-looking signals alone when your exposure lives in the present.

From Static Decision to Dynamic AR Management

Most firms underwrite once and collect forever. That's the flaw.

A client approved at onboarding can become risky months later because their own customers slow down, internal approvals break, or project scope expands faster than payment behavior supports. If you treat underwriting as a one-time event, AR becomes the place where those missed signals finally surface.

Underwriting should continue after approval

In services businesses, post-sale risk often shows up through operational behavior:

- Invoices start aging in small increments rather than failing all at once.

- Approvers go silent and AP asks for resubmissions.

- Scope expands while old balances remain unresolved.

- Disputes become procedural, not substantive. The work is accepted, but payment keeps slipping.

Those aren't just collections issues. They're signals that the original underwriting assumptions need to be revisited.

This is why accounts receivable shouldn't sit outside the credit conversation. AR is where you see whether the client is performing inside the structure you approved.

Where automation helps and where it fails

Modern underwriting engines can process high volumes quickly and consistently, but they depend on data quality. If inputs are stale or incomplete, the resulting risk rating can underprice default risk or over-restrict strong borrowers, according to the Provenir guide to credit underwriting.

The same lesson applies to accounts receivable automation and AI AR automation. Software is useful when it works from current invoice status, real payment behavior, and clean customer records. It fails when the system is only automating reminders on top of bad account setup and outdated credit assumptions.

Operating view: Automation doesn't replace underwriting discipline. It exposes whether you have any.

What dynamic AR management looks like

The better model is continuous underwriting through the AR cycle.

That usually means:

- Setting terms at origination based on risk.

- Monitoring payment behavior against those terms.

- Triggering reviews when patterns deteriorate.

- Adjusting account strategy before balances become uncollectible.

For many firms, AR software for professional services proves strategically useful. Not because it sends emails faster, but because it helps finance teams see risk early enough to act.

A capable workflow can connect billing, collections, and client behavior in one operating loop:

AR signal | Likely interpretation | Finance action |

|---|---|---|

Repeated short delays | Emerging liquidity stress or low payment priority | Tighten cadence and review limit |

Promises to pay keep moving | Weak control on client side or deliberate delay | Escalate outreach and re-approve exposure |

Payment only after manual intervention | Account needs active management, not standard terms | Move to higher-touch collections path |

New work opens while old invoices age | Revenue growth is masking credit deterioration | Hold or re-stage work until balance normalizes |

This is also where QuickBooks AR automation and similar integrations matter. If your accounting data, invoice status, and collection activity don't stay aligned, finance ends up making decisions on lagging information.

Teams that want a more disciplined operating model should think of AR as a forecasting input, not just a back-office task. If you're refining how your team evaluate forecasting performance, receivables behavior deserves a place in that review because expected cash timing is only as good as the payment assumptions underneath it. And if you want the AR side framed operationally, this primer on what AR automation is is a useful companion.

The real trade-off

The trade-off isn't technology versus relationships. It's consistency versus improvisation.

Clients usually don't object to clear terms, timely reminders, or structured follow-up. They object to surprises and uneven handling. A dynamic credit and collections model protects the relationship because it makes expectations visible early, when options still exist.

That's what finance leaders should want. Better control, fewer avoidable escalations, and cash flow that reflects actual client behavior rather than hopeful assumptions.

Conclusion The New Standard for Credit and Collections

The practical answer to what is credit underwriting is simple. It's the discipline of deciding how much risk your firm will carry, on what terms, and how that decision will be managed once work begins.

For professional services firms, that decision can't stay frozen at onboarding. Client conditions change. Payment behavior shifts. Scope expands. If finance only checks risk once, AR ends up carrying the burden later.

The stronger model combines underwriting and collections into one operating system. Finance sets terms based on risk, monitors whether the client performs inside those terms, and adjusts before a late balance turns into a write-off. That's how firms reduce DSO, protect margin, and improve cash flow without turning every client conversation into a dispute.

Good control doesn't require heavy bureaucracy. It requires consistent standards, current data, and a willingness to treat receivables as a live credit exposure. That's the difference between reactive collections and managed cash flow.

Professional relationships don't suffer from clear financial discipline. In most cases, they improve because both sides know how the account will be handled if timing starts to slip.

Resolut automates AR for professional services with a controlled approach that stays consistent, accurate, and human. If you want underwriting and collections to work as one process instead of two disconnected tasks, it's worth a look.