What Is Payment Orchestration: CFO Guide to Reducing DSO

What is payment orchestration? Guide for finance leaders on AR automation, reducing DSO, improving cash flow, and optimizing payment costs.

If you're running a professional services firm, this probably feels familiar. Invoices go out on time, but cash still comes in unevenly. One client pays by card through a portal, another mails an ACH remittance separately, a third asks to split a payment, and your team spends too much time chasing failed transactions that should have been recoverable.

The problem usually isn't invoicing alone. It's that the payment layer behind receivables is fragmented. Gateway here, processor there, manual retries somewhere else, and reconciliation living in QuickBooks or a spreadsheet after the fact.

That's where payment orchestration becomes useful. Not as another finance tool to buy, but as a way to take control of how money moves after you bill a client.

Beyond the Gateway An Introduction for Finance Leaders

Most finance leaders don't wake up asking, "What is payment orchestration?" They wake up looking at aging AR, expected payroll, partner distributions, and a cash forecast that depends on clients paying when they said they would.

In a professional services firm, that pressure shows up in small operational failures. A client's card on file soft-declines. An ACH attempt doesn't settle cleanly. A payment link works for one client but not for another preferred method. Your AR team follows up manually, then finance has to match the payment later across disconnected systems.

That friction matters because unpaid invoices are not a theoretical problem. 1 in 10 B2B invoices go unpaid, costing enterprises $200B annually. In that context, payment orchestration stops being an e-commerce concept and starts looking like an AR control mechanism.

A lot of firms already have pieces of the stack. They may use a processor, a billing tool, and a client portal. They may also be comparing payment gateways for business without realizing the larger issue isn't just which gateway they choose. It's how they manage payment attempts, fallback logic, client choice, and reconciliation as one connected process.

Payment friction doesn't just delay collection. It turns a collectible invoice into a receivable problem.

For CFOs and controllers, the key shift is this. Payments shouldn't be treated as a single processor relationship. They should be managed as a controllable system with rules, fallback paths, and visibility.

That's what orchestration gives you. It creates one layer that can coordinate payment methods, providers, retries, and reporting so your team doesn't have to do that work by hand. In an AR context, that means fewer stalled invoices, faster recovery of failed payments, and a more predictable path from invoice sent to cash applied.

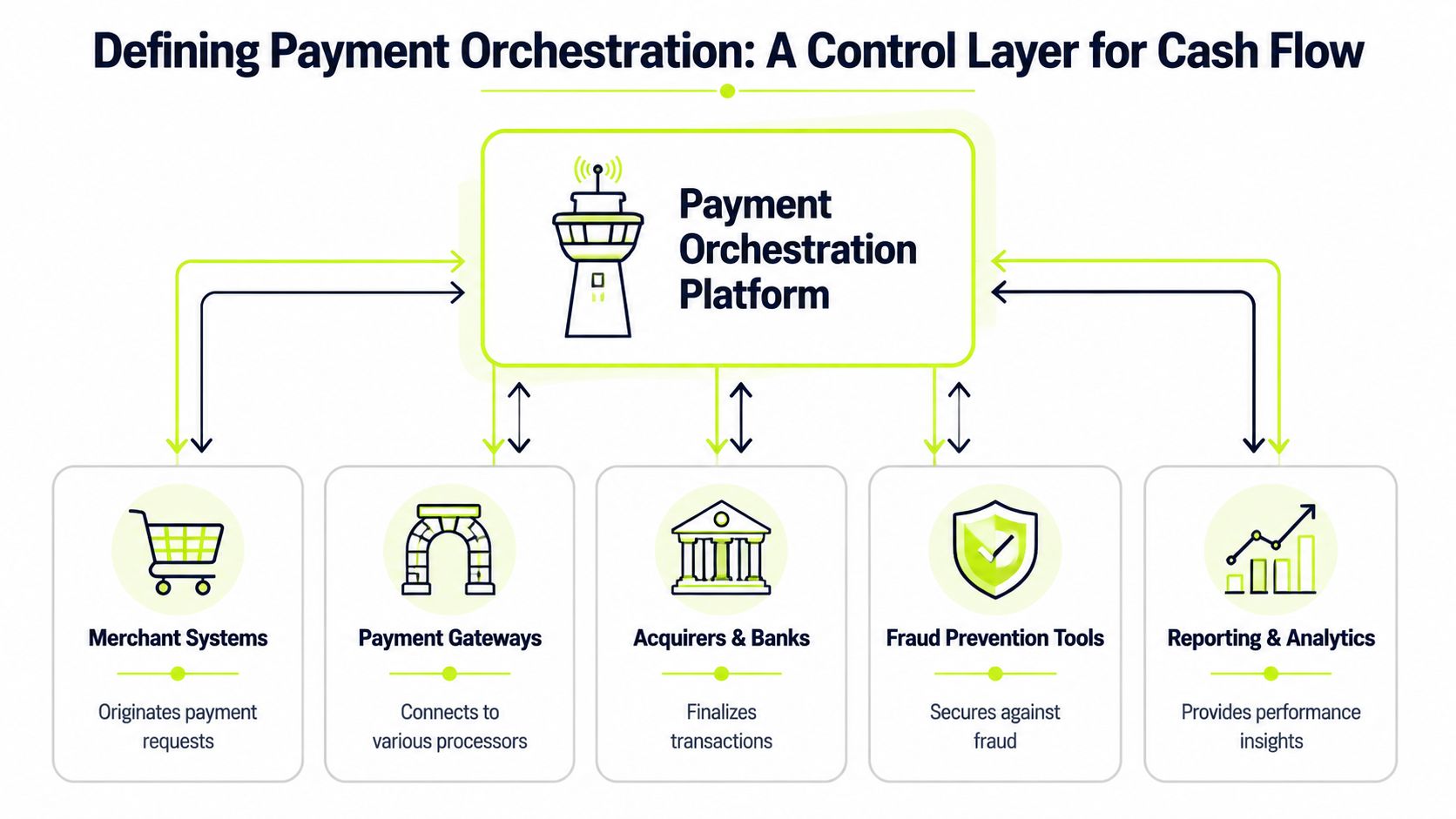

Defining Payment Orchestration A Control Layer for Cash Flow

Payment orchestration is a control layer that sits above gateways, payment service providers, acquirers, fraud tools, and payment methods. Instead of connecting each system one by one, the business connects once to the orchestration layer, then manages routing, retries, and operational control from there.

For a finance leader, the simplest analogy is a control tower. The planes still fly. The runway still matters. The destination still matters. But the tower decides how traffic moves safely and efficiently. In payments, the gateways and processors still execute transactions. The orchestration layer decides how those transactions should be directed and what should happen when the first path fails.

What it is and what it isn't

A payment gateway connects a payment experience to transaction processing. A processor or PSP handles the underlying payment execution. An orchestrator doesn't replace those functions. It coordinates them.

That distinction matters. If your firm adds a second processor, a local payment method, or a different collection channel, you don't want to rebuild the whole stack each time. Orchestration is designed to prevent that. It gives finance and operations a central point of control instead of a chain of point solutions.

According to Custom Market Insights on the payment orchestration platform market, the global market was valued at $1.8 billion in 2025 and is projected to reach $13.4 billion by 2034 at a 24.5% CAGR. That growth reflects a practical need: businesses want one integration layer above multiple PSPs and payment methods so they can manage routing, retries, and reporting centrally.

Why finance should care

The finance value isn't technical elegance. It's operating control.

A solid orchestration setup usually changes these parts of the workflow:

Function | Without orchestration | With orchestration |

|---|---|---|

Provider management | Separate relationships and logic by provider | One control layer across providers |

Retries | Manual or limited | Rules-based and automated |

Reporting | Fragmented dashboards | Consolidated visibility |

Expansion | New integration work for each addition | Reusable payment infrastructure |

That has direct implications for AR software for professional services. If you bill retainer clients, milestone invoices, or recurring service fees, you need a payment structure that can support more than a single static route. You need a system that can adapt without your team improvising every exception.

A short explainer helps make the model concrete:

The practical definition

If someone asks what is payment orchestration in plain English, the best answer is this:

Practical rule: Payment orchestration is the operating layer that lets a business decide how a payment should be attempted, retried, rerouted, recorded, and reconciled without being trapped inside one provider's logic.

For CFOs, that's the point. It's not another checkout feature. It's an infrastructure decision that affects cost control, collection speed, resilience, and visibility into cash movement.

The Architecture of Smart Payment Routing

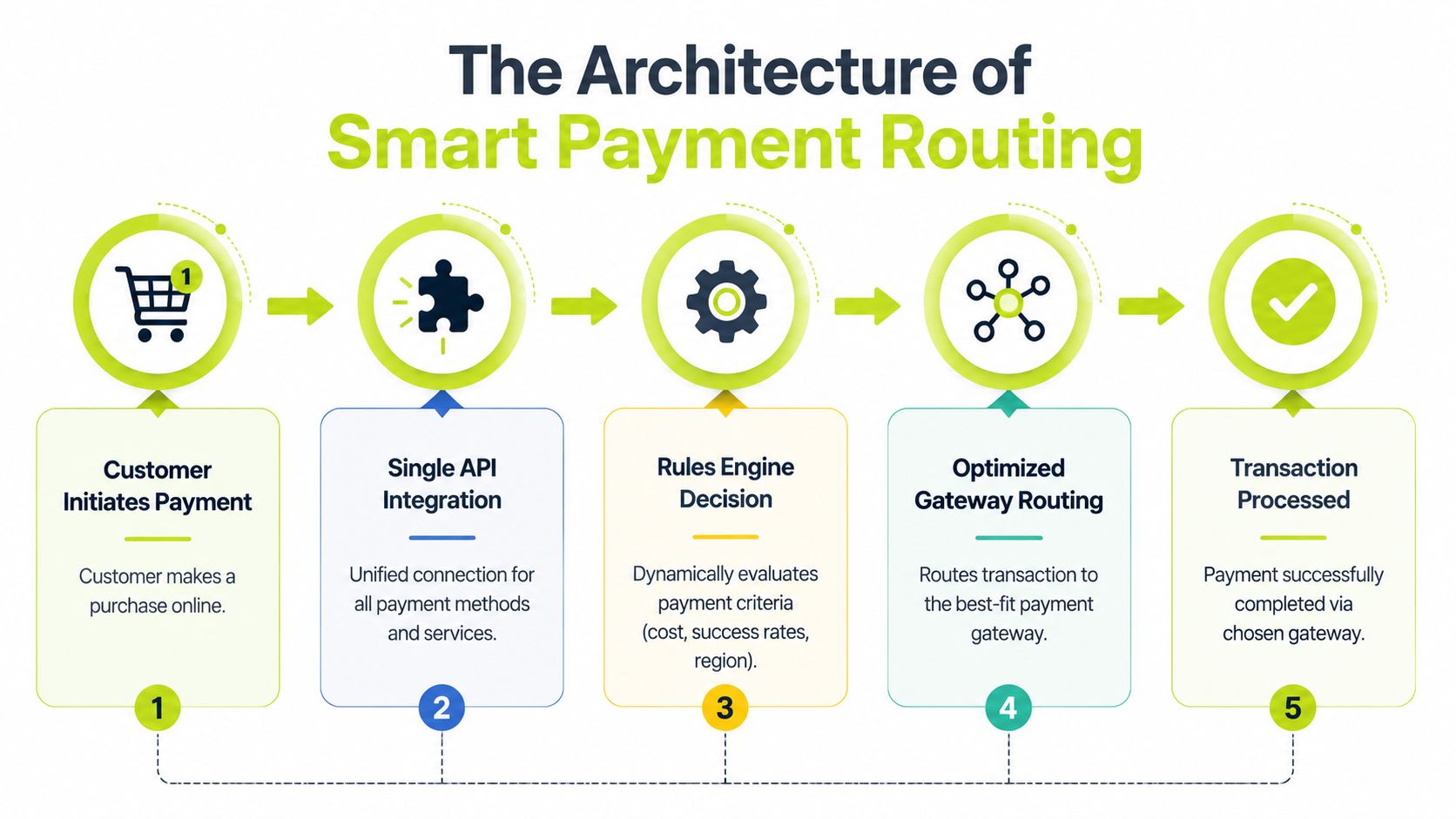

The value of orchestration comes from its logic, not its label. If the system can't make better routing decisions than your team can make manually, it won't move DSO or reduce operational drag.

At a high level, the architecture is straightforward. A single API or connection sits between your billing or client payment experience and the providers that can process the transaction. Inside that layer is a rules engine. The rules decide where a payment should go based on business conditions such as geography, currency, cost, provider performance, or payment method.

How the routing logic works

The useful part isn't that there are multiple providers. The useful part is that the orchestration layer can choose among them in real time.

ACI Worldwide's guide to merchant payments orchestration describes this model as a control plane above gateways and PSPs. It routes transactions based on rules such as geography, cost, or performance, and supports failover, retries, and provider optimization without rebuilding integrations for each provider.

For a professional services firm, that can look less like online checkout optimization and more like disciplined collections infrastructure.

Take a common AR scenario:

- An invoice becomes due. The client receives a payment request through your normal billing channel.

- The first payment path is attempted. You may prefer bank transfer or ACH first because it's aligned with cost control.

- That attempt fails or stalls. The failure might be temporary, method-specific, or provider-specific.

- The orchestration layer reroutes. It can trigger another approved payment path, such as a card on file or a different provider.

- The result flows back into reporting and reconciliation. Your team sees the outcome in one place instead of piecing it together later.

At this juncture, B2B online payment methods become more than a menu of options. The method matters, but the sequence and fallback logic matter more. Offering ACH, cards, and digital methods is useful. Coordinating them intelligently is what improves collection performance.

What works and what doesn't

What works is clear routing logic tied to business priorities. If your main goal is margin protection, route lower-cost methods first where appropriate. If your main goal is speed for aging invoices, prioritize the highest-likelihood collection path. If your client base spans regions, tailor routing by geography and payment preference.

What doesn't work is treating orchestration like a passive integration project. The firms that get value from it actively define rules.

A practical configuration often includes:

- Priority-based routing: Decide when cost should win and when collection speed should win.

- Failure handling: Separate soft failures from hard failures so the system doesn't repeat bad attempts.

- Client-aware preferences: Use payment paths that fit how the client already pays.

- Operational feedback loops: Review which routes produce avoidable failures and adjust.

A routing engine is only as good as the finance policy behind it.

When firms skip that discipline, orchestration becomes an expensive abstraction layer. When they use it well, payment handling becomes more resilient and less dependent on staff intervention.

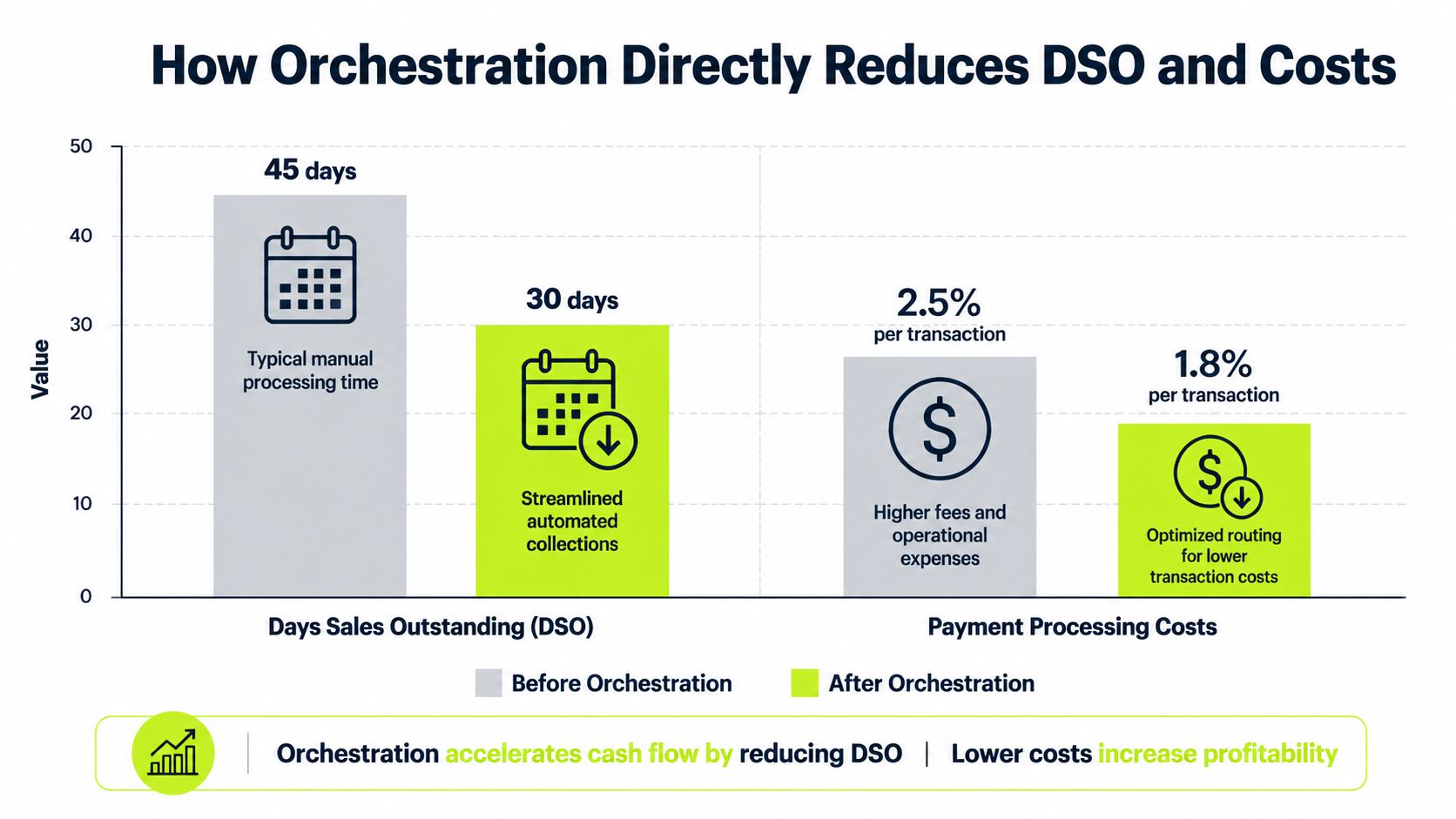

How Orchestration Directly Reduces DSO and Costs

The finance case for orchestration is simple. It helps you collect more successfully, with less manual effort, and with better control over processing economics. That combination affects DSO, cost to collect, and working capital.

Better payment recovery means faster cash

A surprising amount of receivables drag comes from payments that were close to collectible but failed in execution. A card expires. A processor returns a soft decline. A client abandons one payment path but would've completed another.

This is where orchestration matters in accounts receivable automation. Instead of leaving every failed attempt to manual follow-up, the system can apply retry logic, switch providers, or present another method before the invoice ages further. In AR, that shortens the gap between invoice due date and cash received.

The Spreedly guide to payments orchestration cites a 2022 PYMNTS report showing that 54% of U.S. merchants and 62% of U.K. merchants using payment orchestration said it reduced overall costs. The same source notes that smarter routing and failover logic can improve authorization rates by 2–10%.

For a CFO, you don't need to overcomplicate the implication. If more attempted payments complete successfully, fewer invoices sit in follow-up queues and fewer balances age into collection problems.

Lower friction helps clients pay on time

Professional services firms often focus on invoice accuracy, which is important. But client payment experience matters too. If the client has to leave the portal, call accounting, or request a different method after a failure, delay is almost guaranteed.

Orchestration supports a cleaner process because it can connect multiple payment methods and routes behind one front-end experience. That aligns well with accounts receivable automation and AI AR automation strategies where reminders, links, payment options, and follow-ups work together instead of in silos.

The fastest way to reduce DSO is often to remove the extra decision the client has to make after a payment fails.

That's also why payment orchestration pairs well with operational systems such as accounting automation software. The more your finance stack can move from fragmented handoffs to connected workflows, the less time your team spends repairing exceptions.

Cost control improves when routing is intentional

Most firms look at payment cost after the fact. They review statements, spot fee patterns, and accept some leakage as unavoidable. Orchestration changes that sequence. It allows the business to make routing choices before the cost is incurred.

That doesn't mean every payment should follow the cheapest route. It means the route should fit the invoice, the client, and the collection objective.

A finance-led routing model often looks like this:

- Current invoices: Favor lower-cost rails when the client usually pays reliably.

- Aging balances: Favor the route most likely to collect now, even if the fee is slightly higher.

- Large or sensitive accounts: Use proven methods that reduce avoidable friction.

- Cross-provider resilience: Avoid dependence on a single PSP when continuity matters.

Reconciliation gets easier

Cash flow doesn't improve just because payment succeeds. It improves when the payment is applied accurately and quickly enough for the ledger and forecast to reflect reality.

Orchestration supports downstream finance operations. A centralized payment layer can feed cleaner transaction data into reconciliation and cash application processes rather than leaving your team to decode multiple provider records. If you're refining payment reconciliation, that centralization matters.

In practice, that means fewer suspense items, fewer manual touches, and less lag between payment receipt and financial visibility.

What to watch for

Orchestration doesn't reduce DSO by magic. It works when the firm connects the payment layer to collection strategy.

That usually means:

- defining retry windows,

- aligning payment methods to client behavior,

- separating convenience from control,

- and making sure your AR team can see why a payment succeeded, failed, or rerouted.

If those pieces are missing, the platform may process transactions but won't improve cash flow in a meaningful way. If they're present, orchestration becomes one of the more practical levers available to finance teams trying to improve cash velocity without adding headcount.

An Implementation Checklist for Professional Services

Most orchestration projects succeed or fail before the technology goes live. The issue is usually governance. Firms buy for flexibility, then discover they haven't defined rules, ownership, or compliance boundaries clearly enough.

For professional services firms, the implementation should stay grounded in receivables operations. Start with how clients pay, where payments fail, and which handoffs still require staff intervention.

Start with a payment process audit

Before evaluating vendors, map your current payment flow from invoice delivery to cash application.

Look for these friction points:

- Failed payment patterns: Which invoices fail because of method mismatch, processor issues, or avoidable client friction?

- Manual recovery work: Where does your AR staff intervene by email, phone, or portal reset?

- Reporting gaps: Which data points are split across QuickBooks, processor dashboards, and spreadsheets?

- Client exceptions: Which accounts need special payment handling that currently lives in someone's inbox?

This step sounds basic, but it's where firms usually discover the actual business case. The need isn't "more payment options." It's fewer broken handoffs.

Define routing rules before tool selection

Don't ask a vendor to tell you your payment strategy. Decide what the rules should optimize for.

A practical finance checklist includes:

- Cost rules When should the system favor lower-cost payment rails?

- Urgency rules When an invoice is aging, should the system prioritize the payment path with the highest likelihood of collection?

- Client preference rules Which clients should be offered or defaulted into specific methods based on prior behavior?

- Fallback rules What should happen after a soft failure, and what should never happen after a hard decline?

- Approval and exception rules Who owns changes to routing logic, and who signs off on exceptions?

Most implementation pain comes from unclear rules, not weak software.

Plan the systems layer carefully

A good orchestration layer should simplify the environment around it, not create a new finance island. That means planning how it connects to the rest of your stack.

For many firms, the critical systems are:

- QuickBooks or another accounting platform

- CRM records that hold billing contacts and account context

- the client payment portal

- collections workflows across email, SMS, or account outreach

If you're aiming for QuickBooks AR automation, don't stop at payment acceptance. Make sure the payment outcome can move cleanly into matching, posting, and exception handling. Otherwise you've automated the front end while preserving the manual work in the back office.

Treat compliance as a design issue

This is the part vendor demos often underplay. A single integration doesn't remove regulatory complexity. It can concentrate it.

A contrarian but important view is the risk of orchestration-induced fragmentation in compliance. Recent analysis indicates that while 70% of businesses adopt orchestration for multi-currency support, 40% report increased compliance errors due to misrouted data. That matters if your payment data crosses different tax and regulatory environments, including VAT or PSD2 obligations.

For finance leaders, the lesson is straightforward. Centralized payment logic needs region-aware controls. If the orchestration layer becomes a black box, your audit and compliance risk can rise even while operations look cleaner.

A useful vendor checklist should ask:

Question | Why it matters |

|---|---|

How are routing rules governed? | Prevents unauthorized logic changes |

How is transaction data mapped by region? | Reduces misrouting and reporting errors |

What audit trail exists? | Supports finance review and compliance testing |

How are exceptions surfaced to finance? | Keeps problems visible before month-end |

Set operating KPIs early

The best implementation teams agree on success measures before launch. Not abstract platform metrics. Finance metrics.

Use KPIs that answer:

- Are payment failures being recovered faster?

- Is manual follow-up decreasing?

- Is cash application cleaner?

- Is DSO moving in the right direction?

- Are client payment experiences improving or getting more confusing?

Those questions keep the rollout tied to working capital, not just system adoption.

For professional services firms, that's the standard that matters. If the orchestration layer doesn't improve control over collections and cash visibility, it isn't finished, no matter how polished the integration looks.

The Future of AR A Strategic View of Orchestration

The old model of receivables assumed payment was a back-end event. Send the invoice, wait, follow up, reconcile, repeat. That model still exists, but it doesn't hold up well when clients expect flexibility, finance teams are lean, and cash timing matters.

Payment orchestration changes the role of AR. It turns payments from a passive endpoint into an active operating layer. That matters for firms that want more than faster transactions. They want better control over cash conversion.

For CFOs and controllers, the strategic value is discipline. One place to govern routing. One framework for retries and fallback. One clearer view of what happened between billing and cash application. That is much closer to financial infrastructure than to checkout tooling.

Firms that treat payments as an operating system for receivables usually gain better control than firms that treat payments as a vendor setting.

This is especially relevant in professional services, where every delayed invoice affects staffing, hiring, distributions, and planning. A static gateway setup can still work for a simple environment. It becomes a constraint when your payment methods, client expectations, and systems complexity start to grow.

The finance teams that move first won't do it because orchestration sounds modern. They'll do it because they want fewer stalled payments, fewer manual exceptions, and more confidence in cash flow.

Resolut automates AR for professional services with a practical focus on getting you paid faster. It brings collections, payment workflows, and cash application into one operating system that stays consistent, accurate, and human. If you're rethinking how to reduce DSO and improve cash flow, Resolut is built for that job.